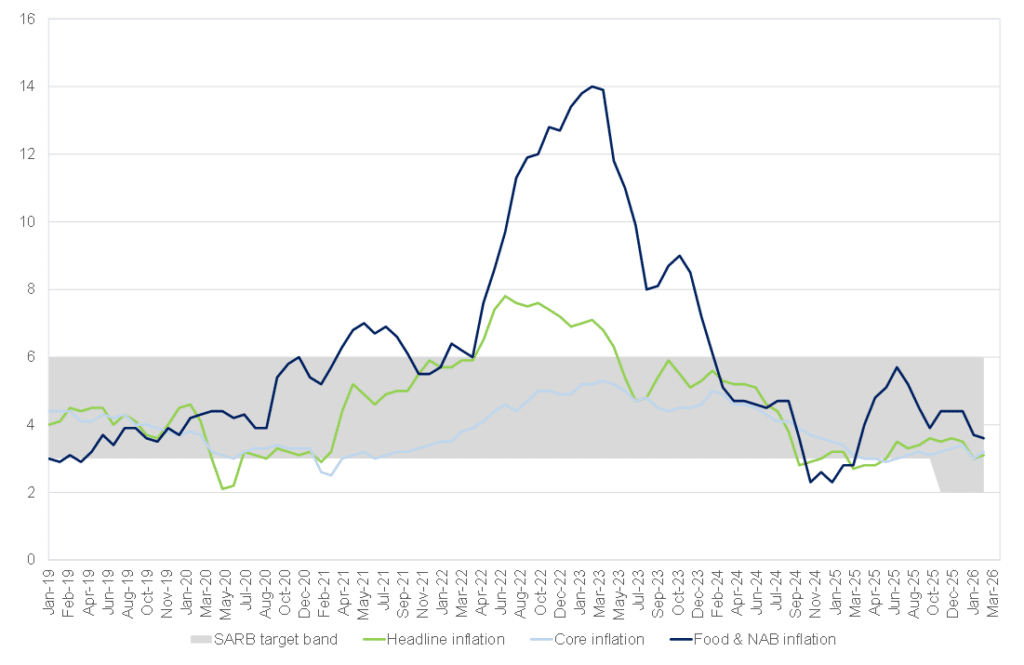

South Africa’s (SA) annual headline inflation rate, as measured by the Consumer Price Index (CPI), edged up to 3.1% YoY in March from 3.0% in February, in line with consensus expectations. MoM, headline inflation rose 0.6%. Core inflation, excluding the volatile food and non-alcoholic beverages, fuel and energy categories, followed a similar path, increasing slightly to 3.1% YoY (+0.6% MoM) vs 3.0% in February.

Importantly, inflation remains well-anchored within the South African Reserve Bank’s (SARB) recently adopted inflation target of 3%, with a 1-ppt tolerance band (meaning a range of 2%–4%), replacing the previous 3%–6% range and reinforcing the central bank’s efforts to anchor expectations at a lower level to support long-term economic growth.

However, the March data should be viewed as a pre-shock snapshot, captured prior to a significant escalation in global geopolitical tensions. There is no Iran war or closure of the Strait of Hormuz reflected in this latest inflation print, the reason being that any material disruption to oil supply routes would need time to filter through to the petrol pump price locally and then into CPI. Fuel prices were still down 8.7% YoY in March, with the overall transport category (-1.6% YoY) acting as a modest drag on headline inflation.

The energy picture was still positive when the March inflation measurements were taken, and this dynamic is set to reverse. As a net importer of refined petroleum, SA is highly exposed to higher global oil prices. The transmission mechanism is relatively direct: rising fuel costs feed into transport and logistics, with broader second-round effects across food, manufacturing, and services. April fuel price increases, which the government tried to mitigate by temporarily reducing the fuel levy, will begin to filter into upcoming inflation prints.

Figure 1: SA inflation, YoY % change

Source: Stats SA, Anchor Capital

March inflation was primarily driven by housing and utilities (+5.1% YoY, contributing 1.2 ppts to the 3.1% total rise), food and non-alcoholic beverages ([NAB]; +3.6% YoY, +0.6 ppts), and insurance and financial services (+4.6% YoY, +0.5 ppts). NAB inflation rose primarily because of high meat prices (+11.6% YoY but easing from February’s 12.2% YoY print), reflecting ongoing supply constraints due to the impact of the foot-and-mouth disease outbreak. Fruits and nuts remained in deflationary territory (-9.6% YoY). March’s print also included the annual fee adjustments in education services, with primary and secondary education services rising by 6.2% YoY and tertiary by 4.2% YoY. Average tuition fees across all education levels rose by 5.4% YoY.

From a policy perspective, the outlook has shifted. At its 26 March meeting, the SARB’s Monetary Policy Committee (MPC) held the repo rate at 6.75%, adopting a more cautious stance amid rising uncertainty. The easing cycle has effectively paused, with risks now tilted to a delay in rate cuts and, in more extreme scenarios, potential tightening. The SARB also revised its headline inflation forecast for 2026 upward to 3.7% from January’s 3.3%.

Our base case is that the interest rate remains on hold in the near term. The path forward will depend largely on the oil price trajectory and the persistence of geopolitical risks. A sustained period of elevated energy costs would place upward pressure on inflation and delay policy easing; conversely, a de-escalation could reopen the window for rate cuts.

SA enters this period in a relatively stronger position than in previous shocks, with improved fiscal dynamics and a more stable macro framework. Nonetheless, the key variable is not the initial oil price spike but its duration and the extent of second-round effects. In short, March’s inflation print reflects contained, largely domestic pressures, not commodity or energy market stress … yet.