Figure 1: Rand vs the US dollar

Source: Anchor

The escalation of military conflict involving the US, Israel and Iran at the end of February has triggered a geopolitical shock reverberating across global financial markets. Oil prices have surged, emerging market (EM) currencies, including the rand, have come under pressure, and investors are reassessing the outlook for global inflation. As a result, the prospects of meaningful rate relief for South African (SA) households have become less certain.

Prior to the escalation, Brent crude was trading at c. US$67/bbl, reflecting relatively balanced supply conditions and subdued global demand. However, within hours of the initial US/Israel military strikes, investors began pricing in the risk of disruption to the Strait of Hormuz through which c. one-fifth of global oil supply passes daily.

Iran’s retaliatory actions and the increased risk of disruption to Gulf energy infrastructure have sharply altered market expectations. In an unprecedented move, Iran declared the Strait effectively closed. By early March, Brent crude had soared above US$100/bbl, the first time oil had traded at that level since Russia’s invasion of Ukraine in February 2022. The sharp move in oil prices highlights the continued vulnerability of global energy markets to geopolitical shocks.

For SA, the surge in oil prices could have important macroeconomic implications. Rising crude oil prices typically translate into higher domestic fuel costs, which in turn filter through to transport, logistics and ultimately consumer prices.

At the start of this year, SA’s macroeconomic outlook had been gradually improving. Inflation had moderated, fiscal consolidation appeared to be gaining traction, and markets had begun to anticipate the likelihood of further monetary policy easing. The latest geopolitical developments have complicated this outlook.

A sustained increase in oil prices could place upward pressure on inflation at a time when policymakers were hoping to anchor inflation expectations closer to the South African Reserve Bank’s (SARB) 3% target. The SARB’s next Monetary Policy Committee (MPC) meeting is scheduled for 26 March, and the latest developments have increased the uncertainty surrounding the policy outlook.

Governor Lesetja Kganyago has indicated that the SARB may have to reassess its risk scenarios, considering the geopolitical escalation. Policymakers are now confronted with a classic supply-side shock – rising energy prices that lift inflation while dampening economic growth. Cutting rates in such an environment risks undermining the SARB’s inflation credibility, while maintaining restrictive policy for longer would place additional strain on households and businesses. The policy trade-off has become more complicated.

SA bond markets have begun to reflect this shift in sentiment. On 9 March, government bonds extended their worst sell-off since the COVID-19 pandemic period, as investors responded to the combination of rising oil prices and a weaker local currency. The benchmark SA 10-year government bond yield rose 36 bpts on the day and has increased by more than 90 bpts since the start of the conflict. This marks a sharp reversal from conditions at the end of February, when yields were trading near multi-year lows of c. 8%. We note that periods of risk-driven bond sell-offs often create attractive entry points. If the rise in yields proves temporary, investors locking in higher yields today may benefit as markets stabilise.

The rand, one of the most risk-sensitive EM currencies, has also come under pressure. During periods of heightened geopolitical uncertainty, investors typically reduce exposure to EMs and rotate capital toward perceived safe-haven assets.

Before the escalation, the rand had been performing exceptionally well, supported by broad-based US dollar weakness, surging commodity prices (notably gold and platinum) and, to a lesser extent, improving investor sentiment towards SA Inc. The currency briefly strengthened to below the psychological R15.70/US$1 level on 29 January.

Since the start of the conflict, however, the rand has reversed some of these gains (although it is still stronger than it was at the end of last year – R16.56/US$1 on 31 December). Between 28 February and 9 March, the currency weakened by c. 4.5%. It is trading at c. R16.29/US$1 at the time of writing. While we doubt it will happen, depreciation past the R17/US$1 could amplify the domestic inflation impact of higher oil prices, as fuel costs are ultimately priced in rand.

Kganyago has previously noted that a 10% depreciation in the rand typically has a more immediate and pronounced impact on SA inflation than a comparable rise in crude oil prices. As a result, the SARB will likely be vigilantly monitoring both currency movements and global energy markets in the coming weeks.

The economic impact of the conflict will ultimately depend on how the situation evolves. Below, we highlight three broad scenarios which will shape the economic consequences of the Iran war for SA.

- Rapid de-escalation (base-case): If military operations conclude within weeks, Iran’s new leadership signals de-escalation, and the Strait of Hormuz traffic resumes, oil prices could fall back towards the US$60-US$70/bbl range (oil at this level and the rand at around US$16.50/US$1 is hardly inflationary). In this scenario, SA will likely face a temporary inflation bump, but broader macroeconomic stability would remain intact. The rand would likely recover a significant portion of its recent losses as global risk appetite improves.

- Prolonged conflict and sustained disruption: If the conflict persists for several months and continues to disrupt Gulf energy infrastructure, oil prices could stabilise in the US$100-US$120/bbl range. Under this scenario, SA would face sustained fuel price increases and a renewed rise in inflation. The SARB would likely delay further policy easing, and economic growth could remain subdued.

- A severe disruption to global energy supply (worst-case scenario): If Iran manages to successfully enforce a prolonged disruption to shipping through the Strait of Hormuz, some analysts have suggested that such an outcome could push oil prices significantly higher, possibly triggering a broader global energy shock. For SA, this would represent a severe macroeconomic challenge with rising inflation, currency weakness, tighter monetary policy and a meaningful risk to economic growth.

Although SA is not directly involved in the conflict, the country remains exposed to global energy markets and shifts in international investor sentiment. For SA households, already under economic strain and grappling with a challenging cost-of-living environment, the impact of higher oil prices will become visible through fuel prices, transport costs and food inflation. While the local economy has demonstrated resilience to temporary shocks in the past, a prolonged period of elevated oil prices would place strain on SA’s still fragile recovery. The weeks ahead will be critical in determining whether the current market turbulence proves temporary or evolves into a more persistent macroeconomic challenge for SA and the world.

A contrarian view – perspective vs panic

While the dominant narrative has focused on the risks to SA and leaned toward alarm, the full picture may be more nuanced. Looking at the rand, we note that despite the war-driven sell-off, the currency remains stronger than where it ended 2025, and the exchange rate is also significantly firmer than the R17.84/US$1 average across last year. This suggests the move is more a correction than a structural collapse in the currency. The distinction matters because SA’s monthly fuel price adjustment uses an average of daily international petroleum prices and exchange rates across a full month – it is not calculated on intraday panic peaks. If current levels persist, petrol prices could rise by around R6/litre and diesel by c. R8/litre in April. While these numbers may be quite large, they come from a historically low base (petrol was at a c. four-year low of around R20/litre a few weeks back). Even after the Iran war shock, it would still be at prices considered unremarkable two to three years ago. So, the genuine risk is the duration of the spike rather than the initial spike itself. A one-month oil shock is absorbed, while a six-month shock can reshape inflation expectations and force the SARB’s hand.

While the current environment may prove uncomfortable, it does not yet resemble a systemic crisis. SA has entered this period with stronger fiscal buffers and a more stable macro framework than during previous shocks. The key variable will be the duration of elevated oil prices rather than the initial spike itself.

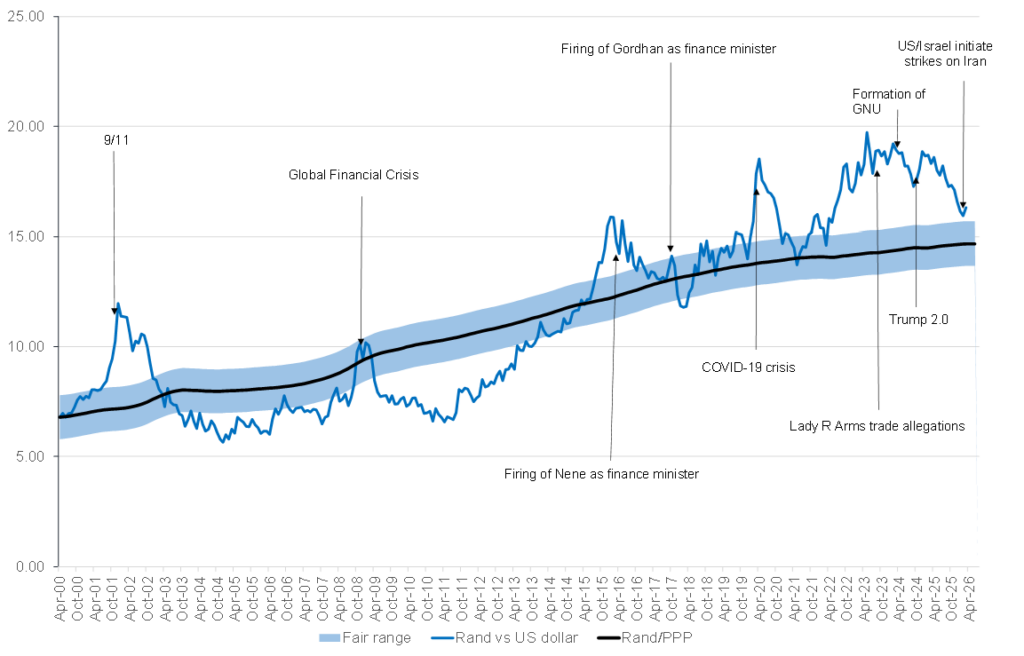

Figure 2: Actual rand/US$ vs rand PPP model

Source: Thomson Reuters, Anchor