For the past eighteen months, the investment case for South African (SA) focused equities has rested on a simple thesis. The end of loadshedding, the formation of the Government of National Unity (GNU), withdrawals under the two-pot retirement system, and a declining interest rate cycle would combine to reignite consumer spending.

Those tailwinds have largely arrived.

Unfortunately, as evidenced by the SA retail sector’s recent trading updates, the local consumer recovery has been surprisingly muted. Retail sales growth limped along at roughly 2%-3% in real terms through 2025, while many JSE-listed retailers underperformed several other sectors. The usual explanations largely continue to apply: still-elevated household debt, anaemic employment growth, and the lagged pass-through of SA interest rate cuts. But there is an increasingly obvious structural drain on discretionary spending in the form of gambling, specifically the rapid rise of online and sports gambling.

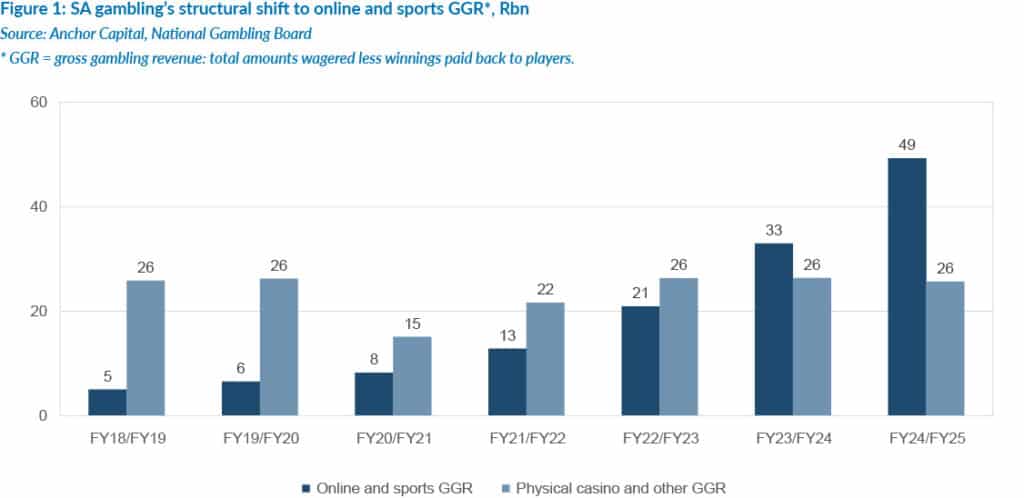

SA’s gambling industry has undergone a remarkable transformation. According to the National Gambling Board (NGB), total gross gambling revenue (GGR), the amount gambling operators realise after paying out winnings, reached R75bn in the year ending March 2025, up 26% YoY.

The expansion has been almost overwhelmingly driven by the explosion in online and sports betting.

We estimate that online and sports betting revenue increased from around R8bn in FY20/FY21 to c. R49bn in FY24/FY25 – a c. sixfold increase in just four years. As a result, online and sports betting now accounts for c. 66% of total gambling industry revenue, up from c. 35% in FY20/FY21.

Several forces converged to drive this structural shift in the gambling industry. The COVID-19 lockdowns accelerated and normalised the adoption of digital payments and pushed many first-time users onto mobile gambling platforms. Smartphone penetration reached over 70% of SA households, driving the proportion of online bets placed on mobile devices to 81%.

Aggressive marketing also played a role. Betting operators spent c. R2.6bn on advertising in the year ended March 2025, with three major brands, Hollywoodbets, Betway and World Sports Betting, accounting for nearly half of that spend. Walk through any airport, Gautrain station, or watch a sports broadcast in SA, and the scale of that advertising presence is hard to miss.

For equity investors, the key question is simple: How much consumer spending is being redirected from traditional retail channels into online gambling?

The data suggest that the shift is significant. According to the Bureau for Economic Research (BER), gambling revenue as a share of total recreation and culture spending increased from 12.3% before COVID-19 to 26.7% by March 2025. In more tangible terms, this means 25% of every rand South Africans spend on entertainment now flows into gambling.

This is not simply abstract macroeconomic analysis. Management teams across the JSE-listed consumer retail sector are flagging the damage in real time. The Foschini Group has publicly described online gambling as “almost entirely extractive”, suggesting it represents a greater threat to retail sales than competition from fast-growing international platforms such as Shein and Temu. Other consumer-facing businesses, including Pick n Pay, Famous Brands, and several others, have echoed similar concerns. Even transaction data hints at the shift. On Shoprite Holdings’ e-wallet platform, Hollywoodbets is the third item on the buying list, behind airtime and prepaid electricity.

The rise in online gambling creates several complications for analysts covering SA retailers. Traditional consumer spending forecasting models rely solely on macroeconomic variables such as interest rate changes, inflation, rand currency movements, and employment data. Ignoring this structural shift risks systematically overestimating the discretionary spending pool available to retailers.

SA regulators, however, are starting to stir. In November 2025, the National Treasury (NT) published a discussion paper proposing a 20% national tax on the GGR of all online gambling operators, payable to SARS on top of existing provincial gambling taxes of 6% to 9%. The gambling industry pushed back strongly, arguing that the combined burden of provincial taxes, VAT, and the proposed national tax would push effective rates to nearly 40%, driving more activity toward illegal offshore platforms.

Separately, the Democratic Alliance (DA) has introduced a private members’ bill (PMB) – the Remote Gambling Bill – aimed at creating a national framework covering licensing, consumer protection and enforcement. The bill is in its infancy, and optimistic timelines suggest in the order of two years to enactment. Meanwhile, illegal operators remain significant. Research by Yield Sec estimates that illegal online gambling operators generated c. R72bn in revenue during 2024, roughly double that of the legal online industry. Until a credible regulatory framework is in place, it falls to investors to account for a structural drain that most forecasting models are not yet capturing.

For investors wanting to allocate capital to JSE-listed retailers, the implications are clear: the consumer recovery trade may require more nuance than macro headline data suggests. Companies exposed primarily to essential spending – such as groceries, healthcare and education – are more insulated than those dependent on pure discretionary spend, such as casual dining, apparel and entertainment. Within discretionary retail, stock selection will become increasingly important. Companies with strong loyalty programmes, digital engagement platforms and differentiated brand positioning should prove more resilient than those reliant solely on a cyclical recovery in customer footfall.

The regulatory outlook may eventually alter the trajectory of online gambling, but the timing and impact offer little near-term comfort. Both the NT’s tax and the Remote Gambling Bill represent potential catalysts, but their directionality is unclear. A higher tax burden on operators could slow advertising spend and customer acquisition, easing pressure on retailers over time. Equally, it could simply push more activity into unregulated spaces where such constraints do not apply. NT’s own track record of abandoned gambling tax proposals (2011 and 2012) does not inspire much confidence that relief is coming soon. With advertising spend accelerating and regulation late to the game, the headwinds from online gambling are likely here to stay.

The drag from both legal and illegal online gambling is not trivial. At c. R49bn, after growing by roughly 50% in 2025, legal online and sports betting is no rounding error in the consumer equation. Understanding where the consumer rand actually goes, rather than where macro indicators say it should, may well be the difference between a well-positioned retail portfolio and an underperforming one.