SA’s 2026/2027 Budget, tabled in Parliament on 25 February, naturally brings tax considerations into focus!

Against this backdrop, it seems opportune to revisit developments in the trust space, particularly given the increasing regulatory scrutiny from the South African Revenue Service (SARS). While the Budget introduced very few direct changes relating specifically to trust taxation, SARS has expanded reporting requirements and is performing audits on many.

In this note, we recap the current tax framework that applies to local trusts, look at whether the indirect changes announced in the Budget have implications for SA trusts, and outline the areas of heightened regulatory focus being implemented by both the Master of the High Court and SARS.

Budget 2026: Key implications for trusts

1. Trust income tax rate (unchanged)

Ordinary trusts continue to be taxed at a flat rate of 45%. Special trusts (e.g., certain disability trusts or testamentary trusts for minors) are taxed at individual tax rates.

2. Capital gains tax (CGT) treatment (unchanged for trusts)

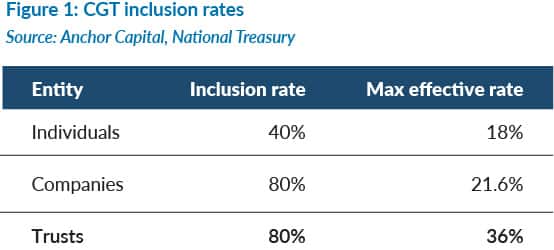

The budget commentary confirms that CGT inclusion rates are unchanged (see table in Figure 1 below):

Therefore, trusts still face a maximum effective CGT rate of about 36%.

3. CGT annual exclusion increase (affects special trusts)

One small change affecting trusts indirectly is that the annual CGT exclusion has increased from R40,000 to R50,000. This applies to individuals and special trusts.

Note: ordinary discretionary trusts do not qualify for this exclusion.

4. No new anti-trust or attribution rules announced

Importantly, for estate and fiduciary planning, the 2026 Budget did not introduce any new anti-avoidance rules targeting trusts. There were no changes to attribution rules (sections 7–25 of the Income Tax Act), the conduit principle, section 7C loan trust rules, or donations tax provisions.

5. Other budget changes that may indirectly affect trusts

Some broader changes may have practical implications for trusts:

- The annual donations tax exemption has increased to R150,000 (from R100,000).

- The primary residence CGT exclusion has increased to R3mn (relevant if a trust holds residential property and qualifies through special arrangements).

In summary, the 2026 SA Budget did not contain major changes to the core trust taxation framework, which remains in place:

- 45% income tax rate for trusts;

- 80% CGT inclusion rate; and

- no new structural or anti-avoidance reforms.

However, National Treasury and SARS have repeatedly indicated that trust taxation remains under policy review. Trust audits by SARS have become more stringent, and we elaborate on this topic below.

Trust audits

SARS has significantly intensified its scrutiny and auditing of family trusts, which it views as a potential area of tax leakage risk. This is driven, in part, by historically low levels of compliance, including a large number of dormant trusts, incomplete reporting, and the incorrect treatment of distributions.

Audits often focus on verifying whether:

- the trust is genuinely actively administered;

- income and capital gains are correctly declared; and

- beneficiary distributions are correctly taxed.

Key areas of focus include:

1. Enforcement of section 7C loan rules

A major driver of audits is compliance with section 7C of the Income Tax Act. Where individuals advance loans to trusts at low or no interest rates, SARS must verify whether:

- the official interest rate has been applied; and

- any deemed donation has been declared.

Many taxpayers either:

- misunderstand the rule; or

- fail to declare the deemed donation each year.

Consequently, loan accounts are closely scrutinised to ensure there is no tax leakage. This would mean that properly executed loan agreements need to be in place, signed by all parties, and with clear terms and conditions.

2. Beneficial ownership transparency requirements

Recent regulatory reforms require trusts to disclose beneficial ownership information, including details of founders, trustees, beneficiaries, and any individuals exercising effective control.

These requirements, enforced by institutions such as the Master of the High Court (South Africa) and the Financial Intelligence Centre (FIC), are designed to combat tax evasion, asset concealment, and money laundering.

The new reporting systems have resulted in enhanced transparency, which has improved SARS’s ability to identify inconsistencies across trust structures.

3. Data analytics and improved technology

SARS continues to invest heavily in data analytics and AI-driven risk profiling. Information is now cross-referenced across multiple sources, including financial institutions, company records, property registries, and international reporting systems.

This enables SARS to identify situations where:

- A trust holds significant assets with minimal reported income;

- beneficiaries receive distributions not reflected in tax returns; and

- continued founder control over trust assets.

These discrepancies often trigger audits or verification requests.

4. Increased focus on high-net-worth taxpayers

Specialised SARS units now focus on high-net-worth individuals (HNWI) and their associated structures. Trusts are commonly used within these structures, so audits often review the individual taxpayer, the trust itself, and related companies and beneficiaries as part of a holistic assessment of wealth structure.

This integrated approach means family trusts are often audited as part of broader wealth reviews.

5. Common issues in trust audits

Some of the most common problems identified during audits include:

- inadequate record keeping by trustees;

- undocumented or poorly structured loan accounts;

- failure to declare section 7C deemed donations;

- attribution rules not applied correctly;

- rental income, non-disclosure, and repairs/maintenance expenses;

- incorrect application of the conduit principle;

- failure to record beneficiary distribution resolutions before year-end; and

- trustees treating trust assets as personal assets by founders or trustees.

Summary

Although the 2026 Budget did not introduce material changes to the taxation of trusts, the regulatory environment continues to tighten. SARS has increased audits of family trusts on the assumption that they are widely used for wealth planning and historically created opportunities for tax leakage. With improved reporting rules and data analytics, SARS can now identify high-risk trust structures more easily and enforce compliance more aggressively. In the current regulatory environment, one needs to be aware of the focus of the authorities and the fact that it is not possible to avoid scrutiny with the increasing reporting that trusts are subjected to and the integrated data available.

If you are uncertain whether your trust structures meet current requirements, we would be pleased to assist in reviewing your arrangements and ensuring compliance with the more stringent approach that is being adopted.

Please get in touch with us by emailing Di Haiden.