ASSET ALLOCATION SUMMARY

Financial markets were shaken by the US and Israeli military strikes on Iran and Iran’s subsequent closure of the Strait of Hormuz, a critical global energy transit route. The resulting increase in oil prices, together with concerns around potential supply disruptions and the impact on global inflation, has weighed on asset prices. Despite this, market behaviour suggests that investors are pricing in a contained conflict with an eventual resolution. While sentiment has been impacted, there has been no broad-based capitulation in asset prices, indicating a degree of underlying resilience and confidence among investors in a stabilisation of conditions and an eventual sensible outcome.

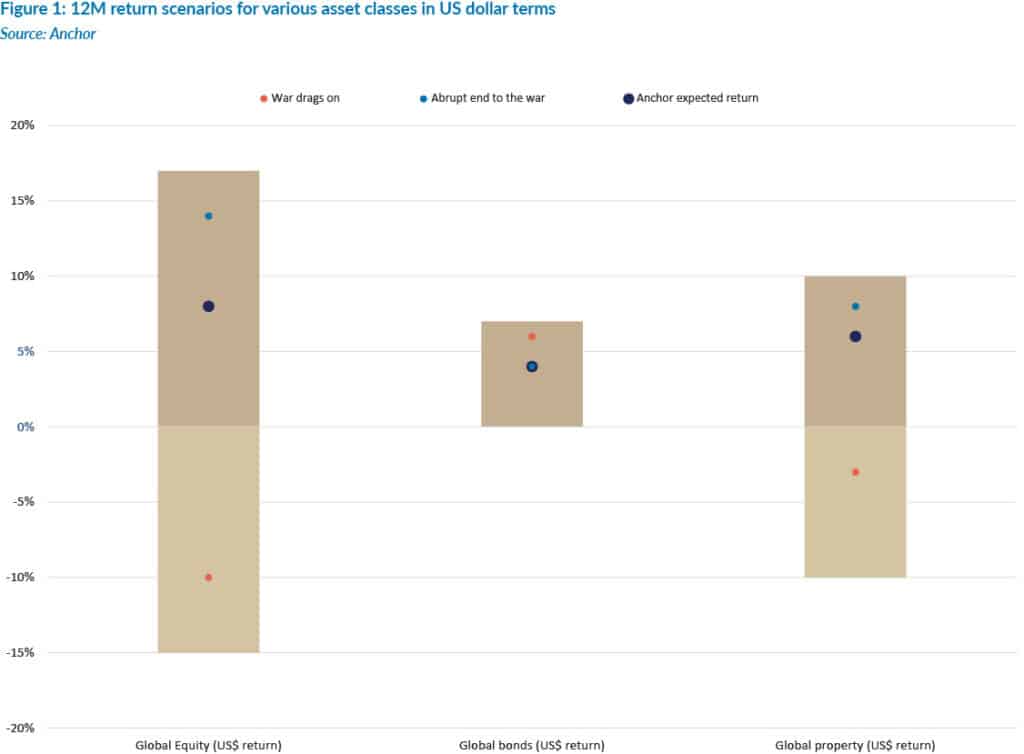

Figure 1 below highlights the US dollar return outlook for the various global asset classes. The bars in Figure 1 represent the reasonable range of possible outcomes, with the dots indicating our estimated outcomes under various scenarios. Except for alternatives (positive), we are neutral on the various asset classes, given the very high level of geopolitical uncertainty.

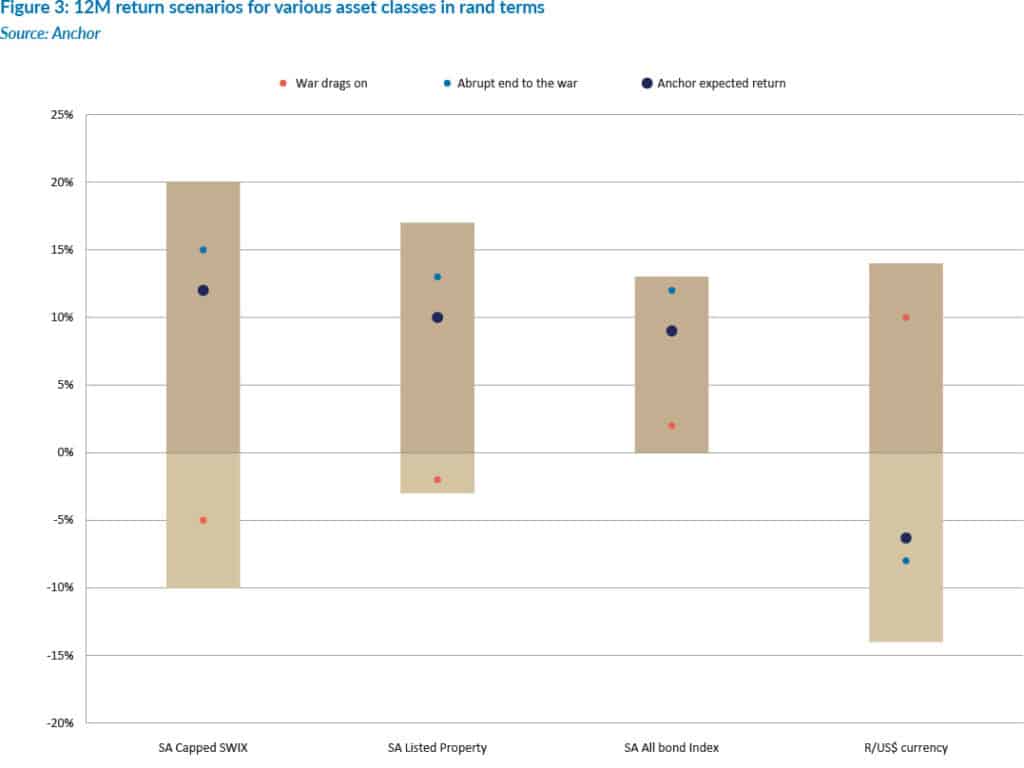

Figure 3 below outlines the rand return outlook for several domestic asset classes. The bar represents the reasonable range of possible outcomes, with the dots indicating our estimate of the outcome under various scenarios. From a domestic perspective, apart from cash (negative) and alternatives (positive), we are neutral on all asset classes, given the high level of geopolitical uncertainty.