Africa has emerged as the global centre of mobile money, with more than US$1trn in transactions processed on the continent in the past year, around two-thirds of total global volumes. This development does not reflect superior fintech innovation, but rather a structural gap: traditional banking infrastructure was never built at scale, creating space for telecom operators to fill the void.

The story is usually framed as a payments story – transaction volumes, financial inclusion milestones, the emergence of telco-led wallets. However, it is more structural than that. Telecoms operators have evolved into de facto financial infrastructure providers, leveraging extensive mobile penetration and distribution networks without the need for physical bank branch networks.

The gap (opportunity?) left by the banks

To understand why telcos could become so integral to everyday life in Africa, start with what the banks did not build. The IMF’s Financial Access Survey (last updated for 2022) shows that across Sub-Saharan Africa (SSA), banking infrastructure remains limited, averaging c. six branches per 100,000 adults. Nigeria, which has Africa’s largest population, is at c. 4.4 branches, with Kenya, one of Africa’s more developed financial markets, at the same level. Compare that to the US at 138 branches per 100,000. Africa’s branch density is not low because it is following a digital trajectory without the need for physical infrastructure, but rather because the branch network was never built to meet the demand.

What the numbers obscure is geography. Most branches are concentrated in urban centres: the Bank of Tanzania’s own data show more than half of the country’s branches are clustered in cities. Rural populations were not just underserved; they were excluded. Mobile network coverage, in contrast, exceeds 90% of Africa’s population, with reach extending well beyond urban areas.

The architecture of the solution

This disparity enabled telecom-led solutions such as Safaricom’s M-Pesa, launched in Kenya in 2007, which utilised unstructured supplementary service data (USSD) technology to deliver low-cost, accessible financial services via basic mobile devices. A user dials a short code like *123# on any phone, a live text-menu session opens on the network, the user follows the prompts, enters a PIN, and the transaction is done in 30 seconds.

USSD technology does not require the latest smartphone, internet, or banking app. All it requires is a SIM card and a GSM signal (primarily 2G and 3G networks), which is the simplest form of mobile technology. It works on every GSM handset ever manufactured and costs the user nothing in data charges. In the West African Economic and Monetary Union (WAEMU; a regional organisation of eight nations—Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo), 89% of mobile money transactions still run over USSD. Across Africa, it is closer to 64%. Given that this technology stack meets the demand, there is very little reason to upgrade.

The Safaricom model has since scaled across the continent. For example, MTN Group’s MoMo operates across 19 African markets with c. 70mn monthly active users (MAUs), processing US$500bn in transactions in 2025. Airtel Africa’s Money serves 44mn users across 14 countries, supported by an agent network that has increased by 320,000 agents in 2025 alone. Together, these operators have built a continental payments network through a common architecture: USSD on the front end, agents as the distribution, and telco infrastructure as the payment rails.

By 2025, there were 755 registered mobile money agents per 100,000 adults in mobile money markets — compared to just six bank branches per 100,000 adults across SSA. In 2024, agents cashed in US$356bn across the mobile money ecosystem. In West Africa, there are 13 times more active mobile money agents than bank branches and ATMs combined.

The clearest signal that this infrastructure has matured beyond emerging-market (EM) curiosity is when you start to see the global payments giants (Visa and Mastercard) investing in this theme. For example, Mastercard invested in MTN Group Fintech in 2024 and in Airtel Mobile Commerce in 2021.

The constraint and what unlocks it

Unfortunately, the current model is constrained by technology. While USSD is universally available and enables payments and basic services, it limits more advanced financial functionality. In a single session, a user can send money, pay a bill, or check a balance, but that is where the financial offering ends. There is, for example, no functionality to generate a loan offer or process a merchant QR code. The financial service is constrained by what the underlying technology can process.

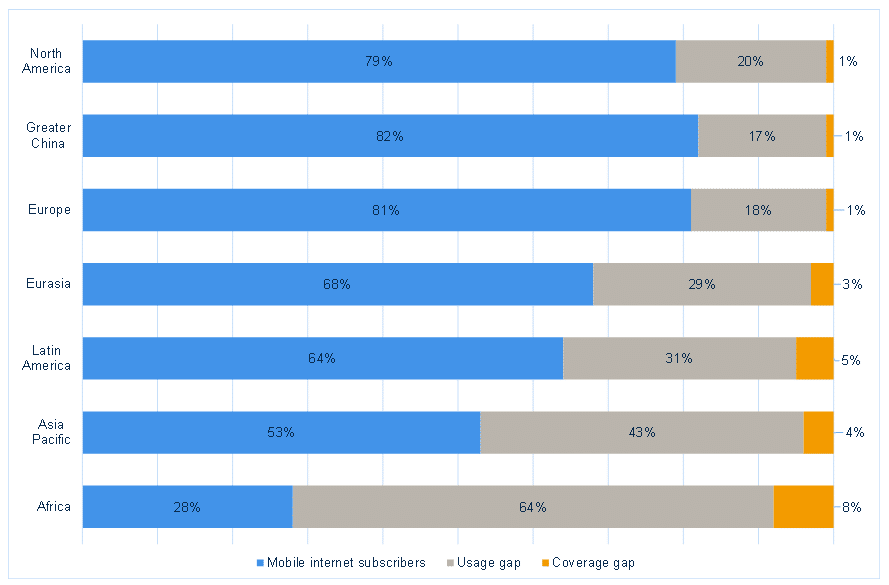

Around 64% of Africa’s population lives within mobile coverage but does not use mobile internet, the highest of any region globally, according to the Global System for Mobile Communications Association (GSMA) Intelligence. Asia Pacific’s usage gap is 43%, and Latin America’s is 31%. Africa accounts for 33% of the world’s unconnected population despite near-universal coverage. The barrier is not network coverage, but device affordability and the usage gap.

Figure 1: Mobile internet connectivity by region, % of population

Source: GSMA Intelligence, June 2025, Anchor Capital

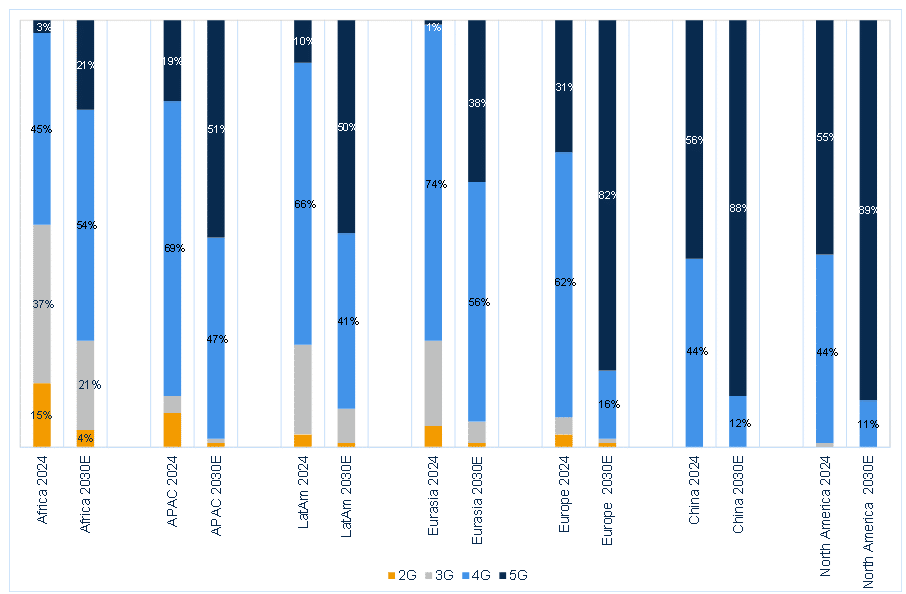

Across all African connections in 2024, 4G already leads at around 45%, and the network has largely been upgraded. However, USSD persists not because users are on 2G networks, but because most devices are still basic feature phones or low-end smartphones for which data costs money and apps require storage.

GSMA Mobile Economy 2026 puts smartphone ownership in Africa at just 24% of the population, also the lowest of any region globally. A 4G-capable handset in SSA costs around 26% of monthly GDP per capita, vs 16% across other low and middle-income countries.

Figure 2: Mobile technology mix by region, % of total connections

Source: GSMA Intelligence, June 2025, Anchor Capital

The forward picture is one of a relatively slower adoption. By 2030, GSMA forecasts Africa at 21% 5G penetration (in the last position globally), vs 89% in North America, 82% in Europe, and 88% in China. Although the trajectory is positive, the pace of change lags the rest of the world.

Addressing this constraint represents the next phase of growth. Industry initiatives aimed at lowering the cost of entry-level smartphones are expected to unlock broader access to digital financial services. In October 2025, the GSMA (working with Airtel, Axian Telecom, Ethio Telecom, MTN, Orange, and Vodacom) introduced minimum specifications for affordable entry-level 4G smartphones. The goal is simple: make a device that unlocks the next layer of financial services affordable at scale. When that happens, the 64% usage gap becomes an addressable market.

The investment angle

From an investment perspective, African telecom operators have evolved beyond just connectivity providers. Fintech revenues are growing rapidly, with increasing contributions from higher-margin financial services. For example, MTN MoMo’s fintech revenue grew 23% YoY to R29bn in 2025, with advanced services (such as credit, insurance, merchant payments) growing at 40% YoY to over R8bn. The mix shift from transfer fee revenue to financial services revenue is already underway.

Another angle that we have discussed at length is Optasia, which was listed on the JSE in November 2025 and is an AI-powered fintech company which focuses on EMs. It partners directly with mobile operators, including MTN and Vodacom, to deliver AI-driven microcredit through existing mobile infrastructure. It processes over 30mn loan transactions daily, with an average ticket size of US$5. The revenue mix tells a similar story to MTN’s: in 2019, virtually all revenue came from airtime credit extensions; by 2025, 62% came from microfinancing. Revenue grew 76% YoY in 2025 to US$265mn, well ahead of the company’s guidance.

The rails are built, and the distribution networks (agent networks) are already in place. The question is how value creation evolves as device accessibility becomes affordable and more sophisticated services are layered onto existing platforms, and who owns the infrastructure when it does.