By almost any measure, the US has the most complex and most expensive healthcare system in the developed world. Americans pay, on average, roughly three times more for branded medicines than patients in other developed nations.

The reasons are often attributed to pharmaceutical companies themselves. Certain political and consumer groups frequently accuse Big Pharma of exploiting patients through exorbitant pricing. While there is some merit to this criticism, it tells only a part of the story.

To understand why drug prices are so high in the US, one must look beyond the pharmaceutical industry itself and into the complex network of intermediaries, incentives, and structural quirks that define the US healthcare system.

The economics of pharmaceuticals

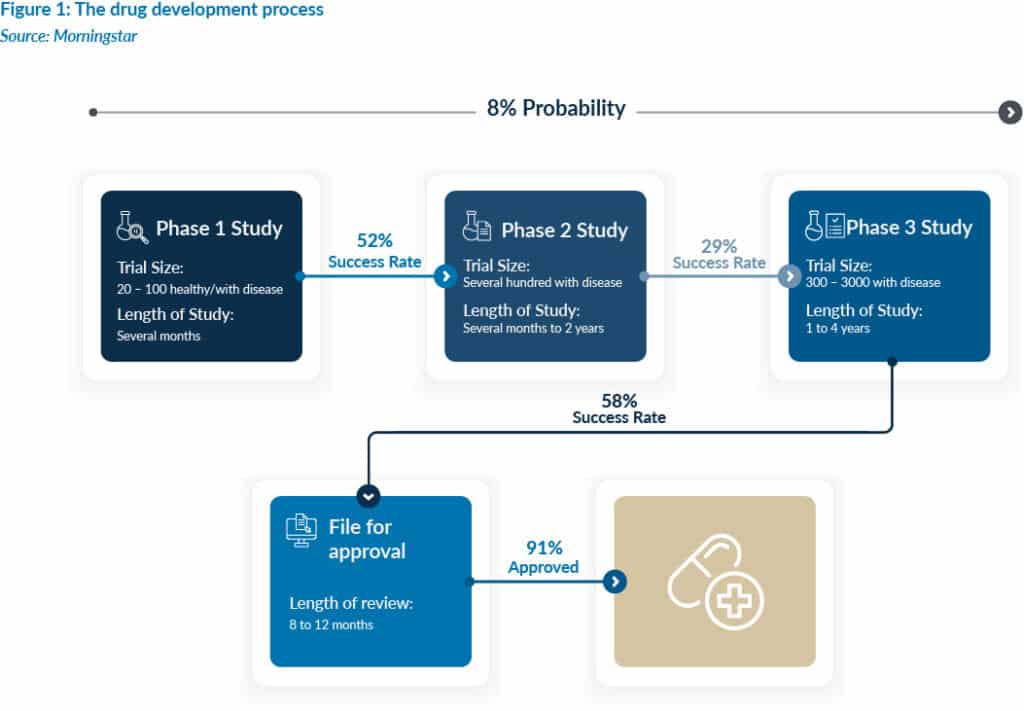

Drug development is a lengthy, risky and expensive endeavour. Pharmaceutical and biotechnology companies begin by identifying a disease-relevant biological target – typically a protein or strand of ribonucleic acid (RNA). Scientists then screen molecules to find one capable of influencing that target. Promising candidates enter preclinical testing in animals before entering the long clinical development process in humans. From discovery to approval, the journey typically takes ten to fifteen years.

Even then, success is far from guaranteed.

For every Pfizer or Eli Lilly, there exists a long tail of failed drug programmes and biotech startups. Additionally, the make-up of the healthcare system is equally, if not more, responsible for the current state of play.

Between 2021 and 2024, the probability that a drug entering Phase 1 clinical trials would ultimately receive approval from the US Food and Drug Administration (FDA) ranged between 7% to 12%. Put plainly, drug development requires a more-than-decade-long commitment with around a one-in-ten chance of success. In any industry, that is a deeply unfavourable wager.

Patent law compounds the challenge. Pharmaceutical companies usually file for protection (patents) at the pre-clinical stage, starting a twenty-year protection clock. Given that development alone consumes roughly half of that period, the window of commercial exclusivity is often less than a decade. Once a patent expires, generic or biosimilar competition enters the market quickly, and the drug’s revenue typically collapses.

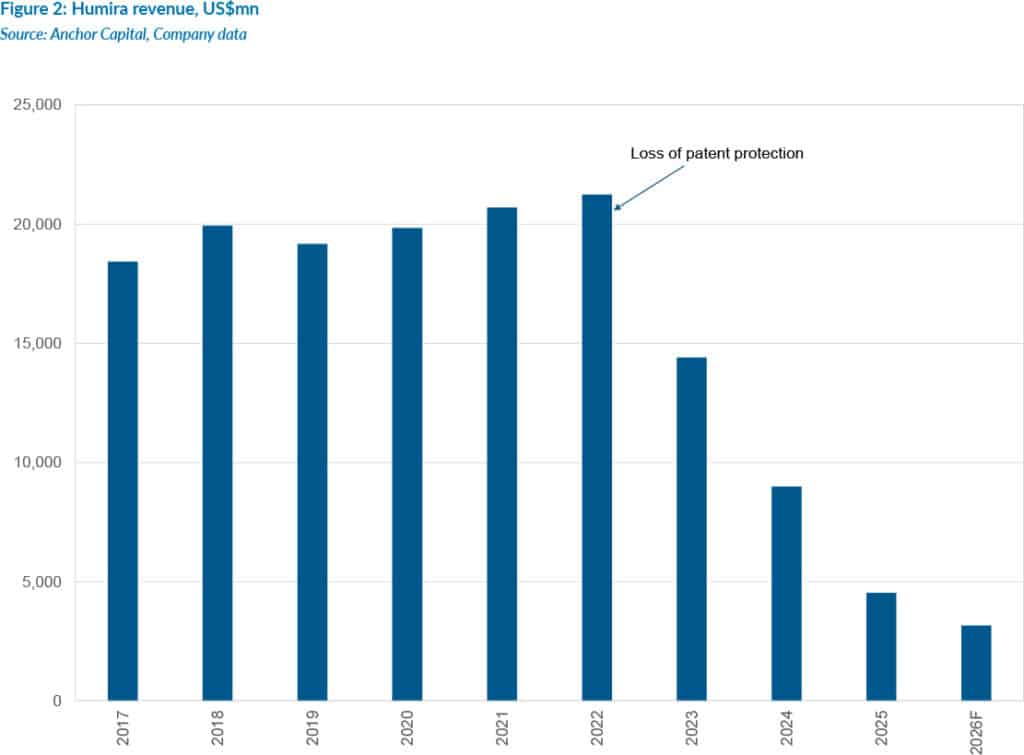

The experience of AbbVie’s blockbuster immunology drug Humira illustrates the point (see Figure 2). At its peak in 2022, Humira was the world’s best-selling drug, generating US$21bn in annual revenue. When its patent expired in January 2023, biosimilar alternatives flooded the market, and sales have fallen by c. 86% since then.

Given this dynamic, pharma companies are naturally incentivised to extract maximum economic value from an approved drug while exclusivity lasts. If the economic return is not realised, the capital required to fund new life-saving treatments evaporates.

So, while individuals can criticise the high gross margins earned by pharma companies, they often forget the sunk costs that preceded those margins.

The anatomy of a drug’s price tag

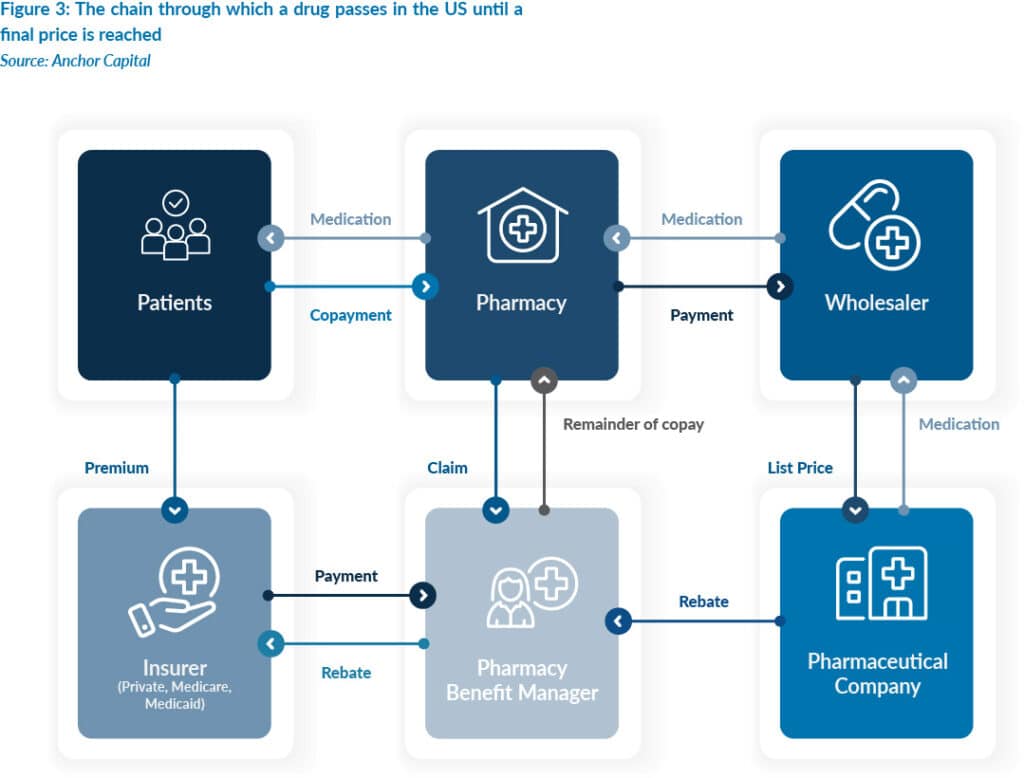

Branded drugs are expensive because they are costly to make, but this does not fully explain the pricing mismatch between the US and other developed countries. The key difference lies in how prices are negotiated. The US is that rare developed nation without a central authority to negotiate or set drug prices for its population.

Elsewhere, developed nation governments wield significant buying power. In the UK, for example, the National Institute for Health and Care Excellence (NICE) assesses whether a medicine justifies its asking price, after which the National Health Service (NHS) negotiates the final reimbursement level. Similar national frameworks exist in countries such as Australia and France. In Australia, prices are negotiated nationally and tied to a central formulary, while in France, they are set through a process grounded in therapeutic value.

In each of these markets, there is ultimately one negotiated price. The US operates very differently.

Pharmaceutical companies do set a uniform list price, but that figure is rarely what anyone actually pays. Instead, the list price serves as a starting point from which a drug passes through a chain of wholesalers, pharmacy benefit managers (PBMs), Medicare, Medicaid, private insurers, and pharmacies. Each participant in that chain negotiates its own discounts, rebates, and fees.

The final price paid by patients and insurers is therefore the product of multiple confidential transactions, with each layer of the system along the way taking its cut.

Because these downstream costs are pegged to the list price, pharma companies are incentivised to set the list price as high as possible. The high list price/high rebate system inflates what vulnerable patients pay while keeping the underlying additive transactions hidden from view.

The intermediaries who ate the system

The fragmented nature of the US healthcare system has given rise to a type of intermediary that exists nowhere else in the developed world – PBMs.

PBMs originally emerged as administrative intermediaries – processing claims and designing formularies to help employers and insurers navigate a fragmented market. Over time, however, PBMs have grown into an industry of their own, becoming powerful gatekeepers in the pharmaceutical supply chain. Today, the three largest PBMs process c. 80% of the c. 6.6bn prescriptions dispensed annually in the US.

Their core function is negotiating rebates from drug manufacturers in exchange for favourable placement on formularies – the list of medicines insurers cover. In theory, this competition should lower drug prices. In practice, it has done the opposite.

To maximise rebate revenue, PBMs have been found to favour a higher-priced drug offering a larger rebate over a cheaper alternative. In this structure, every participant benefits: insurers receive their rebate payments, PBMs collect their fee, and the pharmaceutical manufacturers retain their premium price. Everyone in the chain wins – except the patient.

The state of the nation

In recent years, administrations from both political parties have begun addressing both the manufacturer-pricing side of the equation and the role of the intermediaries. Notably, however, neither has moved to replace the system with a single national buyer of the kind seen in the UK or Australia.

The most significant reform came under the Biden administration through the Inflation Reduction Act (IRA). The legislation overturned the long-standing “non-interference clause,” which had explicitly prohibited Medicare from negotiating drug prices directly with manufacturers. The reforms introduced several important changes:

- Medicare can now negotiate prices on certain high-cost medicines.

- Annual out-of-pocket prescription costs for beneficiaries are capped at US$2,000.

- Pharmaceutical companies are now required to pay rebates to Medicare if drug prices rise faster than inflation.

Subsequent reforms under the Trump administration have pursued a complementary approach. To close the gap between US and global prices, it has moved towards international price benchmarking — linking the maximum fair price (MFP) of certain Medicare drugs to the average prices paid by other G7 nations. In doing so, the US is effectively borrowing the collective negotiating leverage of the global market.

At the same time, policymakers are targeting the intermediaries themselves. New federal transparency mandates require PBMs to disclose payments received from manufacturers. Legislative proposals are also underway to separate PBM compensation from drug list prices, removing the incentive for intermediaries to prefer branded medications (more expensive) over cheaper generics.

Where the system is heading

These reforms suggest that the “Wild West” era of US drug pricing may be coming to an end. The US is gradually moving toward a value-based pricing model, where the cost of medicines is more closely tied to their clinical benefit rather than what the market will tolerate.

Significant challenges remain. Expanding reforms beyond Medicare to all private insurance markets would represent a major structural shift. Still, the pharmaceutical industry has continued to warn that aggressive pricing controls risk creating an “innovation wasteland,” and legal challenges are likely to persist. Nevertheless, it would seem that political momentum has shifted, and the public’s appetite for the status quo has evaporated. More progress on drug pricing reform has been made over the past two years than in the preceding two decades.

For investors and policymakers, the key takeaway is that the future of US pharmaceutical pricing will likely be shaped less by the drug manufacturers themselves and more by the complex system of intermediaries that grew around them.