Figure 1: Rand vs US dollar

Source: Anchor Capital

The US Economy

The US economy was unexpectedly strong in January. Or in the words of the US Federal Reserve (Fed) Chairman Jerome Powell, during his testimony before the US Congress on 7 March, “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely higher than previously anticipated.” In short, he said that the Fed would need to raise interest rates more than expected as the US economy (particularly the labour market) remains too strong. US interest rate hikes were initially conducted in 0.75% increments, which gave way to 0.5% increments in December and 0.25% at the Fed’s most recent meeting. The Fed chairman has now opened the door for interest rate hikes to again accelerate to increments of 0.50%.

We note that US inflation has been falling, from a peak of 9.1% in June 2022 to 6.4% in January. Similarly, personal consumption expenditure ([PCE], the Fed’s preferred measure of inflation) peaked at 7% and is currently at 5.4%. The trend is in the right direction; however, the pace at which inflation is cooling is glacial, and credible economists are pondering whether an economy this robust could ever see inflation return to the Fed’s 2% target range. The clear message from the Fed is that it will do what it takes to cool the economy further, which means more interest rate hikes.

Find out more about the banking mini-crisis in the US here.

We saw through much of 2022 that US interest rate hikes are good for the dollar and bad for just about everything else. Equities, bonds and the rand reacted negatively to the Fed chairman’s testimony. The US dollar strengthened to US$1.05 vs the euro, and parity is once again within the realms of possibility. However, a strong dollar and negative sentiment towards risk assets are bad for the rand, which is also battling our homegrown issues. We started on 8 March with the rand trading at R18.61/US$1.

The rand is currently trading on global events, and Eskom’s assault on our currency is secondary for now. Where US interest rates go will dictate the behaviour of the greenback and global markets. It is difficult to project where peak rates will be, though we maintain our view that the peak most likely is not too far from current levels. We expect that the narrative of higher and higher will subside this year and be replaced by the narrative of higher-for-longer as rate-cut expectations are pushed further into the future. The market is pricing in about a 70% probability of a 0.50% US rate hike later this month, with two further hikes of 0.25% after that. That is probably about right in our view as well. Short-dated yield assets have become very attractive (do not forget about the Anchor Global High Yield Fund, which will yield over 6.5% net), and the rand has become more oversold. South Africa’s (SA’s) economic growth is being Eskom’ed down to a trickle making domestic rate hikes difficult and hurting the rand’s prospects. Nevertheless, if SA follows the US regarding rate hikes, the Anchor Core Income Fund yield will be just sub-10%. We think the SA Reserve Bank (SARB) will have no choice but to follow with higher rates.

If we are moving towards peak rates but not quite there yet, then phase into risk assets; you can never pick the bottom. The rand is likely to hover around these levels for a while but, in time, should eventually recover some of the losses like it has done every time in the past. In the short term, anything is possible, and a strong US jobs report (due on 10 March) and inflation print (due on 14 March) will see the rand test its all-time COVID lows, while a more sanguine print would auger well for a bit of recovery. Only time will tell.

Find out more about how the ZAR VS. USD exchange rate looked in 2022 here.

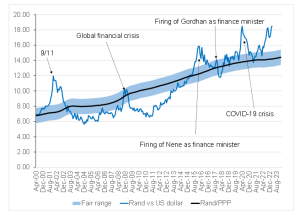

Figure 2: Actual rand/US$ vs rand PPP model

Source: Thomson Reuters, Anchor Capital

At Anchor, our clients come first. Our dedicated Anchor team of investment professionals are experts in devising investment strategies and generating financial wealth for our clients by offering a broad range of local and global investment solutions and structures to build your financial portfolio. These investment solutions also include asset management, access to hedge funds, personal share portfolios, unit trusts, and pension fund products. In addition, our skillset provides our clients with access to various local and global investment solutions. Please provide your contact details here, and one of our trusted financial advisors will contact you.