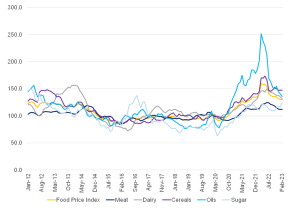

The FAO Global Food Price Index (FFPI)

The FAO Global Food Price Index (FFPI), which measures the monthly change in the international prices of a basket of food commodities, averaged 129.8 points in February 2023, down 0.6% from January and continuing its downward trend for an eleventh consecutive month. With the latest decline, the index has fallen 18.7% from its peak in March 2022. The marginal decline of the FFPI in February reflected significant drops in the price indices of vegetable oils and dairy, together with fractionally lower cereals and meat indices, more than offsetting a steep rise in the sugar price index.

Figure 1: FAO’s Global Food Price Index

Source: FAO, Anchor

In an encouraging development for global food inflation, the Initiative on the Safe Transportation of Grain and Foodstuffs from Ukrainian ports, also known as the Black Sea Grain Initiative, has been extended for another 120 days and will be reviewed again after this period. This initiative started in July 2022 and is an agreement between Russia and Ukraine made with Türkiye and the United Nations (UN) to allow grain movement from Ukraine to world markets without Ukraine being attacked by the Russian military. Since the deal was first signed into fruition, Ukraine has exported about 25mn tonnes of grains and vegetable oils – one of the primary drivers for the decline in global food prices over the past 11 months.

Overall, Ukraine remains a critical player in the global wheat market, even though its production has declined significantly due to the war. Despite the sharp decline in Ukraine’s wheat exports, the latest International Grains Council (ICG) forecast for 2022/2023 global wheat exports is at 199mn tonnes – up 1% from the previous season. In addition, Australia, Canada, the EU, Kazakhstan and Russia are expected to boost the available supplies for the world market.

This improvement in export supplies means global wheat prices could continue to moderate over the medium term. Nonetheless, the Black Sea geopolitical tone and war remain significant risks to the global grain and vegetable oil market for the foreseeable future. Extending the grain deal is a welcome development, but the period is relatively short. A longer time frame is far preferable for market players to clear uncertainty surrounding shipments for more prolonged periods. Nonetheless, the deal extension benefits all wheat- and vegetable-importing countries (particularly South Africa [SA]) as global wheat prices continue to soften.

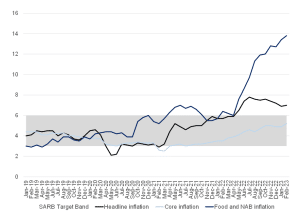

Locally, headline inflation rose slightly by 0.1-pp to 7.0% YoY in February, higher than the consensus forecast of a 6.9% YoY increase. Notably, core CPI inflation jumped more markedly by 0.3-pp to 5.2% YoY. However, the rise in core inflation was mainly driven by health insurance costs, which have started to adjust higher after two years of unusually low increases. Therefore, we do not see the rise in core CPI as reflective of a broad-based underlying price pressure that will be sustained. While upside risks remain, we expect this core CPI print of 5.2% to be the peak, and we forecast that headline CPI inflation will resume its broad easing trend from March 2023. Nonetheless, the critical risk factor for this outlook remains food price inflation, which has increased consistently for most of the past year, reaching 13.6% YoY in February. The dominant contributors were meat and fish (+3.9% YoY), bread and cereals (+3.8% YoY), dairy and eggs (+1.8% YoY), and vegetables (+1.2% YoY).

Figure 2: SA inflation, January 2019 to date (YoY, % change)

Source: Stats SA, Anchor

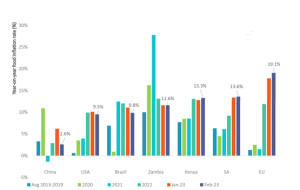

Compared to other key markets, SA’s February food inflation was lower than in the EU but higher than in Kenya, Zambia, Brazil, the US and China. Compared to January 2023, decreasing food inflation rates have been observed for China, the US and Brazil, while increasing food inflation rates have been experienced in Kenya, the EU and SA.

Figure 3: International food inflation comparison

Source: BFAP

Many factors that have driven local food inflation over the past year are not unique to SA. These include high agricultural commodity prices globally, as well as increased energy costs, which influence the prices of inputs such as fuel fertiliser. While a number of these global factors are easing, as evidenced in the continued decline in the FAO’s Food Price Index, the depreciation in SA’s exchange rate has offset much of the global decline. At the same time, persistently high levels of loadshedding added significant costs across the agriculture and food value chain. Notably, the sharp exchange rate depreciation has prevented much of the observed decline in world prices from transferring to SA.

Looking ahead, naturally, any significant appreciation in the coming months would have the opposite effect – easing domestic prices for agricultural commodities. However, this effect could lessen if loadshedding is maintained at lower levels. Unfortunately, the consensus is that loadshedding will likely remain at relatively high levels for the foreseeable future, which will, in turn, be a key factor in keeping local food prices higher for longer. For March 2023, the high base effects of March 2022 are likely to cause food inflation to moderate somewhat. Nonetheless, an increase in administered prices, such as electricity, due to be implemented in April, could further add cost pressures that, in turn, are likely to keep food prices elevated over the coming months.

At Anchor, our clients come first. Our dedicated Anchor team of investment professionals are experts in devising investment strategies and generating financial wealth for our clients by offering a broad range of local and global investment solutions and structures to build your financial portfolio. These investment solutions also include asset management, access to hedge funds, personal share portfolios, unit trusts, and pension fund products. In addition, our skillset provides our clients with access to various local and global investment solutions. Please provide your contact details here, and one of our trusted financial advisors will contact you.