Global equity markets entered June at record highs, but investor sentiment shifted as the month progressed, with markets contending with a combination of sticky inflation, uncertainty around the US Federal Reserve (Fed) leadership change, AI-valuation jitters, and Middle East peace fragility. The Iran conflict, which has roiled energy markets for the past four months, lurched through another cycle of ceasefire euphoria and military flare-ups. At the same time, the global AI/semiconductor unwind (concentrated in the Nasdaq but also spilling into Asian chip counters) ran parallel to the geopolitical newsflow. Against this backdrop, global equities experienced a modest pullback with the MSCI World Index declining by 0.8% MoM (+8.9% YTD/+13.3% 2Q26). Still, towards the end of June, improving sentiment around US-Iran tensions and renewed strength in mega-cap technology shares helped markets recover some of their earlier losses.

US economic data released in June reflected a mixed picture. May headline inflation accelerated to 4.2% YoY vs April’s 3.8% print, the highest since April 2023. Core inflation, which excludes food and energy, increased to 2.9% YoY from 2.8% previously, well above the Fed’s 2% target. The data indicated that much of the inflation surge came from a 3.9% YoY jump in energy prices, putting the 12-month increase at 23.5%. May core personal consumption expenditure (PCE), excluding food and energy, the Fed’s preferred inflation gauge, climbed 3.4% YoY, vs April’s 3.3%. Despite inflation pressures, US economic growth remained resilient. Final 1Q26 GDP data showed the economy expanded at an annualised pace of 2.1%, ahead of previous estimates. At its June meeting, Trump appointee Kevin Warsh’s first as chair, the Fed held rates steady but updated quarterly projections highlighted that nine Fed officials anticipate a rate hike by the end of this year.

A rotation away from tech stocks gathered momentum, with AI capex concerns and macro risks driving US equity market volatility. The tech-heavy Nasdaq fell by 2.8% in June but recorded an impressive 2Q26 (+21.4%) and its best first half since 1986 (+12.8% YTD). The S&P 500 also declined (-1.1% MoM), as investors shifted towards defensive and industrial sectors, but posted its strongest first-half performance since 2021 (+9.6% YTD) and its largest quarterly gain since 2020 (+14.9% in 2Q26). The Dow was the strongest performer among the major US indices, gaining 2.5% in June and reaching a record high (it has notched 19 record highs to end June 2026). The Dow also posted its best 1H performance since 2021, jumping 8.9% (+12.9% in 2Q26).

European equity markets tracked the global AI/tech sell-off and ceasefire headlines closely but were somewhat cushioned by less tech exposure vs their US counterparts. The Euro Stoxx 50 rose 4.6% MoM (+9.3% YTD/+13.6% 2Q26), while France’s CAC advanced 2.7% MoM (+3.1% YTD/+7.5% 2Q26), and Germany’s DAX declined by 0.4% MoM (+2.1% YTD/+10.2% 2Q26). May eurozone inflation rose to 3.2% vs April’s 3.0%, again primarily driven by energy price inflation (+10.9% YoY). As a major net energy importer, Europe is especially vulnerable to energy shocks.

June was another volatile month in UK equity markets, with the FTSE 100 advancing only 0.8% (+5.7% YTD/+3.2% 2Q26). May UK inflation was unchanged at 2.8% YoY as slowing food prices offset rising transport costs. In late June, UK Prime Minister Keir Starmer announced his resignation as Labour Party leader, following mounting political pressure, internal party disputes, and a collapse in approval. He is the sixth British PM to have resigned in the past decade – an unprecedented era of political instability following the 2016 Brexit referendum.

In China, equity markets were more mixed and choppier, with mainland China outperforming Hong Kong as the Hang Seng saw a sharp reversal from its strong 2025 performance, largely on the back of the same AI/semiconductor derating hitting US and European markets. The Shanghai Composite was up 0.6% MoM (+3.2% YTD/+5.2% 2Q26), but the Hang Seng dropped by 9.1% MoM (-10.7% YTD/-7.7% 2Q26). June’s official manufacturing Purchasing Managers’ Index (PMI) printed at 50.3 vs May’s 50, above the 50-point mark that separates expansion from contraction. Non-manufacturing PMI, including services and construction, came in at 50.2 vs 50.1 in May.

Japan was again the standout performer, largely shrugging off the mid-June AI wobble as the benchmark Nikkei soared 5.6% (+39.2% YTD/+37.2% 2Q26), hitting fresh highs repeatedly during June. The equity market’s resilience has been underpinned by AI/semiconductor-related strength (memory chips especially), fiscal stimulus, and corporate reform tailwinds that have outweighed other concerns. Headline inflation printed at 1.5% in May vs April’s 1.4%. The Bank of Japan hiked rates to 1%, the highest level since 1995, as yen and inflation worries take hold.

Brent crude oil ended June 20.8% lower MoM (+19.8% YTD/-38.5% 2Q26) at US$72.92/bbl. Crude prices initially tumbled on easing supply concerns as more oil tankers transited the Strait of Hormuz, but renewed attacks between Iran and the US late in the month ignited oil price concerns before prices slipped again at month-end as tensions eased after the two countries agreed to halt hostilities. Gold (-11.7% MoM/-7.2% YTD/-11.6% 2Q26) was notably weaker while platinum group metals (PGMs) remained under pressure. Platinum dropped 19.1% MoM (-24.7%YTD/-20.6% 2Q26), with palladium down 10.9% MoM (-25.2% YTD/-17.9% 2Q26) and rhodium falling by 11.9% MoM (-15.5% YTD/-24.0% 2Q26).

The JSE underperformed in June, with the FTSE JSE All Share Index declining by 3.8% (-4.8% YTD/-3.3% 2Q26). The weakness was largely concentrated in resources stocks, where precious metals counters were the biggest losers as geopolitical risk premiums unwound and commodity prices declined (Resi-10 -16.4% MoM/-15.6% YTD/-20.0% 2Q26). Large index constituents such as Sibanye Stillwater (-28.6%), South32 (-20.1%), Harmony Gold (-15.6%), Gold Fields (-14.1%), and BHP Group (-5.9%) ended June significantly lower. These losses offset firmer property, financial and industrial counters. In contrast, domestic-focused sectors performed better. The SA Listed Property Index bounced 3.3% MoM (+2.3% YTD/+8.1% 2Q26), financials firmed 2.6% MoM (Fini-15 +5.3% YTD/+6.2% 2Q26), and industrials rose 1.9% MoM (Indi-25 -6.0% YTD/+3.6% 2Q26). The rand weakened by 1.0% MoM (+1.1% YTD/+3.3% 2Q26) against the US dollar, reflecting lower precious metals prices and a stronger greenback.

SA headline inflation rose to 4.5% YoY in May, up from 4.0% in April. The increase reflects the ongoing pass-through of the global oil price shock into domestic prices. Core inflation, excluding food, fuel and energy, climbed to 3.8% YoY from 3.6%. Real GDP growth edged higher to 0.5% QoQ in 1Q26, up from 0.4% in 4Q25, while annual growth accelerated to 1.9% YoY. The outcome exceeded market expectations of 0.3% QoQ and 1.8% YoY growth, respectively, indicating slightly stronger-than-anticipated economic momentum in the early part of this year.

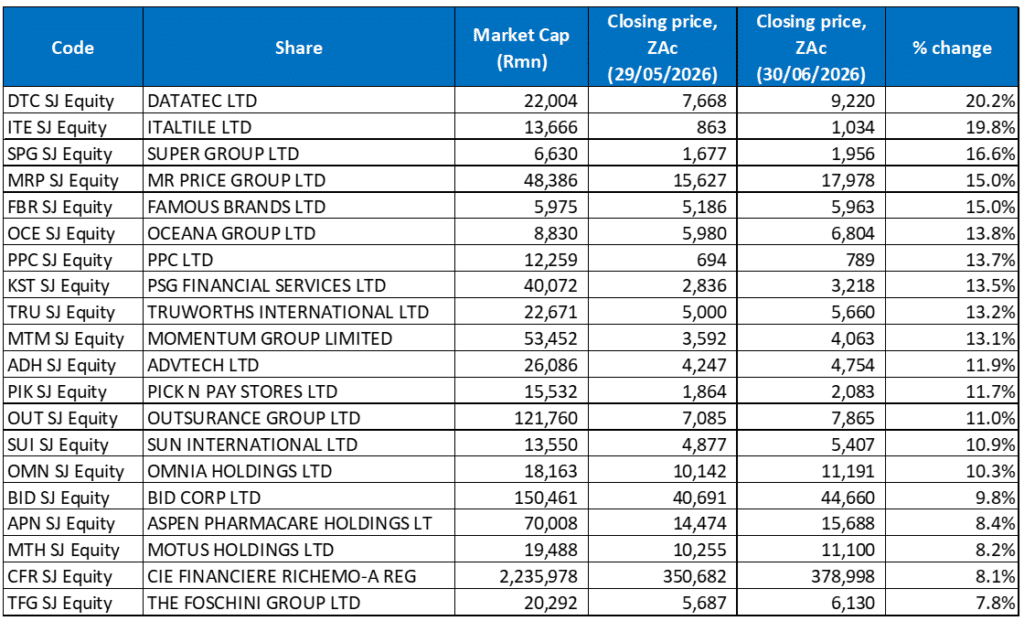

Figure 1: The 20 best-performing shares in June 2026, MoM % change

Source: Bloomberg, Anchor Capital

June saw SA Inc. shares, including oversold retailers and banking counters, performing well, buoyed by a c. 21% MoM collapse in the oil price, following the Islamabad Memorandum. Energy and commodities counters were the month’s biggest losers as the energy-driven inflation shock that had dominated SA’s macro backdrop since February began to roll over.

Datatec (+20.2%) was June’s best-performing share, driven by company-specific factors. It started the month on a positive footing following impressive FY26 results reported on 26 May, which showed that its headline earnings per share (HEPS) rose 56.5% YoY to USc39.9 on gross invoiced income of US$8.5bn. The increase was driven by AI-fuelled demand for cybersecurity and network infrastructure through its Westcon and Logicalis divisions. The Datatec share price rise accelerated during June after it announced a special dividend of up to R7.1bn, arising out of the proceeds from a major refinancing deal that positions the Group well to scale up operations. Datatec subsidiary Westcon International had reached agreement with US private equity firm General Atlantic for the refinancing of Westcon and a minority investment in the unit. Proceeds from the various transaction components will generate cash proceeds of c. US$434mn for Datatec, positioning it well to scale up its operations.

Tiles, flooring and home finishing retailer Italtile (+19.8%) was second, with diversified logistics, dealership and fleet management company Super Group (+16.6% MoM), which is listed on the JSE and in the US, in third place. As the US-Iran “ceasefire” took hold and oil prices fell, the SA consumer is set for meaningful relief, and as a housing-linked discretionary retailer sensitive to interest rate and consumer confidence cycles, Italtile re-rated sharply on improved affordability expectations. Renovation activity tends to improve when rates look like they are peaking or falling. Lower oil prices are also positive for a logistics-heavy business like Super Group through reduced fuel costs and improved margins. The US/Iran ceasefire has also improved global supply chain confidence, supporting the outlook for its international logistics divisions. In May, Super Group released robust 1Q26 earnings, posting revenue of US$612mnn and a net profit of US$86mn. The company also reaffirmed full-year guidance of over US$2.55bn in revenue and US$680mn in adjusted EBITDA.

MR Price, Famous Brands, and Oceana Group rose by 15.0%, 15.0%, and 13.8% MoM, respectively. Value clothing, homeware and accessories retailer Mr Price’s share price jumped after it released resilient FY26 results in June and reported market share gains for the period. Total revenue increased by 4.2% YoY to R42.7bn, and HEPS growth of 7.7% YoY was achieved in a volatile trading environment. In addition, lower oil prices, a firmer rand, and the prospect of falling inflation feed directly into consumer spending power for MR Price’s core lower-to-middle income customer base. The same is true for Famous Brands. Its restaurant franchises are highly exposed to consumer disposable income and food input costs, both of which improve materially when the oil price falls and the rand strengthens. Lower fuel costs also reduce distribution costs across its supply chain. Fishing and food products Group, Oceana, also benefits from lower fuel costs (fishing is extremely energy-intensive) and an improving consumer spending environment.

Cement producer. PPC (+13.7%) delivered a second consecutive year of financial turnaround in its FY26 results, released last month, with a step-change across all its key financial metrics and despite muted domestic cement sales volume growth. PPC’s FY26 revenue rose to R10.26bn from R9.87bn recorded in FY25, while diluted EPS increased by 75.0% YoY to ZAc56.00. The strong performance led to a dividend of R469mn – a 72% YoY jump. This follows the first two years of the implementation of PPC’s “Awakening the Giant” turnaround plan.

PSG Financial Services (+13.5%), Truworths (+13.2%), and Momentum (+13.1%) accounted for the remainder of the JSE’s ten best-performing shares. Truworths also benefitted from the lower-income consumer relief story, as the June oil price drop drove a sector-wide re-rating of SA domestic retailers as the inflation outlook improved sharply. Finally, insurer and financial services Group Momentum reported stronger earnings and higher new business volumes for the nine months to end March. However, it said that pressure on new business margins persisted (the value of its new business was down 4% as the margin contracted from 0.6% to 0.5%) as its product mix in parts of the business continued to shift. Normalised HEPS rose 20% YoY to ZAc414, with share buybacks helping to boost a solid performance. Recurring premiums rose by 7% YoY, and single premiums were up 15%.

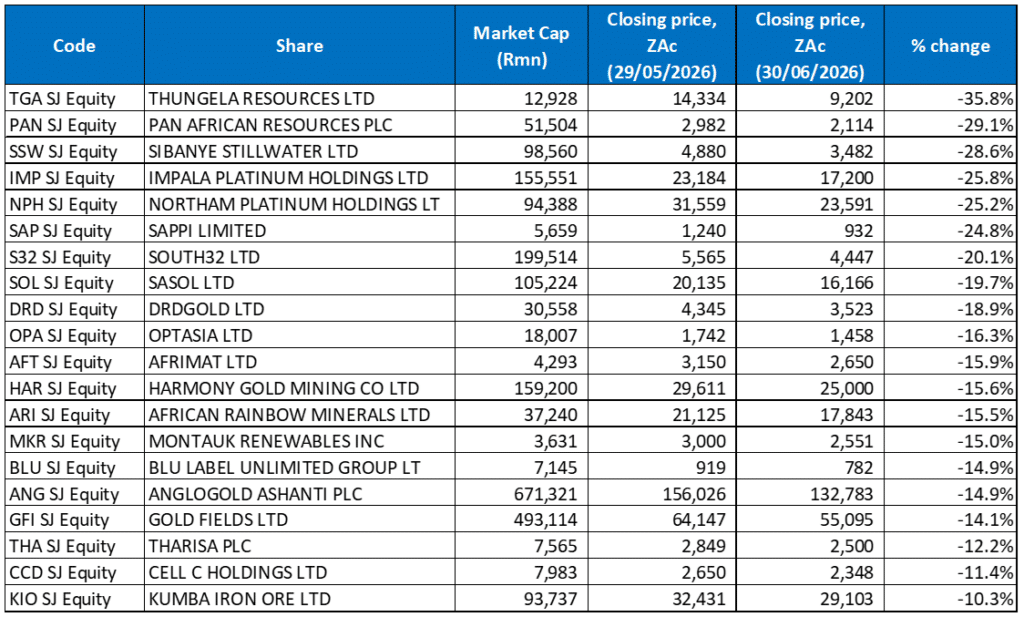

Figure 2: The 20 worst-performing shares in June 2026, MoM % change

Source: Bloomberg, Anchor Capital

Precious metals counters were the weakest sector by some distance, reflecting a further pullback in gold and PGM prices through June. Beyond precious metals, Sasol shares came under renewed selling pressure as oil retreated sharply on optimism around the Iran peace deal framework.

Thermal coal exporter Thungela Resources (-35.8% MoM) was June’s worst performer by some distance. Thungela was up 49.3% in the year to end May as coal rallied sharply during the Iran war as a substitute energy source. However, with a ceasefire taking hold and oil prices dropping, the price of coal retreated in tandem, removing the war premium that had buoyed Thungela’s share price. The share declined despite Thungela highlighting a robust operating performance and strong cash generation for the six months to 30 June in a pre-close statement released this week.

Thungela was followed by Pan African Resources (-29.1% MoM) and Sibanye Stillwater (-28.6% MoM) in second and third place. At the start of June, Pan African Resources released an FY26 operational update, which showed that gold production rose 40% YoY. However, this was at the lower end of the company’s guidance and largely driven by a slower-than-anticipated production ramp-up at its Tennant operations, triggering a sharp sell-off in the share. This, combined with the much weaker gold price, weighed on the counter in June. Sibanye Stillwater is exposed to both gold and PGMs. PGM miners including Sibanye had surged on the April ceasefire news, meaning they had already rallied hard earlier in the conflict cycle. In June, following the signing of the Islamabad Memorandum of Understanding (MOU), platinum and palladium prices fell on reduced safe-haven demand and expectations of recovering automotive supply chains. The war-premium that had propped up platinum (given fears over SA supply disruption) deflated rapidly. Sibanye is the most leveraged and diversified of the PGM majors, but ironically also felt the most pain in June.

Implats, Northam Platinum, and Sappi Ltd followed with MoM declines of 25.8%, 25.2%, and 24.8%, respectively. Implats and Northam are both pure-play PGM miners, and with PGM prices recording double-digit declines on improved supply confidence, a strong US dollar and Fed rate hike expectations, both re-rated sharply lower. The platinum price, which had hit an all-time high of US$2,923/oz on 26 January 2026, ended June at US$1,561.56/oz – down 47%.

Diversified miner South32, which is heavily exposed to manganese, aluminium, copper, and coal, was down 20.1% MoM. The coal element (South32 owns Illawarra Metallurgical Coal) suffered the same ceasefire-driven unwinding as Thungela, while base metals also softened on demand uncertainty, weighing on the share price. Sasol, DRDGold, and fintech platform Optasia rounded out June’s worst-performing shares, declining by 19.7%, 18.9% and 16.3% MoM, respectively. Sasol came under renewed selling pressure as crude oil prices retreated sharply on optimism around the Iran peace framework, falling below US$85/bbl and then continuing lower, with Sasol shares slipping toward and then through the R200 level. Sasol’s 2026 re-rating had been predicated on elevated oil prices, and this collapse has removed that fundamental pillar. DRDGold is a gold retreatment specialist with high operating leverage to the gold price; thus, as safe-haven gold sold off on ceasefire news, DRD, as a smaller, more volatile gold counter, amplified the move. Optasia’s decline seems to have been primarily driven by the temporary suspension of its airtime and data credit services in Nigeria. The suspension has since been lifted, with the underlying regulations remaining suspended pending the outcome of ongoing legal proceedings.

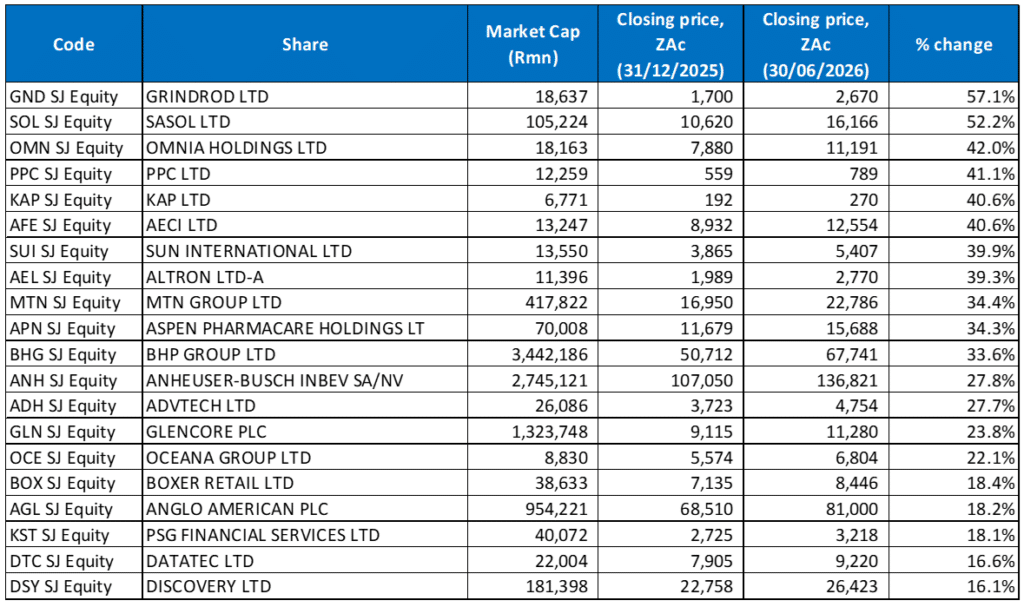

Figure 3: The 20 best-performing shares YTD, % change

Source: Bloomberg, Anchor Capital

Fifteen of the 20 best-performing shares YTD were unchanged from the year-to-end-May, as gold and PGM counters continued to be pushed out following another volatile month. Two dominant macro themes defining these shares are direct or indirect leverage to the energy (oil) shock that has defined markets this year and fundamental earnings delivery (the winners tended to have company-specific results momentum that held even as the Iran premium deflated).

Logistics and port terminals operator Grindrod’s (+57.1% YTD) bumped Sasol from the top spot, emerging as the best performer to end June. Its share price gains have been driven by a strong company-specific results story, port throughput recovery and rand-hedge earnings from its shipping operation. Grindrod has experienced record throughput at the Port of Maputo, and the ongoing rollout of rail reform in SA, which is opening third-party access to the country’s national rail network and expanding Grindrod’s operational footprint and growth pipeline, is likely also benefitting sentiment. Grindrod has continued to re-rate throughout 1H26 as the market recognised the quality of its port concession extensions (Maputo concession extended to 2058) and the Terminal de Carvão da Matola expansion pipeline targeting 12mn tonnes by 2027.

Sasol, in second place, entered 2026 with its share price at around R106, already in a multi-year downtrend. However, the closure of the Strait of Hormuz changed everything, and the share price has climbed 52.2% YTD despite dropping by nearly 20% in June to R161.66 as oil prices retreated on easing Iran tensions. The 2026 oil shock has rescued Sasol from what had been a near-terminal valuation, even if the ceasefire has since partially unwound these gains.

In third spot, Omnia Holdings is up 42.0% YTD. The chemicals and agricultural inputs Group’s raw material and energy input costs (primarily natural gas-derived ammonia and nitrates) have also benefitted from the Iran conflict. As gas prices increased, Omnia’s fertiliser pricing also rose, and it hedged energy costs effectively. Strong agricultural demand globally (driven in part by food security concerns during the conflict) has further supported fertiliser volumes and pricing.

PPC (discussed earlier), KAP Industrial and AECI have recorded YTD gains of 41.1%, 40.6%, and 40.6%, respectively. KAP’s polymer division has benefitted from oil price volatility (which influences petrochemical feedstock costs), while its logistics and timber operations have been advantaged by improving domestic conditions. Meanwhile, AECI’s speciality chemicals benefitted from tighter global supply chains. Both these shares entered 2026 at historically cheap valuations.

Sun International (+39.9%), Altron (+39.3% YTD), MTN Group (+34.4% YTD), and Aspen Pharmacare (+34.3% YTD) rounded out the ten best performers YTD. Altron is one of the JSE’s most credible domestic tech plays. It operates across managed services, digital transformation, its own platforms and its fintech and healthtech businesses. The company reported a hike in its FY26 dividend and a special R500mn dividend payout in May. Although FY26 Group revenue advanced by only 1% YoY to R9.6bn, it recorded a 34% YoY jump in HEPS, driven by technology services demand. Altron has undergone a three-year strategic overhaul that its CEO set out in 2023, and which has shifted the Group decisively towards its platform business. In the case of MTN, a major contributor to the improved outlook is MTN Fintech’s strategic partnership with Ant International, a leading digital payments and financial technology provider. The collaboration, which will initially launch in Nigeria, aims to enhance MTN’s Mobile Money (MoMo) platform into a comprehensive super-app offering financial services, lifestyle applications and digital commerce.

Finally, Aspen has benefitted from multiple tailwinds this year, including strong demand for its sterile injectables and branded medicines, and a partial rand weakening that boosted the rand-translation of its international earnings. At the end of May, Aspen’s share price jumped after it announced the completion of the R27bn sale of its Asia Pacific business. The move marks a milestone in the Group’s strategy to realise value, with the proceeds from the AUD2.37bn transaction expected to strengthen Aspen’s balance sheet and provide improved financial flexibility.

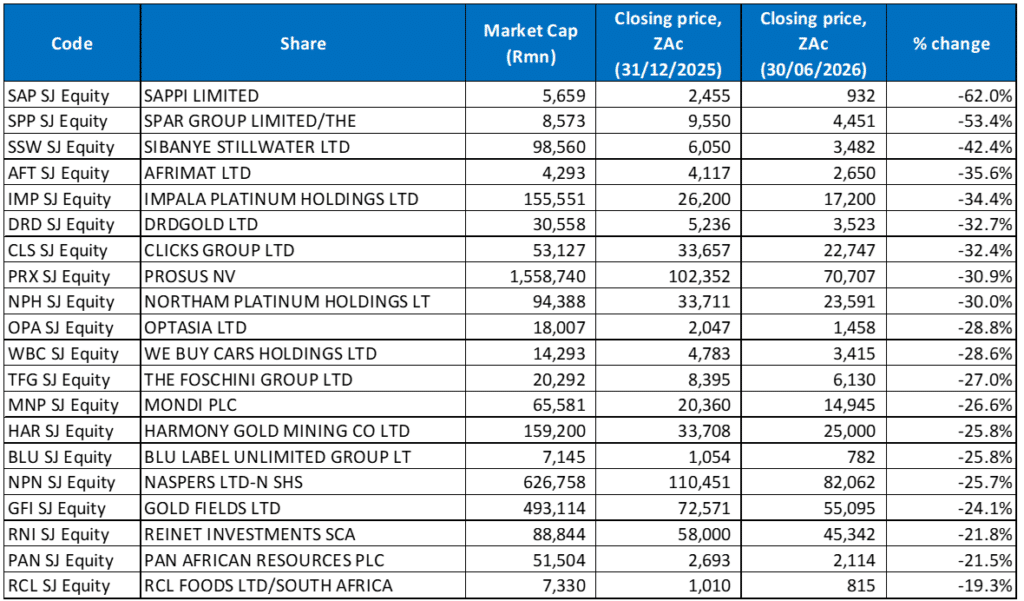

Figure 4: The 20 worst-performing shares YTD, % change

Source: Bloomberg, Anchor Capital

Most of the YTD worst performers share a common vulnerability – SA consumer-facing businesses at a time of acute and sustained cost pressures and precious metals miners. In addition, the YTD losers include a distinct cluster of company-specific failures (Sappi’s pulp market collapse, SPAR’s operational issues, May’s Prosus/Naspers’ iFood warning) that had nothing to do with Iran, a stark reminder that the macro story, however dominant, never tells the whole JSE picture.

Sappi was once again the worst-performing share YTD – down 62.0%. The global paper and pulp Group’s 2Q26 results included a US$413mn (c. R6.7bn) net loss driven by impairments, falling pulp prices, weak global demand, and adverse currency movements. Adjusted EBITDA collapsed to US$52mn from US$107mn in 2Q25, and management warned conditions could deteriorate further. The multi-year decline (the stock has fallen over 75% over the past five years) reflects a secular weakening in graphic paper demand that the company has not yet offset through its transition to packaging and bio-based materials.

SPAR Group (-53.4% MoM), in second place, has been under pressure due to operational challenges following its troubled SAP system implementation, continued weakness in its European business, and consumer pressure across multiple geographies, which has compounded an already difficult turnaround story. In late May, it released a 1H26 profit warning where the retailer flagged that HEPS would decline by up to 60% YoY, driven by deep margin compression, rising operational costs, legacy issues, and executive changes. SPAR also faces intensifying competition from Shoprite/Checkers and rising input costs that it has struggled to pass through to consumers.

In third place, Sibanye Stillwater (-42.4% YTD; discussed earlier) has been caught in a perfect storm. Starting from an already-challenged position, the company has faced persistent operational difficulties, high debt, and weak PGM prices since 2023. Its US palladium operations (Stillwater) remain loss-making at current prices, and the domestic SA business has required painful restructuring.

Afrimat, Implats, DRDGold, and Clicks Group followed with YTD declines of 35.6%, 34.4%, 32.7%, and 32.4%, respectively. Afrimat, a diversified miner exposed to iron ore, anthracite and construction materials, has been negatively impacted by iron ore price volatility and risk-off sentiment towards smaller mining names. Iron ore prices have weakened on China demand uncertainty throughout 2026, and anthracite/coal has faced the same ceasefire-driven unwind as thermal coal. Afrimat also had company-specific concerns: its pivot into bulk commodities via iron ore created concentrated commodity price risk at exactly the wrong time. The most notable non-commodity name on the losers list, Clicks, had re-rated to a very high valuation multiple during 2024–2025, pricing in consistent double-digit earnings growth. In 2026, rising energy costs compressed consumer disposable income, threatening Clicks’ volume growth assumptions. Clicks has also faced competition concerns as pharmacy rivals expanded.

Prosus (-30.9%), Northam (-30.0% YTD; discussed earlier), and Optasia (-28.8% YTD; discussed earlier) rounded out the YTD worst performers list. Prosus delivered an impressive FY26 financial performance with continued momentum across its global portfolio as revenue increased 57% YoY to US$9.7bn, while EBITDA surged 84% YoY to US$1.3bn. This follows the implementation of its “ecosystem” strategy a year ago, which has grown the business substantially. Still, despite the positive earnings report, the Prosus share price is down YTD primarily because its largest investment, Chinese tech giant Tencent, has declined by c. 28% over the same period on increased concerns over its AI strategy.