The perceived market anomaly known as the October effect, which says markets usually decline in October (as happened with the 1929 stock market crash, 1987’s Black Monday, 2002’s bursting of the Internet bubble and the 2008 global financial crisis, where the bear market started on 9 October), was most at play during the last week of the month, as volatility reigned ahead of this week’s US Presidential Election. Uncertainty over what the election will hold for markets and economic policy, a breakdown of US fiscal stimulus talks, investor concerns over surging COVID-19 cases and deaths in parts of Europe and the US, as well as announcements of fresh lockdowns in Europe (the UK, France, Belgium and Greece have all announced second lockdowns, while stricter measures were introduced in Spain and Italy) and the implications for economic activity, weighed on major global markets. In addition, the usually reliable and high-flying, large-cap tech stocks, which had led markets higher after the start of the pandemic in March, released earnings reports which investors perceived as being disappointing, resulting in the share prices of big tech names such as Apple, Amazon, and Facebook losing ground.

The three major US indices all recorded MoM declines, the S&P 500 ended lower for a second straight month (-2.8%), with the tech sector the worst performer among the S&P 500’s 11 sectors. However, YTD the S&P 500 is still up 1.2%. The Dow Jones Industrial Average (Dow) closed October 4.6% lower, its worst month since March 2020. The Dow is now down 7.1% YTD. The usually reliable Nasdaq registered its second MoM decline (-2.3%) but is still up 21.6% YTD.

On the economic data front, there was some positive news as US GDP rose by a record 7.4% in 3Q20, a sharp turnaround from 2Q20’s 9% drop albeit from a low base as 2Q20 was the quarter when the US saw COVID-19 related business closures. Still, expectations remain that the full-year growth number will show a contraction. On a more sombre note, the US Labor Department said last week that another 751,000 people had filed for unemployment insurance the previous week, indicating that new layoffs are continuing. In addition, c. 22.6mn Americans continue to receive some type of unemployment benefit. US consumer confidence declined in October after September’s sharp rise. The Conference Board reported that the index’s headline number stood at 100.9 – a decrease from the final reading of 101.3 for September. After four consecutive months of growth (including an 8.8% MoM surge in August), pending home sales declined by 2.2% for September.

European markets were sharply down in October as a second wave of COVID-19 infections saw some European countries reimpose restrictions including further lockdowns, which are expected to limit the region’s economic recovery from the first wave of the pandemic. UK equity markets were also under pressure, with the FTSE 100 Index dropping 4.9% last month (-26.1% YTD). Germany’s Dax plummeted 9.4% MoM (-12.8% YTD), while France’s CAC fell by 4.4% MoM (-23.1% YTD). On the economic data front, 3Q20 euro area GDP grew by 12.7% QoQ – a sharp rebound from 2Q20’s 11.8% decline. At its meeting last week, the European Central Bank (ECB) kept rates unchanged but said that the region’s economic outlook had darkened notably, with ECB President Christine Lagarde signaling that further monetary easing was likely to be announced at the ECB’s December meeting.

In Asia, Japan’s Nikkei closed October 0.9% lower MoM and the index is now down 2.9% YTD. China’s Shanghai Composite Index rose by 0.2% MoM (up 5.7% YTD) and Hong Kong’s Hang Seng jumped 2.8% MoM (-14.5% YTD). China’s economic recovery continued in October with expansion in the country’s manufacturing sector as the official manufacturing PMI rose to 51.4 vs 51.5 in September. The private Caixin/ Markit PMI came in at 53.6 – its highest level since January 2011 (above 50 indicates expansion and below 50 contraction). China’s 3Q20 GDP growth also accelerated to 4.9% vs a contraction of 6.8% in 1Q20 and 3.2% growth in 2Q20.

On the commodities front, iron ore prices came under pressure, falling c. 3% MoM, on the back of weak sentiment resulting from high iron ore port inventories and low margins at Chinese steel mills. Nevertheless, the steel-making ingredient is still c. 29% higher YTD. The platinum price was 6.5% lower MoM, while the gold price declined (-0.4% MoM) for a third consecutive month, although the price of the yellow metal is still up 23.8% YTD. Crude oil prices ended October c. 8.5% lower (-43.2% YTD), reaching $37.46/bbl by month-end. The oil price came under pressure largely on the back of demand concerns due to the increasing COVID-19 cases in the US and Europe, as well as additional restrictions in some European countries, which the market seems to be interpreting as a reason that oil demand could remain lower for longer.

In South Africa (SA), the FTSE JSE All Share Index ended October 4.8% in the red (-9.5% YTD), as the local market tracked major global equity markets lower. Among the index’s large-cap constituents, British American Tobacco (-13.4% MoM), BHP Group (-13.0% MoM), Richemont (-9.9% MoM), Glencore (-8.0% MoM), and Annheuser Busch InBev (-7.0% MoM), recorded significant share prices drops, while Naspers and Prosus rose by 6.8% and 5.5% MoM, respectively. The Resi-10 plummeted 11.4% MoM (-3.9% YTD), followed by the Fini-15, which was down 6.1% MoM (-39.7% YTD). The Indi-25 closed in positive territory, recording a slight gain of 0.3% MoM (+6.0% YTD), pulled higher by positive performances from Naspers and Prosus. The rand ended the month at $16.24/US$1 – up c. 3% vs the greenback, although YTD the local unit is still down c.16% against the dollar.

On the economic data front, September annual consumer price inflation (CPI) fell to a three-month low of 3.0% YoY – barely within the SA Reserve Bank’s 3% to 6% target range and a decrease from August and July’s 3.1% and 3.2% YoY annual inflation rate. MoM, inflation rose 0.2% – unchanged from the previous month, with price gains largely driven by the higher costs of alcoholic beverages and tobacco, housing, and utilities as well as food and non-alcoholic beverages. Core inflation, which excludes food, non-alcoholic beverages and fuel and energy prices, was unchanged from August’s 3.3% print.

Finance Minister Tito Mboweni delivered his Medium-Term Budget Policy Statement (MTBPS) on 28 October, highlighting both the need for fiscal consolidation and the high execution risk present. On the positive side, government reiterated its commitment to reducing spending growth, shifting spending patterns, and stabilising the country’s debt-to-GDP ratio in the medium term and categorically ruled out prescribed assets and debt-funded spending to try and stimulate the economy. Unfortunately, there were also negatives in the speech starting with SAA, which received yet another bailout (largely funded by cuts in basic service provisions) to fund its business rescue process and, in our view, setting an uncomfortable precedent with regards to the government’s handling of problematic state-owned enterprises. The Land Bank also received a further R7bn bailout – quite sizeable when considered against the recent R3bn bailout of the same entity.

Prior to the MTBPS, President Cyril Ramaphosa announced government’s Economic Reconstruction and Recovery plan, which Treasury expects to help raise growth to c. 3% on average over the next decade. Very little of what he said was new and, in part, there were no strong positive takeaways from the plan (although we highlight that there were also no strong negative takeaways either). Over the last few years there have been several economic revival plans and the market is likely asking whether this latest plan will get any more traction than its slew of predecessors. Our view is that the renewed energy and focus being created by the Presidency should see this plan being better executed than we have experienced in the past. Unfortunately, we remain unconvinced that it will spark the necessary sustainable uptick in SA’s economic growth.

On 31 October, the Health Department said the total number of confirmed COVID-19 cases in SA to date, stands at 726,823, while the recovery rate remains at 90%. The US is still the country with the most COVID-19 infections at 9.28mn, followed by India (8.23mn), Brazil (5.55mn), the Russian Federation (1.66mn) and France (1.41mn) in fifth spot. SA is now in twelfth position globally in terms of total COVID-19 cases.

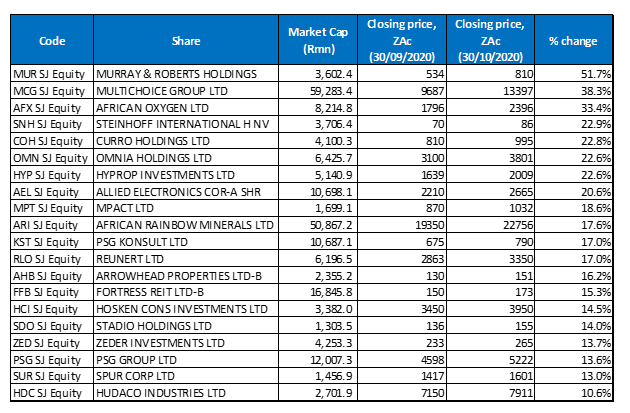

Figure 1: The 20 best-performing shares in October 2020, MoM

Source: Anchor, Bloomberg

Building and engineering Group, Murray & Roberts was October’s best-performing share – soaring 51.7% MoM. The company’s share price rose 9.0% on 12 October alone, after it announced that its subsidiary, Clough, is part of a joint venture (JV), which was awarded a large energy contract in Australia. SecureEnergy, the 50/50 partnership between Clough and Spanish Group, Elecnor was selected for a c. R17.8bn (AUD1.5bn) contract to work on power grids in South Australia and New South Wales. As at end June, Murray & Roberts said it had a significant, quality order book valued at R54.2bn, which includes several multi-year contracts.

In second place, Multichoice’s (+38.3% MoM) share price jumped after it was announced that French broadcasting group, Canal+ had taken a 6.5% equity stake in Africa’s largest satellite TV firm. This move set of talk of possible deeper future ties between the two companies, buoying the Multichoice share price which jumped by c. 9.0% on 5 October alone – its biggest one-day gain in 4 months. Last week it was announced that Canal+ had pushed its stake in Multichoice even higher (to 12%).

African Oxygen (Afrox: +33.4% MoM) was October’s third best-performing share, after receiving a takeout offer from its largest shareholder, Dublin-headquartered, German industrial gases and engineering group, Linde. Linde is offering Afrox shareholders R21.18/share, and Afrox will also pay a special dividend of R3.82/share at a total cost of R1.18bn. Afrox will then delist from the JSE.

Troubled retailer, Steinhoff International’s (+22.9% MoM) share price rose after it said that discussions around a $1bn settlement with various litigants were progressing well and it is requesting consent support from its financial creditors. Last week, the JSE fined Steinhoff R13.50mn – the largest ever imposed by the bourse after an investigation into breaches of listing requirements. This included a maximum possible fine of R7.5mn for publishing “incorrect, false and misleading” information in its previous financial statements. The Financial Sector Conduct Authority (FSCA) has also imposed an administrative penalty of R241mn on former CEO, Markus Jooste for insider trading. Jooste is at the centre of the Steinhoff scandal with accusations that he was involved in false financial reporting and insider trading.

Curro, chemicals and fertiliser Group, Omnia Holdings, and Hyprop recorded share price gains of 22.8% and 22.6% (both Omnia and Hyprop), respectively. In October, Omnia said it had reached agreement to sell its Oro Agri business to European private equity owned, Rovensa. Rovensa’s offer is based on an enterprise value of $165mn for Oro Agri, which will translate to aggregate cash proceeds of c. $152mn (c. R2.4bn) for Omnia. Shareholders are expected to approve the transaction at a general meeting on 14 December. Local property counters have been battered this year, but Hyprop saw a turnaround in its share price fortunes after being massively oversold over the past few months (Hyprop being a retail-focused fund with an elevated LTV ratio). Hyprop released results towards the end of September and the results were clearly (albeit marginally) better than the market was anticipating based on its share price movement in October.

Rounding out October’s 10 best-performing shares were Allied Electronics (Altron), Mpact, and African Rainbow Minerals (ARM), with MoM gains of 20.6%, 18.6%, and 17.6%, respectively. Altron delivered strong results despite the lockdown, reporting a 1H21 revenue advance of 14.0% YoY to R8.35bn, while its diluted EPS stood at ZAc84, vs ZAc67 recorded in 1H20. CEO Mteto Nyati said the results were dominated by the impact of COVID-19, which coincided with the start of the company’s financial year.

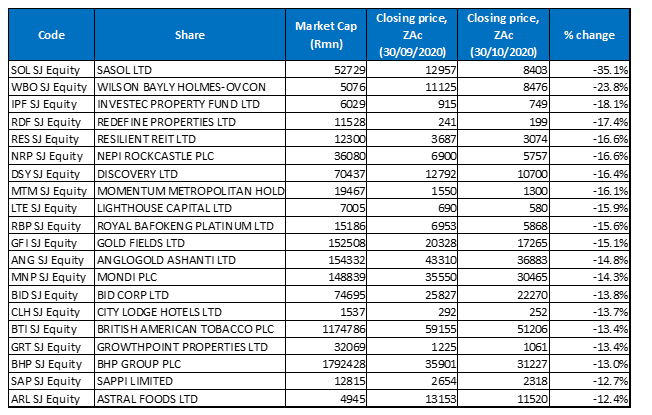

Figure 2: The 20 worst-performing shares in October 2020, MoM

Source: Anchor, Bloomberg

Sasol (-35.1% MoM) was October’s worst-performing share, with the share price now seemingly stuck below R100 (the share traded above R170 in June). The company has literally and figuratively been in the eye of the storm this year as hurricanes, COVID-19, a plummeting oil price, and asset sales have impacted the Group. Last month, a second hurricane in two months forced a shutdown of Sasol’s Lake Charles Chemicals Project plant just as it was restarting operations following the shutdown caused by the pandemic.

Sasol was followed by construction Group, Wilson Bayly Holmes-Ovcon (WBHO; -23.8% MoM) in second spot. In a FY20 trading statement last week, WBHO said that in both Australia and the UK, construction was considered an essential service and, other than four client-suspended projects in the UK, its operations were able to continue, albeit at reduced levels of productivity due to the pandemic (the four suspended projects have also subsequently restarted). Still, WBHO expects to report a FY20 headline loss per share of between ZAc886 and ZAc979, compared with a HEPS of ZAc932.3 recorded in FY19. WBHO added that the impact of COVID-19 on its African operations would result in a revenue decrease of between 5% and 15% YoY, in the building and civil engineering division.

The JSE-listed property sector was already under pressure prior to the pandemic, due to weak fundamentals and the SA economy being in a technical recession. However, subsequent COVID-19-related lockdowns imposed by various governments around the world and on home soil, have resulted in listed property companies facing their most challenging year yet as lockdown-related rental relief and weak demand for retail, office, and industrial space severely impacted earnings, while the pandemic also accelerated the digitisation of businesses and commerce. In addition, some property companies have exposure to European markets that are now experiencing a second wave of the pandemic and the spectre of a more severe lockdown (as is the case in the UK, for example, where PM Boris Johnson announced a hard lockdown on Friday [30 October] that will start on 5 November and only end on 2 December). All of these issues continued to be reflected in the share price performances of JSE-listed property counters in October, with five out of last month’s ten worst-performing shares coming from the sector. Investec Property Fund, which lost 18.1% MoM, was October’s third worst-performing share, followed by Redefine, Resilient, and Nepi Rockcastle, which recorded MoM declines of 17.4%, and 16.6% (both Resilient and Nepi Rockcastle), respectively.

Meanwhile, Discovery, Momentum Metropolitan Holdings (MMH), and Royal Bafokeng Platinum recorded MoM share price declines of 16.4%, 16.1% and 15.6%. In October, financial services group, MMH said that it intends to implement a broad-based BEE trust that would hold 3% of its issued share capital, worth about R641mn. In a production report released last month, Royal Bafokeng said that it had achieved record 4E ounce production of 124.5k oz for the reporting period on the back of an improved BRPM operational performance, the steady ramp-up progress at Styldrift, improved built-up head grades and consistent performance at its concentrators. Total tonnes hoisted for the reporting period increased 27.3% YoY, while total tonnes milled rose 15.6% YoY.

Resilient is a major shareholder in Lighthouse Capital (-15.9% MoM) and Lighthouse in turn has significant exposure to JSE-listed Hammerson, which also owns retail shopping centres in the UK and Europe – the epicentres of the second wave of the pandemic.

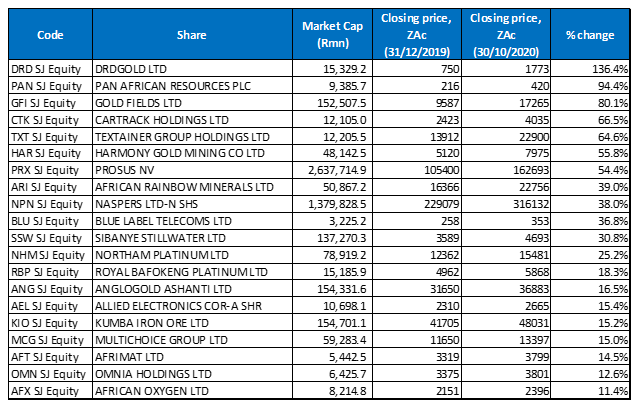

Figure 3: Top-20 YTD performers (to end October 2020)

Source: Anchor, Bloomberg

While gold fell for a second straight month in October, the price of the yellow metal is still up 23.8% YTD, on the back increased global risk brought about by the pandemic, and continued monetary stimulus pushing gold’s rally as a risk hedge. It is therefore not surprising that the three best-performing shares YTD all come from the gold sector (and are unchanged for a fourth-consecutive month), while overall, for the year to end October, five of the ten best-performing stocks are gold and platinum counters – DRD Gold, Pan African Resources, Goldfields, Harmony Gold, and ARM.

DRD Gold (+136.4%) was once again the best-performing share YTD and, in October, it reported a 45% rise in its gold production for the quarter ended 30 September. The company flagged a potential interim dividend as sales jumped by more than half in its 1Q21 and the gold price topped R1.00mn/kg. DRD Gold was followed by Pan African Resources (+94.4%), and Gold Fields (+80.1%).

Cartrack, Textainer, and Harmony Gold are up 66.5%, 64.6%, and 55.8% YTD, respectively. In mid-October, Cartrack, the fleet-management and stolen-vehicle recovery services provider, said that it has more than quadrupled its interim dividend after reporting that the COVID-19 pandemic failed to dull interest in its software. The Group opted for an interim dividend of ZAc87/share for the six months to end-August – up c. 30% YoY, while revenue grew by 16% YoY to R1.08bn. Cartrack also said that it had added 13% more subscribers despite the pandemic, bringing the total number to 1.17mn.

Harmony Gold was followed by Prosus (+54.4% YTD), which saw its share price jump 5.5% in October. Last week, Prosus announced a $5bn (c. R82bn) share buyback programme whereby Prosus, the consumer internet arm of Naspers (+38.0% YTD), will buy back shares as it looks to help close the gap between the value of its underlying assets and its shares.

ARM and Blue Label Telecoms rounded out the 10 best-performing shares YTD, with share price gains of 39.0% and 36.8%, respectively.

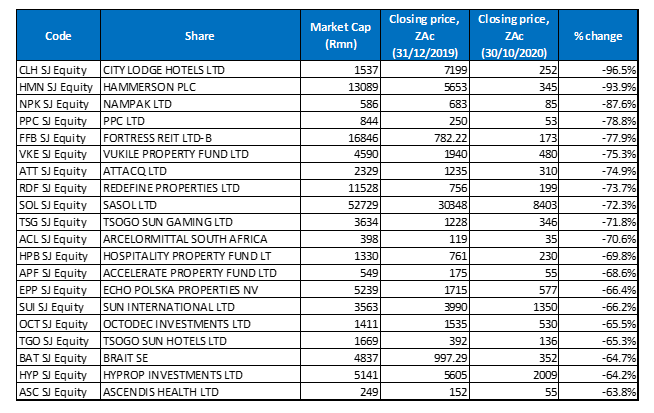

Figure 4: Bottom-20 YTD performers (to end October 2020)

Source: Anchor, Bloomberg

October’s 20 worst-performing shares YTD were basically unchanged from September, with only Sasol (-72.3% YTD and discussed earlier) and Ascendis Health (-63.8% YTD) entering the ring, while Arrowhead Properties and EOH Holdings exited. In addition, ten of the 20 worst-performing shares were from the beleaguered listed property sector.

City Lodge (-96.5% YTD), which has seen limited trading in its shares over the past seven months, claimed the worst-performer title for a third month in a row. This, as the COVID-19 induced lockdowns and a difficult local economic environment continued to take their toll on the company’s fortunes. In July, City Lodge was compelled to raise R1.2bn through a rights issue in order to pay down debt and prop up its balance sheet. This after asking its bankers in June for an additional R200mn, which pushed the company over agreed lending limits.

City Lodge was followed by UK and European shopping centre owner, Hammerson plc (-93.9% YTD), with Nampak (-87.6% YTD) remaining in third position. In October, Hammerson, which owns shopping centres in the UK and Europe, said that rental collection was steadily improving as tenants resume operations after the lockdown. However, this was prior the UK’s announcement last week that it would be resuming lockdowns on 5 November to combat a second wave of COVID-19.

Nampak was followed by PPC (-78.8% YTD), Fortress REIT -B- (-77.9% YTD), Vukile Property Fund (-75.3% YTD), Attacq (-74.9%), and Redefine (-73.7% YTD), with Sasol (-72.3% YTD), and Tsogo Sun Gaming (-71.8% YTD), rounding out October’s ten worst-performing shares YTD.