We had expected the South African Reserve Bank (SARB) to resume its rate-cutting cycle at its 26 March meeting. However, this was before the events of 28 February, when the US/Israel alliance launched military action against Iran, which has materially changed the outlook. Iran’s closure of the Strait of Hormuz continues to constrain global oil supply, pushing prices above US$100/bbl and introducing a significant upside risk should disruptions persist.

This shift has prompted a more cautious, “higher-for-longer” stance from the Monetary Policy Committee (MPC), despite South Africa’s (SA) February headline inflation slowing for a second consecutive month, easing to 3.0%, in line with the SARB’s revised 3% mid-point target (within a 2%–4% band). While inflation has been on a favourable trajectory, rising energy costs now pose clear upside risks, particularly through fuel, transport, and second-round effects.

Externally, conditions have become less supportive. Oil prices are c. 30% higher while the gold price has declined by around 20%, resulting in a deterioration in SA’s terms of trade. As a net importer of oil, this dynamic places pressure on SA’s current account and contributes to rand weakness. Although we do not believe a sustained move in the rand beyond R17.00/US$1 is fundamentally justified, sentiment-driven volatility and global risk aversion may lead to temporary overshooting.

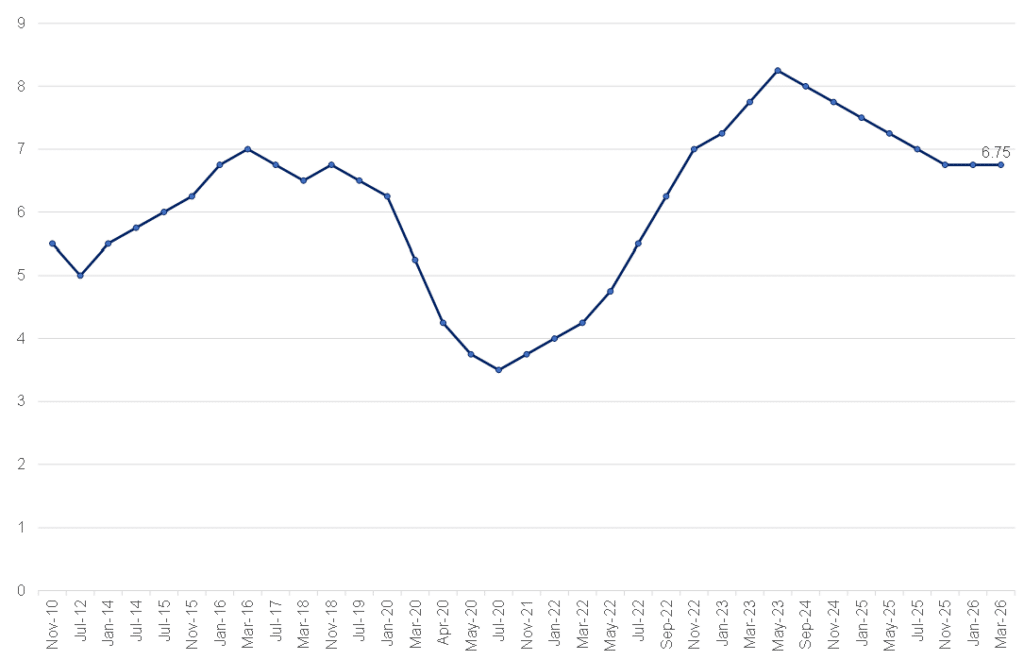

Against this backdrop, the SARB’s MPC opted to hold the repo rate at 6.75% (prime at 10.25%), with a unanimous decision among the six members of the MPC reflecting the heightened uncertainty. The policy bias has shifted: risks are no longer skewed toward easing but toward a delay in rate cuts and, in more extreme scenarios, potential tightening. The SARB has also revised its headline inflation forecast for 2026 upward to 3.7% from January’s 3.3% forecast. For 2027 and 2028, it now expects a 3.3% and 3.0% inflation rate, respectively.

Figure 1: The history of the SARB MPC’s repo rate changes, %

Source: SARB, Anchor Capital

We believe that a sustained move in the rand above R17.50/US$1 or oil prices above US$135/bbl would materially increase the probability of a rate hike. While any such tightening would likely be short-lived, given the negative impact on growth and consumers, it underscores the shift in the policy balance.

Our base-case scenario is that the interest rate remains on hold in the near term, with rate cuts deferred until there is greater clarity on the oil price trajectory and geopolitical developments. Conversely, a meaningful de-escalation in the conflict could quickly reopen the window for easing rates. However, for now, the bar for cuts has risen.

Given this uncertainty, we remain cautious on the rand and see more compelling opportunities in other asset classes, especially where recent volatility has created value. SA bonds, for example, appear oversold and may offer attractive entry points for investors willing to look through near-term risks.