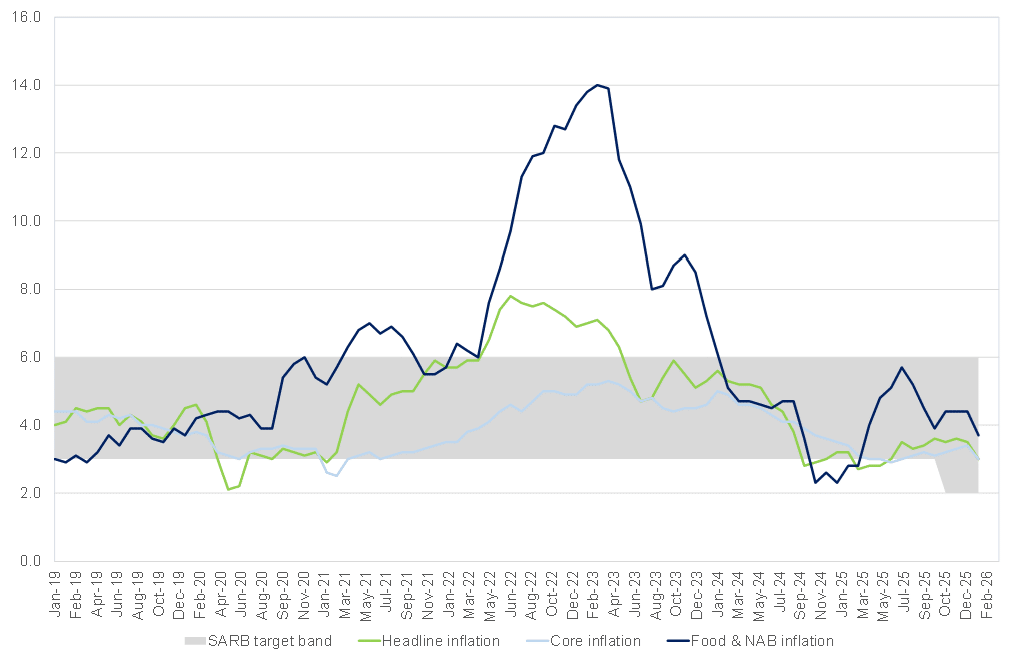

South Africa’s (SA) annual inflation rate, as measured by the Consumer Price Index (CPI), slowed for a second consecutive month, easing to 3.0% in February vs January’s 3.5% print. This marks the lowest level since June 2025 and is below consensus expectations of 3.2%. MoM, headline inflation rose 0.4%. Core inflation, excluding the volatile food and non-alcoholic beverages, fuel and energy categories, also moderated to 3.0% YoY (+0.7% MoM) from 3.4% in January, marking its lowest point since 2021, and a broad-based easing in underlying price pressures.

The latest print aligns with the South African Reserve Bank’s (SARB) newly adopted inflation target of 3%, with a 1-ppt tolerance band (meaning a range of 2%–4%), replacing the previous 3%–6% range and reinforcing the central bank’s efforts to anchor expectations at a lower level to support long-term economic growth. This latest headline inflation print was exactly on the SARB’s 3% mid-point target. However, it is important to recognise that February’s data represents a “before” snapshot, captured prior to a significant escalation in global geopolitical tensions.

Figure 1: SA inflation, YoY % change

Source: Stats SA, Anchor Capital

Currently, inflation remains largely driven by housing and utilities (+4.8% YoY, adding 1.1 ppts to the headline number), food and non-alcoholic beverages ([NAB]; +3.7% YoY, +0.7 ppts), and insurance and financial services (+4.7% YoY, +0.5 ppts). NAB inflation rose primarily because of surging meat prices (+12.2% YoY), reflecting the impact of the foot-and-mouth disease outbreak, while fruits and vegetables remained in deflationary territory (-7.2% and -2.7% YoY, respectively). February’s strong headline print was also helped in part by base effects linked to a delay in the implementation of certain medical aid increases and a 2.1% drop in transportation prices, following January’s 0.2% decline and reflecting a sharper fall in fuel prices (-10.1% YoY vs -3.7% YoY)

However, since the end of February, the global backdrop has shifted materially. On 28 February, the US and Israel launched coordinated strikes on Iran, triggering the closure of the Strait of Hormuz, through which one-fifth of global oil supply passes, resulting in the largest global oil supply disruption on record. Since the outbreak of hostilities, tanker traffic through the Strait has ground to a near-halt. Brent crude, which ended February at c. US$72/bbl has surged to above US$110/bbl. On 18 March, following Israeli strikes on Iran’s South Pars gas field, the world’s largest natural gas reserve, oil spiked further to c. US$110/bbl, materially altering the inflation outlook.

For SA, as a net importer of refined petroleum, this shock is transmitted quickly into domestic fuel prices via the monthly fuel price adjustment mechanism. Higher fuel costs typically feed through to transport and logistics, with broader second-round effects across food, manufacturing, and services.

For SA households, already facing a constrained cost-of-living environment, the impact of increasing oil prices will become visible through higher fuel prices, transport costs and food inflation. Current estimates point to a petrol price increase of between R3 and R4/litre, with diesel prices potentially exceeding R7.00/litre. In addition, the April fuel price adjustments will incorporate Budget 2026 fuel-related tax increases (carbon, general fuel, and Road Accident Fund [RAF] levies).

While the local economy has demonstrated resilience to temporary shocks in the past, a prolonged period of elevated oil prices would place strain on SA’s still fragile recovery. The weeks ahead will be critical in determining whether the current market turbulence proves temporary or evolves into a more persistent macroeconomic challenge for SA and the world.

A sustained increase in oil prices could place upward pressure on inflation at a time when policymakers were hoping to anchor inflation expectations closer to the SARB’s 3% target. The SARB’s next Monetary Policy Committee (MPC) meeting is scheduled for 26 March, and the latest developments have increased the uncertainty surrounding the policy outlook.

Although the current environment does not yet resemble a systemic crisis, SA enters this period with relatively strong fiscal buffers and a more stable macro framework than in previous shocks. However, elevated oil prices are likely to place upward pressure on inflation, particularly through fuel and transport costs. A fuel price rise is unlikely to be contained only to the transport component of CPI, with second-round effects expected across multiple categories, including food prices, services, manufacturing, retail, etc. As a result, the key variable is not the initial spike in oil prices but the duration for which elevated energy costs persist and the extent to which they feed through into broader inflation dynamics.