In an era marked by increasing population growth, shifting dietary preferences, climate change uncertainties and intricate trade networks, ensuring global food security has become a pivotal challenge requiring collaborative efforts across nations, sectors, and disciplines. Whilst not immediately apparent, global food security holds significant implications for financial markets due to its interconnectedness with broader economic and geopolitical dynamics. For example, fluctuations in global food prices can lead to market instability. Food price spikes can impact inflation rates, affecting central bank interest rates and monetary policy decisions. These fluctuations can also impact consumer spending patterns and investor sentiment. Furthermore, disruptions in food supply chains due to trade disputes, export restrictions, or natural disasters can lead to market uncertainty. Naturally, financial markets react to these disruptions as they influence cross-border trade, shipping, logistics, and transportation industries.

Moreover, institutional investors, such as pension funds and insurance companies, assess food security risks as part of their portfolio diversification and risk management strategies. Climate-related risks, supply chain disruptions, and social unrest related to food security are all considered when evaluating various investment risks. Simply put, financial markets react to the various (often complex) interwoven elements that shape food security, making it a crucial factor for investors, businesses, and policymakers to consider when making financial decisions.

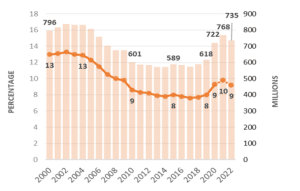

As per the World Bank’s latest estimates, global hunger (measured according to the prevalence of undernourishment) remained relatively unchanged from 2021 to 2022 but is significantly higher than before the COVID-19 pandemic. Approximately 9.2% of the world’s population faced hunger in 2022, compared with 7.9% in 2019. Between 691mn and 783mn people experienced hunger in 2022 – 122mn more than in 2019.

Figure 1: Number and percentage of undernourished people globally

Source: World Bank

Over recent years, progress has been made in reducing hunger in Asia and Latin America, but it continues to increase in western Asia, the Caribbean, and all subregions of Africa. The World Bank further projects that by 2030, almost 600mn people will be chronically undernourished, highlighting the significant challenge of eradicating hunger, particularly in Africa. Unsurprisingly, Russia’s invasion of Ukraine has resulted in substantial ramifications across the global economy, impeding the economic recovery that had begun in 2021 after the global COVID-19 pandemic. Global gross domestic product (GDP) grew by 3.4% YoY in 2022, 1 ppt slower than initially predicted. Russia’s war on Ukraine cast a significant shadow over global food and agricultural markets, given the pivotal roles of Russia and Ukraine as major agricultural producers and exporters.

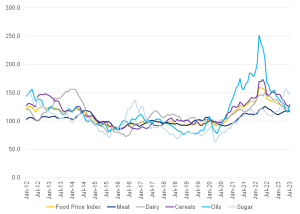

This geopolitical upheaval triggered a rapid escalation in international food prices, with the Food and Agriculture Organization (FAO) Food Price Index reaching an all-time high in March 2022. The cost of food imports surged, impacting nations heavily reliant on food purchases from abroad and driving global food imports to an unprecedented threshold of nearly US$2trn due to inflated prices. Consequently, escalating costs for food and inputs drove overall inflation, with global headline inflation surging beyond 9% in the latter half of 2022. While the economic rebound in 2022 bolstered disposable incomes and food accessibility for some households, elevated food costs and inflation eroded access for others, particularly for the most vulnerable segments of the global population. As a result, worldwide hunger persisted significantly above pre-pandemic levels across the globe.

Figure 2: FAO’s Global Food Price Index

Source: FAO, Anchor

It is essential to remember that food and nutrition security encompasses more than calorific intake. Nutrition security is vital in the formal measure of overall food security. As such, good nutrition is achieved through a suitably nutritious and balanced diet. More recently, the ‘nutrition transition’ concept has become a concern, particularly within developing countries. The idea essentially refers to the increased consumption of animal products, fats and refined sugars as they become more affordable and easily accessible to consumers in developing nations. Overall, nutrition security exists when a nutritionally adequate diet combines regular physical activity, a sanitary environment, good health services, knowledge, and care. For example, South Africa (SA) does not face a national food security problem but rather a structural household food insecurity problem, primarily caused by widespread poverty and unemployment.

Aside from the usual suspects that typically drive food insecurity (think adverse weather patterns, geo-political tensions etc.), trade policies are increasingly becoming a significant source of risk for global food price stability. For example, governments often implement export restrictions (export bans, quotas, or taxes) to ensure domestic food security or control domestic prices. While these measures might stabilise domestic markets, they can lead to price spikes and volatility in the global market. Similarly, import restrictions can limit food availability in certain countries, leading to higher domestic prices. Tariffs and other trade barriers can increase the cost of importing food products, potentially leading to higher domestic prices in countries that rely heavily on imports for their food supply. This can affect both consumers and producers, as higher input costs can impact production and increase final prices for consumers.

Global trade policy actions on food and fertiliser have surged since the beginning of the war in Ukraine, in addition to countries having actively used trade policy to respond to domestic needs when faced with potential food shortages at the beginning of the COVID-19 pandemic. As of July 2023, twenty countries had implemented 28 food export bans, and ten had implemented 14 export-limiting measures. Using the latest trade restrictions, on 19 July 2023, the government of India amended its export policy on non-basmati white rice from “Free with export duty of 20%,” which it had imposed in September 2022, to “Prohibited,” with immediate effect. This particular trade restriction was implemented to ensure the availability of non-basmati white rice and limit price increases in the domestic market. Given that India is the world’s dominant rice exporter (accounting for nearly 40% of the global rice market), this could naturally cause considerable increases in global prices and general volatility across markets. Unfortunately, the export ban comes at a time of heightened global concerns about international global food prices following Russia’s exit from the Black Sea Grain Initiative.

It is important to note that the impact of trade policies on food prices can be complex and multifaceted. Policies that aim to ensure domestic food security might inadvertently contribute to global price volatility, and policies that promote international trade might have differing impacts on various countries and regions. However, achieving global food price stability requires a delicate balance between domestic policy objectives, international trade considerations, and the broader goals of ensuring food security and reducing market volatility.