National Treasury’s (NT’s) 2024/2025 Budget was tabled in Parliament on Wednesday (21 February) by South Africa’s (SA’s) Minister of Finance Enoch Godongwana. This year’s budget was tabled amid an even more challenging economic and socio-political environment than previous iterations, given the upcoming national elections, the decades of policy inertia and years of state capture that preceded it. As expected, the 2024 budget did not introduce any new, significant populist policies or spending measures before the upcoming elections. Instead, NT continues to toe the line between fiscal continuity, consolidation and declining revenues amid an increasingly stagnant local economy.

Notably, to help mitigate SA’s growing debt burden, NT has decided to reduce its borrowings over the medium term by using a portion of valuation gains in the Gold and Foreign Exchange Contingency Reserve Account (GFECRA) held at the South African Reserve Bank (SARB). As such, the government will receive R150bn in distributions from the SARB over three fiscal years: R100bn in 2024/2025, R25bn in 2025/2026 and R25bn in 2026/2027. As a result, Treasury states that using the GFECRA, debt-service costs will decline by R30.2bn over the 2024 Medium Term Expenditure Framework (MTEF) period compared with the 2023 Medium Term Budget Policy Statement (MTBPS) estimate. In turn, this will reduce domestic market financing requirements and the growth of debt stock and debt-service costs.

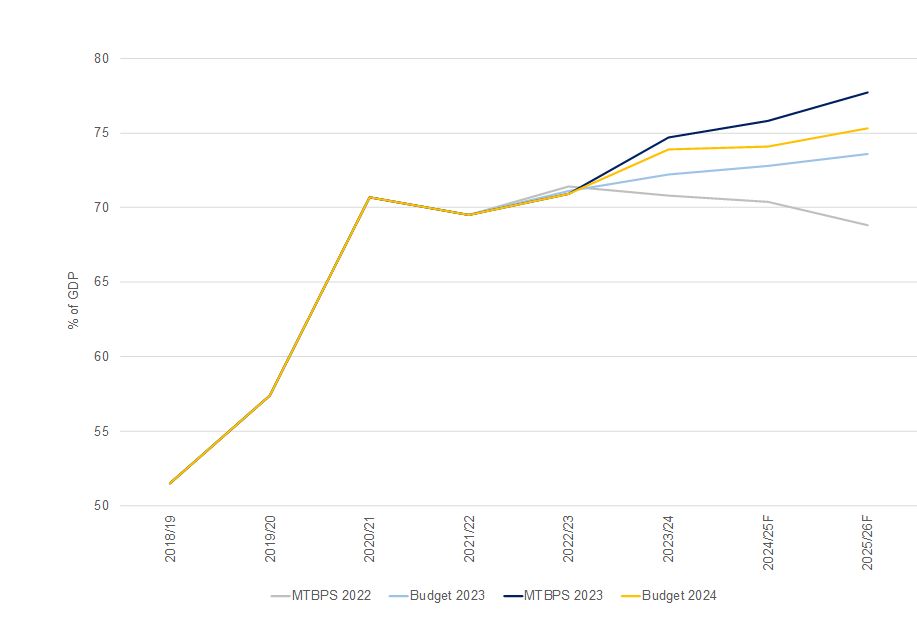

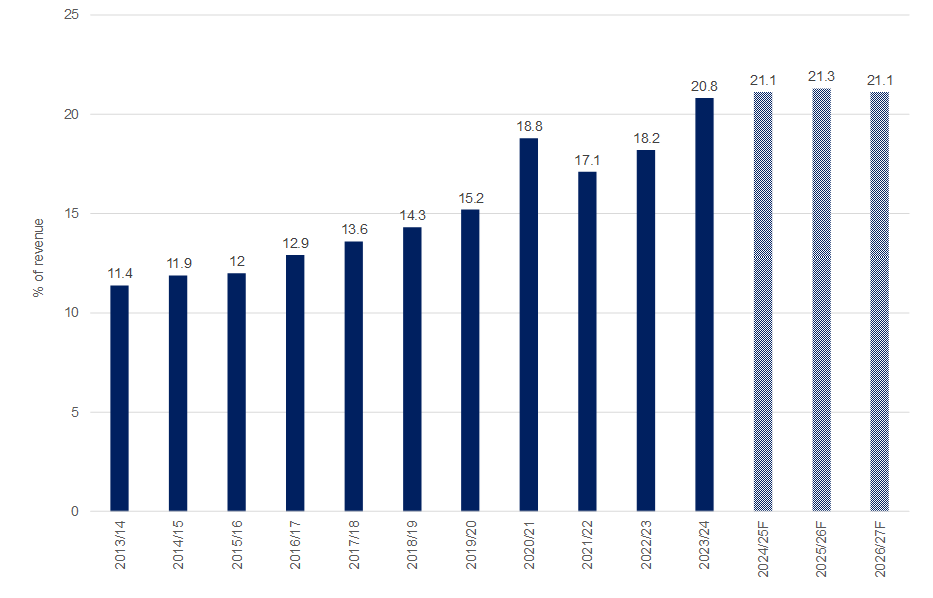

This seemingly forms a useful short-term measure but does not address the longer-term structural issues of SA’s growing debt burden. Although government debt is now expected to stabilise at 75.3% of GDP in 2025/2026 (lower than the 77.7% projected in the 2023 MTBPS), essentially thanks to the use of GFECRA, in 2023/2024, for the first time since 2000/2001, debt‐service costs absorb more than ZAc20 of every rand collected in revenue. Moreover, debt-service costs now absorb more of the budget than basic education, social protection, or health. The SA’s government gross loan debt‐to‐GDP trajectory is about 16% higher than the median emerging market (EM) level. Reducing debt‐service costs remains critical for SA’s growth and development.

Figure 1: SA government debt forecasts

Source: National Treasury, Anchor

Figure 2: Debt-service costs as a share of main budget revenue

Source: National Treasury, Anchor

Matching expectations, gross tax revenue for 2023/2024 was R56.1bn, which was lower than estimated in the 2023 Budget due to a decline in corporate profits and revenue from taxes on mining – reflective of the current economic status quo in SA. In an attempt to alleviate these fiscal pressures, NT has proposed some tax reforms to be implemented this year. In the short-term, personal income tax brackets are unchanged for 2024/2025 (i.e., not adjusted for inflation), along with above-inflation adjustments to some excise tax rates and medical tax credits not being raised for inflation. These are collectively expected to add R15bn in revenue for the fiscus.

In the longer term, two notable tax reforms are the two-pot retirement system and the new minimum corporate tax rate. The two-pot retirement system will be implemented on 1 September 2024, with an estimated R5bn likely to be raised in 2024/2025 from the tax collected when retirement fund members access once-off withdrawals. The new global minimum corporate tax will be implemented on multinational corporations with annual revenue exceeding EUR750mn. It will be subject to an effective tax rate of at least 15% regardless of where their profits are located. This tax also aims to limit the adverse effects of tax competition. It is expected to raise an additional R8bn in corporate tax revenue in 2026/2027. While these tax reforms align with international standards, in general, SA’s tax policy is skewed towards the more aggressive side of the scale, raising questions about longer-term imbalances in the economy.

Overall, the risks to SA’s fiscal position are largely unchanged since the 2023 MTBPS. Weak economic growth continues to slow revenue growth and widen the budget deficit. The risks around higher borrowing costs, unaffordable wage increases in the second year of the MTEF period and further deterioration in the balance sheet of major public‐sector institutions (resulting in bailout demands) remain as prevalent as ever. Nonetheless, the 2024 Budget has turned out to be a reasonably neutral affair followed by a somewhat positive market reaction. Overall, the primary fiscal intent is unchanged, and the fiscal prognosis has turned out marginally better than many market participants initially feared – notwithstanding the risky headwinds currently facing the local economy.

At the end of the day, the SA economy requires significant investment to grow and drive sustainable job creation. Whilst the 2024 Budget prioritises macroeconomic stability, structural reforms, and improved state capacity, it will take time to reverse the consequences of operational, maintenance and governance failures at state‐owned companies (primarily those of Eskom and Transnet), decades of policy inertia and years of state capture.