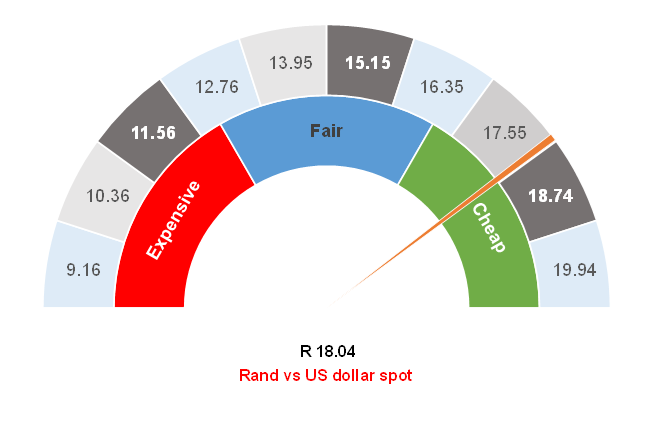

Figure 1: Rand vs the US dollar

Source: Anchor

Global markets are trying to determine what to expect from the incoming Donald Trump administration. From his cabinet announcements, we can infer that he intends to deliver on campaign promises and that loyalty is a priority for his presidency. He campaigned on four broad policy objectives that we outline below.

- President-elect Trump remains eager to increase tariffs for goods imported to the US, at one stage talking about a 60% tariff on goods from China and 10% on goods from the rest of the world. The current base case in financial markets is that we will see increased tariffs in the first half of 2025 but to a less extreme extent. The broader expectation is that he will raise tariffs on Chinese goods towards c. 20% to 25% quite soon after taking office. Other countries are less likely to face immediate tariff increases. This scenario has a negligible impact on US economic growth while increasing US inflation by about 0.35% as a one-off event. The effect is sufficiently small that US core inflation will still end next year at a lower rate than it is right now. The US Federal Reserve (Fed) rate cut expectations remain intact from this perspective. There is a risk of broader tariffs, which could come as a negative shock to bond and equity markets.

- The incoming president’s focus on reducing immigration, particularly of lower-skilled individuals, could lead to a c. 20% decline in immigrants to the US next year. With the US economy already at full employment, the reduced availability of labour may lead to some inflationary pressures and act as a handbrake on economic growth. This, coupled with stronger-than-expected US economic data, is part of the reason why the market is pricing in fewer US rate cuts.

- The president-elect favours tax cuts. The US has several tax concessions expiring in the next year. The current view is that he will extend the expiring tax cuts. This in and of itself will cost the US Treasury just over US$4trn in reduced revenue. The consensus is that there is limited scope or ability to implement additional cuts beyond extending the current tax cuts. This is broadly neutral for the market at this stage.

- There is much excitement on social media about the role of Elon Musk and the Department of Government Efficiency (DOGE). However, financial markets are not yet convinced and are pricing-in only modest spending cuts and benefits from this office. As a result, the government will likely be issuing bonds to fund the extension of the tax cuts. The US 10-year bond is around 4.4% at the moment, and an uptick in issuance might see this rise toward 4.75%.

When all of this is tallied up, Anchor anticipates 1.25% of further US rate cuts this cycle, with the US Fed funds rate pushing toward 3.25%-3.5%. This is one rate cut (of 0.25%) more than US futures are pricing in at the moment. In our view, longer-dated bonds are at about fair value right now while we wait for direction on tax cuts and tariffs over much of 2025.

Domestically, we have been in a good place with Standard & Poor’s revising South Africa’s (SA) outlook to positive (from stable). We do not think a rating upgrade is imminent, but there is increasing evidence that SA is gradually bottoming out and that the forward trajectory is more positive. The South African Reserve Bank (SARB) held its Monetary Policy Committee (MPC) meeting last week and cut rates by 0.25%, as was broadly expected. The highlight was that the SARB has now pencilled in economic growth of 2% for 2027. The SARB probably has the best economic models in SA and carries significant credibility. The central bank seems to be indicating that the SA economy has bottomed. The MPC meeting was met with a slightly positive market reaction. We continue to hold that SA will likely see more positive than negative news headlines in the coming months and that domestic bonds still hold value.

Perhaps the only point of difference is that interest rates were cut by 0.25%. Prime is now 11.25%. The SARB models, financial markets, and Standard Bank economists are only predicting two further interest rate cuts of 0.25% each this cycle, with prime bottoming out at 10.75%. Anchor remains of the view that there will be additional interest rate cuts and that the prime rate will bottom at 10.50% toward the MPC meeting in July 2025. So, tallying that all up, domestic rates are fair, with possible positive surprises occasionally.

Interest rate cuts will reduce the running yields of our portfolios. Based on the above, we estimate where we stand today and what is likely to transpire over the next 12 months as further interest rate cuts are expected.

Figure 2: Portfolios’ current yield and forward estimates

Source: Anchor

The US dollar has been on a strengthening trend since the US election. Trump’s America First policies will likely keep the greenback strong, while tariffs in the first half of next year are probably negative for emerging markets (EMs). All said and done, there is not much to be excited about for the next while on the global front. Domestic sentiment, a positive trade balance, and no deteriorating fundamentals should help a little. We are also starting with a rand that is relatively oversold. We anticipate that the rand will trade in the R17.00-R18.00/US$1 range for the next year, with any rand strength being more back-ended next year while we wait for certainty on global policies. One year out, the rand will likely trade closer to R17.00/US$1 than R18.00/US$1.

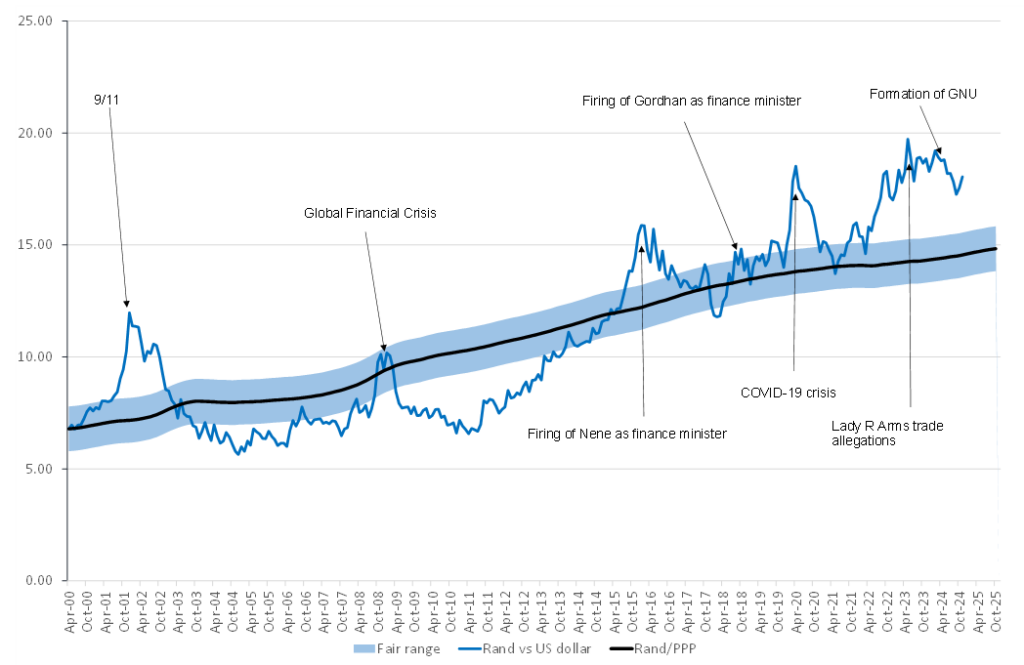

Figure 3: Actual rand/US$ vs rand PPP model

Source: Thomson Reuters, Anchor