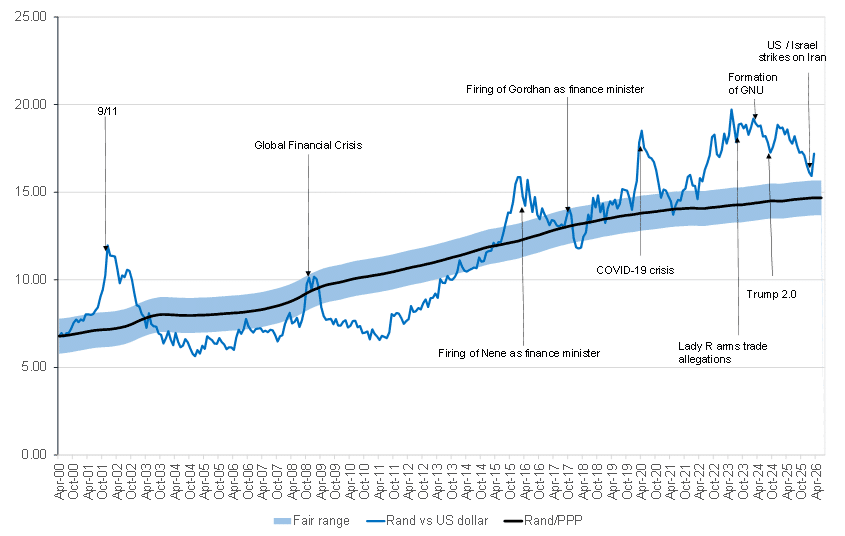

Figure 1: Rand vs the US dollar

Source: Anchor Capital

The war between the US/Israel-led alliance and Iran continues to evolve, with tensions now centred on the closure of the Strait of Hormuz, a critical artery for global oil supply. As of 21 March, diplomatic efforts to reopen the Strait had proven unsuccessful, with Iran’s response pointing to a prolonged and uncertain standoff. US President Donald Trump subsequently issued a 48-hour ultimatum aimed at reopening the Strait. Today (23 March), he indicated via a post on Truth Social that talks between the parties are showing signs of progress. While this introduces a degree of cautious optimism, the situation remains fluid and highly sensitive to further developments. For now, the Strait remains closed, and global oil supply continues to be constrained, underscoring the ongoing risk to energy markets.

At the onset of the conflict, approximately 2.9bn barrels (bbls) of oil were held in commercial storage facilities outside the region. By our estimation, based on current consumption trends, this provides a limited buffer, with potential supply pressures emerging within the next three to five months (should disruptions persist), which could become very problematic in terms of global access to oil. In addition, oil production across parts of the Gulf has been curtailed, and any restart would likely be gradual.

The escalation staircase has seen oil rise to over US$100/bbl, and even US$140/bbl is becoming a realistic scenario if the Strait remains closed over the coming months. This evolving backdrop has important implications for global markets and, by extension, South Africa (SA).

From a South African perspective, the shift in key commodity prices is particularly unfavourable. Gold has declined meaningfully (down c. 19% from 27 February to c. US$4,264 currently), and oil prices are c. 30% higher over the same period, resulting in a meaningful deterioration in SA’s terms of trade. As a net importer of oil and exporter of commodities such as gold, this dynamic places pressure on the current account and, in turn, the currency.

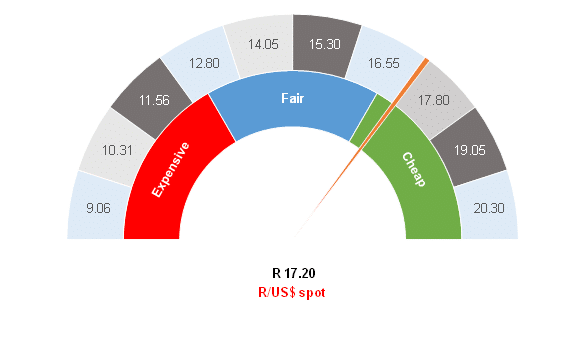

Locally, market dynamics and the weaker rand have been driven largely by sentiment. We remain of the view that fundamentals do not really support a rand weaker than R17.00/US$1 at this stage. However, in periods of elevated uncertainty, market pricing can deviate materially from fair value. We are seeing massive swings based on whether Trump’s random tweets on Truth Social are deemed to be inflammatory or de-escalatory in nature. This means that the rand can still weaken meaningfully away from its fair value or strengthen. As seen in previous global shocks, including the COVID-19 pandemic, overshooting remains a risk, and it is quite plausible that the rand breaches R19.00/US$1 again. Still, this is neither our base case scenario nor likely. It is all about how far the escalation of the conflict goes and when it simmers down.

From a monetary policy perspective, with the rand at R17.20/US$1 and oil at c. US$110/bbl, we maintain our view that the South African Reserve Bank (SARB) is not compelled to respond, and we believe an interest rate hike is not warranted yet. Nevertheless, we are moving toward the precipice where a rate hike could become inevitable. We maintain our view that a sustained move above R17.50/US$1 or the oil price above US$135/bbl would likely increase the possibility of a policy response. At those levels, we think the hike will be relatively short-lived due to the fallout in the economy from higher oil prices and the negative impact on consumers.

Our base case is that the rand hovers around current levels, with a bias towards modest weakness in the event of an escalation. Conversely, we think that the rand can snap back meaningfully if we see a significant de-escalation. Given the binary nature of the current environment, we remain cautious about taking positions in the rand. Instead, we see more compelling opportunities in other financial asset classes (such as bonds), particularly where recent market directions have created value. SA bonds, for example, have been oversold and may offer attractive entry points for investors willing to look through near-term volatility.

Figure 2: Actual rand/US$ vs rand PPP model

Source: Thomson Reuters, Anchor Capital