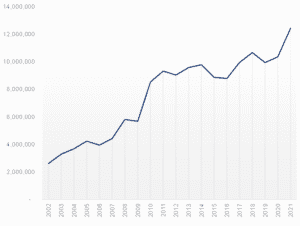

Despite South Africa’s (SA’s) landmass being mostly a semi-arid climate, the country has ample agricultural output. As a result, SA exports about half of what it produces in value terms every year. These SA-exported products were worth a record US$12.4bn in 2021, making the sector an increasingly important currency earner. Agricultural exports are diverse, with SA’s top exports consisting of citrus fruits, grapes, maize/corn, and wine, amongst many other commodities. SA’s primary export markets are well diversified (both country-specific and regionally across continents), which means that the local agricultural sector is not overly dependent on any single market. SA’s geographical position also makes it an ideal exporter to Northern Hemisphere countries. Export markets span the African continent, Europe, Asia, the Middle East, and the Americas.

SA has reached this level of agricultural trade diversification partly because of the openness of SA policymakers, agribusinesses, and farmers to technological advancements, mechanical and biological, which have been instrumental in driving productivity higher. However, the reality of SA’s geographical environment means that it cannot produce all the food products both required and demanded by local consumers. For example, SA’s agricultural import bill in 2021 was US$6.9bn. The top-five imported products that year were palm oil, rice, wheat, poultry meat, whiskies, and other spirits. These accounted for 30% of the total import value. Notably, SA does not have the climate to increase its production of some of the top-three products – palm oil, rice, and wheat. The first two (palm oil and rice) are not even plausible because SA is semi-arid.

Figure 1: SA total agricultural exports, US$’000

Source: ITC Trade Map, Anchor.

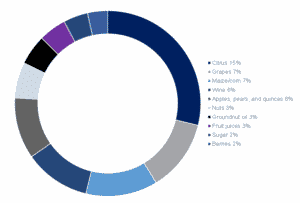

Figure 2: SA top-10 agricultural exports, 2021

Source: ITC Trade Map, Anchor.

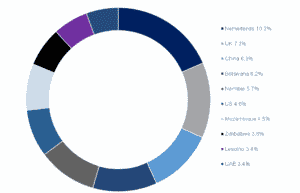

Figure 3: SA top-10 agricultural export markets, 2021

Source: ITC Trade Map, Anchor.

As we move further into 2022, the impact of the recent floods in Durban, which have destroyed infrastructure and interrupted trade activity, will likely appear in the 2Q22 trade data. 1Q22 faced similar constraints to past quarters, such as delays at ports and rail and deteriorating road infrastructure. This is true for all exporting sectors of the local economy, including the agricultural sector. In 1Q22, the sector collectively drove engagement in more coordination with Transnet, agriculture industry groups, and transport organisations, which, in turn, helped improve the flow of information about various challenges and functions at SA ports. This was particularly with regards to Port of Cape Town, where there were long delays at the start of this year due to numerous infrastructure constraints and weather-related difficulties.

Nonetheless, in 1Q22 the sector was dominated by Russia’s invasion of Ukraine, which disrupted trade with the Black Sea region. For SA agriculture, the war holds great relevance – particularly for the horticulture subsector. Russia accounts, on average, for 7% of SA’s citrus exports in value terms, and 12% of SA’s apples and pears exports. Consequently, concerns were high across the sector that the impact of the conflict would instantly show in local trade data. However, exports were modestly up in 1Q22 (+1% YoY) to US$2.96bn. On a QoQ basis, exports rose 6%. The top exportable products were grapes, maize, wine, apples and pears, peaches, cherries and apricots, wool, and fruit juices, amongst other products.

The key drivers underpinning this robust export value are the sizeable agricultural output in the 2021/2022 production season, combined with general solid global demand, even at higher agricultural commodity prices for maize. Still, April’s heavy rains and floods in KwaZulu-Natal (KZN) possibly had a notable impact on trade activity, although the response to rebuild by Transnet and other organisations was timeous. Subsequently, it is plausible that there will be a decline in trade activity in 2Q22, given the importance of the Port of Durban for both exports and imports of agricultural products and other goods.

Over the past decade, the area planted for high-value fruits (i.e., citrus, pome fruit, stone fruit, table grapes, and avocados) increased by more than one-third – from c. 140,000 in 2011 to more than 192,000 hectares in 2021. Investments in these industries assumed that SA can grow its export base, and build on a strong competitive performance throughout the value chain backed by expanding export market demand. Positively, this is exactly what transpired – export volumes increased from 2.3mn tonnes to 3.6mn tonnes over the past decade, with additional volume growth still expected in the coming years as recently planted, non-bearing trees mature to reach full bearing. However, from a logistical point of view, the business model for future success in these industries is under severe pressure. Since the start of 2020, there have been consecutive Black Swan events that threaten the sustainability of these investments and job creation. For example, the horticultural sub-sector employs more agricultural workers per hectare and in total, despite it only contributing c. 30% to the gross value of production from farming. How did the current situation come about? Three key aspects of the logistics chain are proving to be highly problematic – global shipping schedule reliability, global container freight rates, and domestic port performance.

- Global shipping schedule reliability

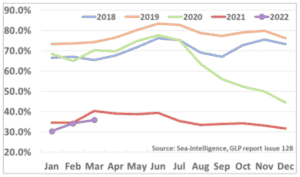

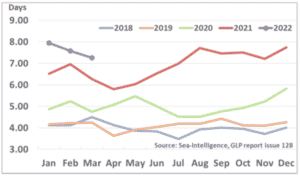

Figure 4: Global container line schedule reliability

Source: Sea-Intelligence, GLP report issue 128

Figure 4 above shows the reliability of container ships remaining on schedule, on a monthly from 2018 to 2022. Until July 2020, schedule reliability fluctuated between 65% and 85%. It has, however, declined ever since, to as low as 30% in 2021. More concerning is that schedule reliability in terms of the global average delays for late vessel arrivals indicates that 2022 has thus far been even worse than the start of 2021 (see Figure 5).

Figure 5: Global average delays for late vessel arrivals

Source: Sea-Intelligence, GLP report issue 128

- Global freight rates

Maersk was recently overtaken by MSC as the world’s largest container shipping operator, holding a 16.7% market share of the global liner fleet. In 2019, 2020, and 2021, Maersk reported loaded volumes across all shipping routes of 13.3mn, 12.6mn, and 13.1mn containers, respectively. Therefore, it appears that low schedule reliability and delays have not affected the total loaded volume, only the time of collection and delivery. However, despite a minimal variation in loaded volumes, freight rates have soared as schedule reliability worsened in July 2020. Consequently, carriers’ YoY growth in net profit increased, on average, by 828%, with operating profit margins growing from 17.2% in 2020 to 48.4% in 2021. At its peak in September 2021, shipping a 40-ft container would have cost US$10,361, compared to the US$2,644 cost just 12 months prior. At R16.72/US$1 in September 2020 and R14.58/US$1 one year later, the cost of shipping product changed from R44,208 to R151,063 per 40-ft container. Most of these cost increases are shifted back into the value chain towards producers, rather than being absorbed by consumers. Whilst food inflation has risen, the increases are not indicative of the total cost increase in the value chain, pointing to severe pressure on margins.

- Domestic port performance

In a statistical exercise by the World Bank to rank 351 container terminals by their performance in 2020, Cape Town (347), Durban (349), and the Port of Ngqura (351) were three of the five worst-performing ports in the world. Unfortunately, the situation has not improved. In 2021 Transnet’s system was hacked and unrest in KZN impacted access to the port and its operations. At the Port of Cape Town’s container terminal, a power outage in December 2021 resulted in around 1,350 reefer containers with stone fruit, table grapes, and blueberries being left for 28 to 36 hours without power. Furthermore, Transnet reported that a total of 96 operational days were lost at the terminal in the most recent financial year. In 2022, operations at the Port of Durban and access to the terminal have been hampered by floods for the second time in as many months. This has sadly occurred while the fruit production area has expanded in SA, with export volumes having consequently increased. The result is even greater challenges for SA producers and exporters than for many of their international competitors.

Although high-value fresh exports are bearing most of the brunt of shipping disruptions this also has consequences for other products and commodities. Commodities with a lower level of perishability are also impacted by payment terms, which take much longer as produce queues at domestic and international ports. There is some evidence that 30-day payment terms can now take up to 120 days, affecting cash flow in the value chain and resulting in a failure to honour commitments. Simultaneously, higher interest rates are adding additional pressure in an environment where input costs – fuel, electricity, and fertilisers – are already surging. In addition, long-standing trade relations are affected, in more than just the perishable export industry. While some urgency is awarded to perishable products (which is understandable and justifiable), other industries such as nuts, wine, and maize are just as dependent on these logistic services and are also impacted.

As a result of SA’s dependency on imported farming inputs (specifically fertiliser, chemicals, and fuel) the broader agricultural sector could also be affected. If the necessary inputs are not available, timeously, and affordably, total agricultural output could be impacted. Nonetheless, freight rates are trending downwards, and new containers and container ships are on order and being built. Food inflation is already at higher-than-normal levels across the globe. Together with higher global interest rates tempering global aggregate demand, freight demand could normalise over the next 12 to 24 months. However, it is unlikely that average freight rates will normalise to pre-pandemic levels any time soon. A key uncertainty to the outlook is how China will manage COVID-19 going forward. If China’s zero-COVID policy remains, another lockdown with associated port disruptions would likely happen again towards the end of this year. Overall, the combination of the unreliability of global shipping lines, dramatic freight cost inflation, and severe challenges at domestic ports is affecting produce quality at destination, increasing unreliable arrivals, and resulting in claims and negative returns at a farm level.

If you have any questions or would like to discuss the subjects raised in this article with someone at Anchor please email us at info@anchorcapital.co.za.