Leading US private-label retail credit card bank, Synchrony Financial’s share price dropped by 10% on Friday (24 January), following the release of its 4Q19 results. However, we note that these results were good and slightly ahead of expectations and the share price reaction was as a result of the firm’s FY20 guidance. We can understand that the call created some uncertainty about earnings in 1H20, but we do think that it was an overreaction. We are happy with the results and we recommend retaining our holding in the stock. Synchrony’s share price was up 57.5% in 2019 (off a low base).

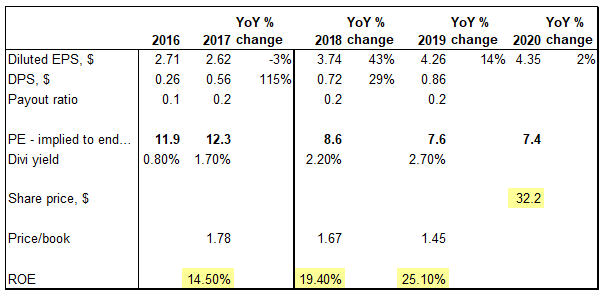

Figure 1: Synchrony Financial metrics

Source: Company data, Anchor.

The explanation below gives some background as to what the market appears to be concerned about:

Synchrony lost the Walmart credit card contract in 2019. The Walmart credit book was roughly 10% of Synchrony’s total credit assets at the end of 2018. This book was sold during 2019 and Synchrony now has excess liquidity on its balance sheet ($3bn out of a c. $19.8bn market cap). Much like when American Express lost the Costco contract several years ago, the challenge for Synchrony now is to deploy its surplus capital without damaging the overall return metrics of the firm (ROE of >20%), and to possibly create a more diversified portfolio than in the past (i.e. less exposure to traditional retail chains). We note that Synchrony does not face any large retail card contract renewals before 2022.

Synchrony has a net interest margin (NIM) of almost 16% (compared to that of the large banks, which are closer to 3%). The business charges an average yield on credit card balances of say 21%, which accounts for the bulk of its total credit book. So, when you sell 10% of your book (i.e. Walmart), the NIM returns will be diluted until you are, first, able to deploy the surplus capital, or, second, able to return the capital to shareholders via share buybacks.

First, the potential deployment of capital with new clients is probably the area which the market is concerned about. Walmart is a successful retailer in a US retail environment that is under stress. Online retail now accounts for 14% (and growing) of total US retail. Although overall retail sales have been buoyant, this has benefited a small number of companies (like Amazon) but hurt profitability across much of the sector, particularly department stores. For your reference about 1 in 10 listed retail companies (excluding food and drug retailers) have gone bankrupt since 2008, and the value of shopping malls has dropped by 30% in the past three years (as per a Financial Times [FT] article dated 28 January 2020). Fortunately, Synchrony has contracts with Amazon, Google and PayPal, but it also has many contracts with old line retailers such as Gap and JC Penney. Synchrony has also moved fast into the online space – 39% of its retail card transactions were digital in 4Q19. In other words, the company is not only shifting its client base to ecommerce companies but it is also helping traditional retailers to do more online. For 2020, Synchrony highlighted that it will be investing in its PayPal credit relationship and in its new Verizon contract (Verizon is the large mobile, and fixed-line, telco in the US).

Second, Synchrony is likely to return some of this excess capital back to shareholders via further share buybacks. This means that the share count could very well drop by a further 10% in 2020, following the 10% drop in 2019.

The net result is that Synchrony’s NIM will drop to 15% in 1Q20 (vs 15.78% in FY19). 20bps of this drop is due to the excess liquidity on the back of the Walmart sale. The balance appears to be largely due to investment in its PayPal and Verizon contracts as well as the fact that Walmart had a higher NIM than Synchrony’s overall book (we highlight though that it also had higher write-offs). Management are guiding for NIM to recover to 15.2%-15.5% for FY20, implying that the NIM for 2H20 could return to normal (the market appears to have doubts about this).

Synchrony is a well-run business that has been in existence since the 1920s. It was spun out from GE Capital in 2014 – under the leadership of CEO, Margaret Keane. The management team is very stable and Berkshire Hathaway owns 10% of the business.

Synchrony’s tangible book value/share as at 31 December 2019 stood at $19.50. The firm’s return on tangible equity for FY19 was 29.9%, although we highlight that this may be misleadingly high (in FY18 it was 22.4%). There is a new regulation known as current expected credit loss (CECL) which took effect in the US from 1 January 2020 and which concerns credit card businesses. Although this has no impact on cashflows it does reduce Synchrony’s book value by some 15%.

Synchrony does not have a specific dividend policy (although its payout ratio happens to be c. 20%) and it appears to spend far more on share buybacks than on dividends.