July was a relatively strong month for US equity markets, with less volatility than has been the case in recent months, although the performances of other major global markets were mixed. Many US states rolled back reopening plans as COVID-19 cases soared, while on the geopolitical front relations between China and the US deteriorated further. The two superpowers clashed over trade, technology and even territory, with the Trump administration imposing sanctions on Beijing over China’s policies in Hong Kong, challenging the country’s claims in the South China Sea and ejecting China from its Houston Consulate. This resulted in a tit-for-tat retaliation as China ordered the US to close its consulate in Chengdu.

Meanwhile, the big banks kicked off the US’ 2Q20 earnings season in mid-July and, thus far, most companies have reported strong earnings with the large-cap tech counters especially releasing strong results. Facebook, Amazon, Apple, and Alphabet (Google) all posted better-than-expected results, with Apple beating revenue expectations by a wide margin and Amazon reporting a blowout quarter as COVID-19 provided a tailwind for online shopping (a c. 50% YoY e-commerce revenue jump). While the big US banks had set aside billions in anticipation of expected losses, their actual charge-offs and delinquencies remained manageable for the quarter.

The Dow Jones Industrial Average (DJIA) gained 2.3% MoM but is down 7.8% YTD. However, the S&P 500 (+4.2% MoM) is now 0.5% in the green YTD, buoyed by the generally strong earnings and hopes that a COVD-19 vaccine will be available before the end of this year. The tech-heavy Nasdaq (+4.3% MoM and +18% YTD) remained 2020’s big winner as many large tech stocks continued to benefit from the stay-at-home economy. The US dollar came under pressure in July, with the US Dollar Index recording a 4%-plus drop as the US Federal Reserve (Fed) reinforced the existing narrative that stimulus will continue for the foreseeable future at its July policy meeting.

On the US economic data front, a 2Q20 GDP decline was widely expected considering that large parts of the economy were essentially shut for much of April and May. However, GDP recorded a 32.9% annual decline – slightly better than the 34.7% drop consensus economist forecasts were expecting but still the US’ worst quarterly performance ever. As might be expected the services sector was the largest contributor to the decline. July US consumer sentiment also fell against the backdrop of rising COVID-19 cases and expiring federal aid relief programmes, with the final reading of the July consumer sentiment survey slipping to 72.5 from 73.2 in June. US consumer sentiment is now barely above the pandemic low, erasing most of the momentum gained in late May and June as large parts of the US economy reopened. Unemployment data remained elevated and initial unemployment claims continue to rise with c. 1.4mn people filing for unemployment in the last full week of July – the second straight weekly increase.

The UK market underperformed, with the FTSE 100 Index down 4.4% last month (-21.8% YTD) as the government imposed fresh lockdown restrictions on parts of the UK and the index struggled against the pound’s gains (sterling climbed c. 6% in July). European equity markets closed lower on Friday (31 July), with Germany’s Dax basically unchanged MoM but down 7.1% YTD, while France’s CAC fell 3.1% MoM and is now down 20.0% YTD. On the data front, the eurozone economy contracted by 12.1% in 2Q20 – the lowest reading since records began in 1995. France’s GDP fell 13.8% in 2Q20, slightly better than expected, but still its worst on record, while Germany’s economy contracted by 10.1% in 2Q20 — its worst reading since records began in 1970.

In Asia, Japan’s Nikkei was down 2.6% MoM and is down 8.2% YTD. However, China outperformed with the Shanghai Composite Index jumping an impressive 10.9% in July (up 8.5% YTD), while Hong Kong’s Hang Seng rose 0.7% MoM (-12.8% YTD). The latest economic data continues to suggest that China’s economic recovery is well underway, with the country’s official July manufacturing purchasing managers index (PMI) coming in above expectations at 51.1 vs June’s 50.9, according to China’s National Bureau of Statistics (NBS). Reuters consensus economists had expected a 50.7 print. July’s non-manufacturing PMI came in at 54.2, down from 54.4 in June and slightly below consensus expectations of 54.5. Above 50 signals expansion, while below 50 indicates contraction. Earlier last month, data showed that China’s economy had recovered from it 6.8% contraction in 1Q20 with official GDP growth at 3.2% QoQ in 2Q20

On the commodities front, iron ore demand remained strong with the price hitting a one-year high around mid-July as governments around the world turn to infrastructure projects to help fuel economic growth and China’s iron ore imports jumped 17% in June. MoM, the iron ore price rose c. 9% in July. The platinum price was up 9.9% MoM, while palladium rose 5.3% in July. Crude oil prices ended the month c. 5% higher, reaching $43.30/bbl by month-end but YTD oil is still down c. 35%. Over the past two months investors have been buying bullion on the back of mounting concerns surrounding surging COVID-19 cases in the US and renewed tensions between the US and China. This resulted in gold having another great run in July (up 10.9% MoM and 30.2% YTD), closing the month at $1,975.86/oz after reaching new all-time highs last week. The global backdrop for gold (and other precious metals prices) remains stable thanks to expansionary monetary policy responses, which has seen real yields continue to fall and remain depressed – an environment that has, historically, proven positive for precious metals prices.

The JSE’s performance for July was mixed, with impressive gains from resources on the back of strong gold and precious metals prices, while industrials underperformed. Still, the FTSE JSE All Share Index closed Friday 2.5% higher MoM (-2.4% YTD), buoyed by strong share price gains from various large-cap resource shares including Glencore (+11.5% MoM), AngloGold Ashanti (+9.7% MoM), Anglo American (+4.2% MoM), Anglo American Platinum, and BHP Group (both up 4.0% MoM). While industrials underperformed (the Indi-25 was down 1.3% MoM [+7.5% YTD]), resources soared by 8.3% in July (+12.8% YTD) and the Fini-15 advanced by 1.2% MoM (-35.2% YTD). Among the large industrials, Anheuser Busch InBev (AB InBev) jumped 10.3% MoM, while Prosus rose 2.5% MoM and Naspers disappointed with a 0.3% share price decline. The rand strengthened 1.6% in July (down 21.9% YTD), closing at R17.07/$1 as the greenback weakened although the local unit saw renewed pressure towards month-end as the impact of the pandemic was seen in emerging market economic data releases.

SA’s headline consumer price inflation (CPI) slowed to 2.1% YoY in May, its lowest level since September 2004, and vs April’s 3.0% print. MoM, CPI was down 0.6% compared with a 0.5% MoM decrease in April. May core inflation, which excludes food, non-alcoholic beverages, fuel, and energy prices, slowed to 3.1% YoY vs 3.2% in April. MoM core inflation declined 0.2%. The SA June trade balance widened further to a R46.6bn surplus (the largest since c. January 1990) vs a revised R19.7bn surplus in May. Exports jumped 10.1% MoM to R116.3bn, while imports fell 18.9% to R69.7bn. On 23 July, the SA Reserve Bank (SARB) announced a widely expected 25-bpt rate cut, bringing the SARB’s total rate cuts YTD to 3.0%, with the repo rate now at 3.5% – its lowest level since the early 1970s

With March’s hard lockdown gradually being eased to allow more businesses and sectors of the economy to open, SA’s total number of confirmed COVID-19 cases rocketed to 493,183 at end-July (vs 151,209 as at 30 June). The total number of local COVID-19 deaths now stand at 8,005 vs 2,657 as at the end of June, with 326,171 recoveries (a recovery rate of 66%). The US continues to account for the most COVID-19 infections worldwide at 4.5mn, followed by Brazil (2.7mn), India (1.8mn), the Russian Federation (850,870) and South Africa in fifth spot.

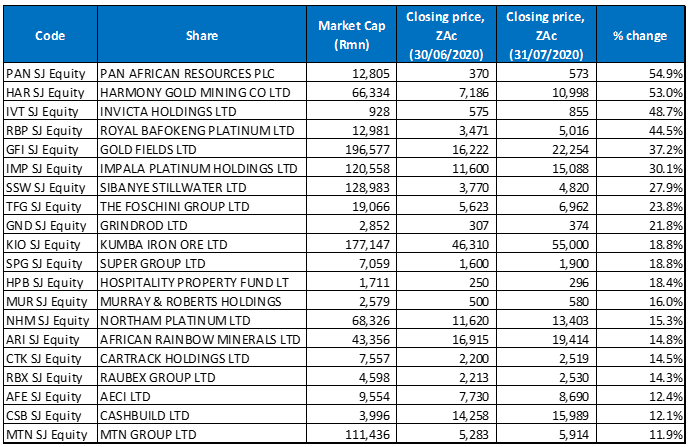

Figure 1: The 20 best-performing shares in July 2020, MoM

Source: Anchor, Bloomberg.

Apart from Invicta, Foschini and Grindrod, all of July’s top-10 MoM performers came from the resources sector with gold counters especially recording impressive gains. Pan African Resources was July’s best performer as its share price soared 54.9% MoM. The company said last month that it expected to be debt-free within the next 12 months due to the record gold price which would also see the firm cutting c. half of Group net debt during the year ended June on better-than-expected output. The firm added that its annual FY20 gold output had climbed by 4.1% YoY, despite the severe impact of lockdown restrictions, and it also increased its FY21 production guidance to 190,000 ounces. Gold breached the $1,980/oz price level last week for the first time since 2011 and SA gold miners’ share prices have been on a roll as the economic disruption created by the pandemic, as well as the consequent central bank stimulus efforts, sent investors to gold. The yellow metal has always been regarded as a safe-haven asset, meaning that it is not correlated to the economy as a whole and can instead maintain or even increase in value during periods of high market volatility such as we have been experiencing this year.

Another gold miner, Harmony (+53.0% MoM), was July’s second-best performing share. It was followed by investment holding company, Invicta (48.7% MoM). Invicta’s share price jumped after it entered into an agreement with CNH Industrial SA to sell four of the businesses within its Capital Equipment Group (CEG) segment for c. R507mn to service its debt. The disposal will be effective next year once regulatory approvals and outstanding suspensive conditions had been met.

Royal Bafokeng Platinum, Gold Fields, and Impala Platinum (Implats) recorded MoM share price gains of 44.5%, 37.2% and 30.1%, respectively. Implats saw its share price jump c. 5.5% on the day it flagged a strong rise in full-year earnings due to better selling prices for its metals. In a trading statement, the platinum miner said headline earnings per share (EPS) would be “significantly more than 20% higher …” than the ZAc423 it reported last year. Implats attributed this to a large increase in the dollar basket price for platinum group metals (PGMs) and a weaker rand, which had resulted in a much higher rand PGM basket price. Implats also revised its refined production guidance for the year to between 2.77mn to 2.795mn 6E ounces from 2.6mn to 2.9mn ounces, previously.

Implats was followed by Sibanye Stillwater with a 27.9% MoM gain, and retailer Foschini Group, which rose 23.8% MoM. Foschini said in a trading update for the three months ended 27 June 2020, that its retail turnover declined 43.0% YoY, with significant trading disruptions caused by government-enforced lockdowns and regulations on social distancing in all three of its major operating territories – SA, the UK and Australia. However, it also said that it had submitted a conditional offer to acquire c. 371 Jet stores from Edcon’s administrators, an announcement which saw the share price surge.

Investment holding company, Grindrod (+21.8% MoM) and Kumba Iron Ore (+18.8% MoM) rounded out July’s 10 best-performing shares. For 1H20, Kumba reported an 8.5% YoY revenue decline to R31.58bn, while HEPS were down 17% YoY to R26.19 – in line with its guidance. Kumba also announced an interim dividend of R19.60 (a 75% payout ratio) implying a supportive 7.1% annualised dividend yield. Separately, the iron ore miner announced the approval of its Kapstevel South project at its Kolomela mine by both the company and Anglo American’s boards. The total capital cost of the project is expected to be c. R7.0bn, including pre-stripping.

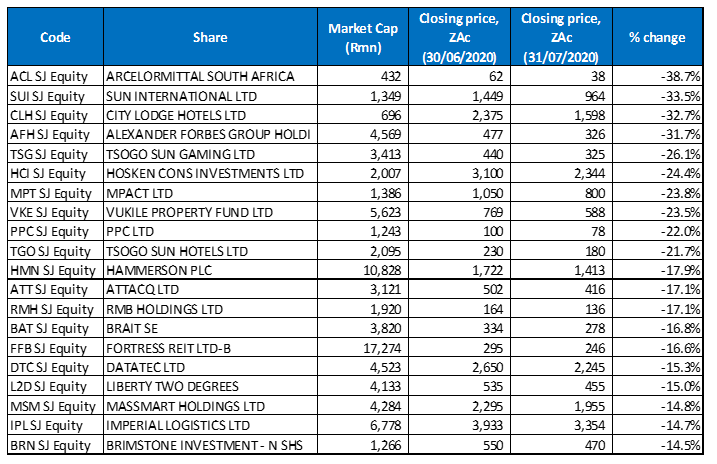

Figure 2: The 20 worst-performing shares in July 2020, MoM

Source: Anchor, Bloomberg.

Steel producer, ArcelorMittal SA was July’s worst-performing share – down 38.7% MoM. In its 1H20 results, released last week, the company said that revenue dropped to R12.01bn from R21.74bn posted in 1H19, while its diluted loss per share stood at ZAc211.0 vs ZAc59.0 recorded in the same period of the prior year. These results came as steel demand dropped due to COVID-19 and on the back of output declines after its operations were shut during lockdown. Rising costs (such as materials, electricity, etc.) added to the Group’s operational woes.

July’s second-worst performer, Sun International, had recorded a 101.7% MoM share price surge in June but gave back up some of these gains in July as the share closed Friday (31 July) 33.5% in the red. The cash-strapped company last month announced that it would tap shareholders for funds at R9.44/share in a R1.2bn rights issue. The rights issue funds will be used to improve its short to medium-term liquidity and to strengthen its balance sheet as the COVID-19 imposed lockdown restrictions continue to impact its operations.

City Lodge Hotels was July’s third-worst performer with a share price drop of 32.7% MoM. In its 9M20 results released last week, the hotel chain stated that its revenue dropped to R1.13bn from R1.18bn posted in the corresponding period of 2019, while its diluted loss per share stood at ZAc862.6, compared with diluted EPS of ZAc469.6 in the same period of the prior year. City Lodge’s FY20 trading statement, also released in July, showed that the company expected a headline loss per share of between ZAc369.6 and ZAc403.3 compared with HEPS of ZAc561.7 in FY19.

City Lodge was followed by diversified financial services Group, Alexander Forbes, Tsogo Sun Gaming and Hosken Consolidated Investments (HCI) which posted MoM declines of 31.7%, 26.1%, and 24.4%, respectively. The Alexander Forbes share price decline was partly a result of a special dividend of ZAc50, which accounted for a third of its price decline. The company ended its FY20 on a low note as the positive market returns it had recorded in the first nine months of its financial year were reversed in the last quarter. Assets under administration and management fell 9% YoY to R310bn, owing to a negative market performance mostly in March, while HEPS dropped 20% YoY from ZAc44.2 in FY19 due to COVID-19 induced market disruptions. The company said that the operating environment has become more complicated, uncertain, and difficult with the pandemic and the country’s economic prospects. Meanwhile, Tsogo Sun Gaming, which had seen its fortunes turn around in June when it was the month’s top-performing counter with an impressive 106.6% share price gain, fell 26.1% in July after the prior month’s strong run.

Last week, paper and plastic packaging firm, Mpact (-23.8% MoM) released a trading statement in which it said that it expected 1H20 revenue to decrease by 1.4% YoY and HEPS to be between ZAc5.0 and ZAc11.0, compared with the ZAc39.0 recorded in the previous year. This was on the back of electricity disruptions (according to Business Day, the failure of a municipal substation in Ekurhuleni cost one of Mpact’s mills 22 production days and R27mn), and weak international demand for some of its paper products.

Rounding out the 10 worst-performing shares were Vukile Property Fund (-23.5% MoM), PPC Ltd (-22.0% MoM) and Tsogo Sun Hotels (-21.7% MoM). In a July trading update, PPC said that it expected its FY20 HEPS to drop by over 20.0% YoY, compared with FY19 HEPS of ZAc20.0. The cement manufacturer also said that its cement operations ramped up in May 2020 post the lifting of the COVID-19 restrictions imposed across most of the jurisdictions in which it operates. SA sales volumes plunged an estimated 95% in April, with volumes in Rwanda and Zimbabwe also under pressure. It added that May’s SA volumes were still down c. 30%-35%, while its international volumes were just 5% lower due to strong sales in Rwanda. PPC noted that the general economic environment and the pandemic would have a material impact on impairments, expected credit losses and other fair value adjustments.

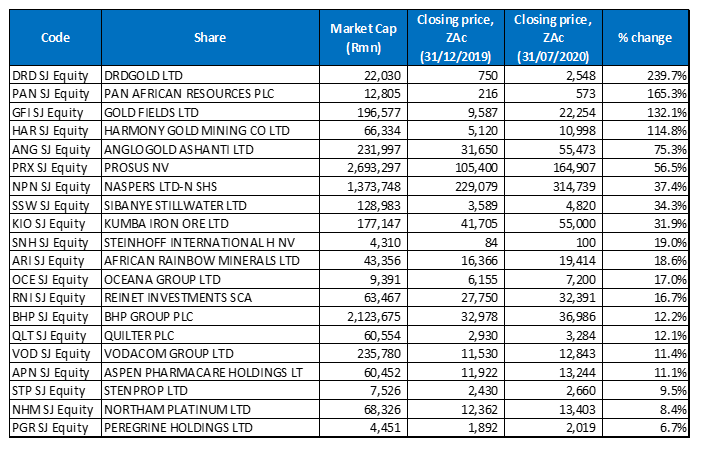

Figure 3: Top-20 YTD performers (to end July 2020)

Source: Anchor, Bloomberg

With the price of gold soaring it is not surprising to find that six of the ten best-performing stocks YTD are gold counters – DRDGold, Pan African Resources, Goldfields, Harmony Gold, AngloGold Ashanti, and Sibanye Stillwater. Gold’s rally (+30.2% YTD) this year has seen the gold price recently reaching 11-year highs and, with gold counters ultimately leveraged to the price of the yellow metal, these shares are tracking the gold price higher. In addition, 17 of June’s YTD best-performing shares remained among the 20 best performers for the year to end July. African Rainbow Minerals, Quilter and Northam Platinum were last month’s new entrants into the YTD top-20, bumping British American Tobacco, Lighthouse Capital, and Investec Australia Property from the YTD top-performers list.

The top three YTD performers were unchanged from the year to end June, with DRDGold remaining the top performer YTD for a fifth month running. It was once again followed by Pan African Resources (+165.3% YTD) and Goldfields (+132.1% YTD) in second and third spot, respectively.

Harmony, with a 114.8% YTD gain, was in fourth place, followed by AngloGold Ashanti (+75.3% YTD) in fifth position. Prosus (+56.5% YTD), which has been spurred along by growth in online gaming during the various lockdown periods and its investment in Chinese gaming juggernaut Tencent, took sixth spot, after gaining a further 2.5% in July.

Prosus was followed by Naspers (+37.4% YTD), with Sibanye Stillwater (+34.3% YTD), Kumba Iron Ore (+31.9% YTD) and Steinhoff (+19.0% YTD), rounding out the top-10 YTD performers.

Figure 4: Bottom-20 YTD performers (to end July 2020)

Source: Anchor, Bloomberg

Looking at the year to end-July’s worst performers, three shares entered the arena with ArcelorMittal (-68.1% YTD), Massmart (-61.9% YTD) and Arrowhead Properties (-61.3% YTD) replacing Invicta, Octodec and The Foschini Group. Invicta’s sterling performance in July, which saw its share price jump 48.7% MoM, pushed it out of the 20 worst-performing shares list, while Octodec and Foschini’s July gains of 5.7%, and 23.8% MoM, respectively, resulted in these counters also moving out from among the twenty worst-performing shares YTD.

Nampak (-83.0% YTD) was once again the YTD worst performer, with the share price recording a 10.1% MoM decline in July. After its poor performance last month, City Lodge has been bumped to second position with a 77.8% YTD drop. It was followed in third place by Sun International, which is now down 75.8% YTD after its share price dropped by 33.5% MoM in July.

UK and Europe shopping centre owner, Hammerson (-75.0% YTD), HCI (-74.2%), Tsogo Sun Gaming (-73.5%), Brait SE (-72.1%), Vukile Property Fund (-69.7%) and PPC (-68.8%) rounded out the ten worst-performing shares YTD.