Trade war worries seemed a distant memory as ongoing fears around the impact of the novel coronavirus (COVID-19, Wuhan flu or 2019-nCoV) and infections spreading outside of China resulted in investors growing increasingly concerned about the virus’ impact on global economic growth and company profits. Markets across the globe ended February in the red in a volatile month for world equities as worries about the virus outbreak mounted following a spike last week in Italy and South Korea, with a new case also reported in California on Friday (28 February) and the US Centers for Disease Control and Prevention saying it expects the cases in the US to rise. Thus far, the virus has infected more than 83,000 people worldwide (of which 95% is in China) and been a dominant theme in US earnings releases and on companies’ conference calls as firms such as Apple, Microsoft, Starbucks, Mc Donald’s, etc. continue to warn that they won’t meet 1Q20 earnings targets because of the virus.

In the US, the three major stock indices posted their worst weekly percentage declines since the global financial crisis (GFC). The Dow ended February 11.0% lower MoM (-10.1% YTD) after the index dropped 1,191 points or 4.4% on Thursday (27 February) – its worst one-day point drop in history. The S&P 500 lost 8.6% (-8.4% YTD), while the Nasdaq closed Friday 4.5% down MoM (-6.4% YTD) – over 10% below its recent peak. However, while indices fell into correction territory last week, we highlight that, according to Bloomberg, stocks still aren’t close to a bear market, which is defined as 20% or more below the most recent peak. The S&P 500 and the Dow ended February 12% and 10% below their most-recent peaks, respectively. US 10-year government bond rates have also reached an all-time low, with markets having moved to price-in at least two rates cuts by the US Federal Reserve (Fed) in the next few months

Still, the US economy remains resilient and, on the US economic data front, a second reading of 4Q19 GDP left growth unchanged at 2.1%. The University of Michigan’s monthly consumer sentiment survey saw the final read of February consumer sentiment beat expectations and rising to its highest level since March 2018. However, it did warn that the “domestic spread of the virus could have a significant impact on consumer spending.” Meanwhile, the CBOE Volatility Index (VIX), which represents the market’s expectation of 30-day forward-looking volatility (and is referred to as Wall Street’s “fear gauge”), surged to 49.15 last week – its highest intraday level since February 2018.

In the UK, the FTSE 100 also fell into correction territory towards the end of the month in that market’s first correction since December 2018. MoM, the index was down 12.8%, while YTD it has lost 9.7%. Shares in Europe closed February with their worst weekly performance since the 2008 GFC as the spread of COVID-19 outside China saw continued selling. Germany’s DAX was down 10.3% MoM (-8.4% YTD), while the CAC ended February 11.2% lower (-8.5% YTD).

In Asia, Chinese markets, which were closed from 23 January to 3 February for an extended Lunar New Year holiday, recorded losses across the board. MoM, Hong Kong’s Hang Seng lost 7.3% (-0.7% YTD), while the Shanghai Composite was down 5.6% for the month (-3.2% YTD). On the economic data front, China’s official manufacturing purchasing managers’ index (PMI) plunged to 35.7 in February from 50.0 in January (a reading above 50 indicates expansion, while below 50 signals contraction). This was its worst decline on record as the damage caused by the COVID-19 outbreak suggested deepening cracks in an economy that was already negatively impacted by the trade war. In Japan, stocks also recorded major declines with the Nikkei plummeting by 10.6% MoM (-8.9% YTD).

On the commodity front, crude oil prices dropped around 13% in February closing the month at $50.52/bbl, while US oil traded at $44.76 – their lowest prices since late 2018. While the gold price initially rose on COVID-19 fears, its reputation as a safe haven during financial turmoil was tarnished on Friday as the yellow metal suffered one of its worst one-day drops on record. This after hitting a seven-year high at close to $1,700/oz on 24 February. MoM, the gold price was down 0.2% but it remains up over 4.5% YTD. Despite supply tightening as weather events squeezed exports from such key suppliers as Australia and Brazil, benchmark iron ore prices lost c. 6.5% in February amid expectations that end-users in China would lower production levels or even idle some capacity. The price of platinum was also down c. 14% MoM, while palladium continued to rise MoM, jumping by 13.7%, despite plummeting by 10.2% on 28 February – its worst one-day drop since the GFC. A February PGM Market report by Johnson Matthey estimates that the supply deficit for palladium had widened to c. 1.2mn oz in 2019 and is expected to deepen this year, as stricter emissions legislation in China and Europe drive up vehicle palladium loadings.

In South Africa (SA), the JSE ended February red across the board, with the FTSE JSE All Share Index closing the month 9.0% down (-10.6% YTD) as the share price of market-cap heavyweights such as Anheuser Busch InBev (-22.4% MoM), BHP Group (-13.8% MoM), British American Tobacco (BAT: -7.8% MoM), Naspers (-3.2% MoM), and Prosus (-2.4% MoM) were battered. On 24 February, the benchmark index had suffered its biggest fall since December 2008 (according to Bloomberg), dropping by 4.46% on the day, as fears of rising COVID-19 cases outside China sparked an initial global sell-off. Concerns ahead of the Budget speech and worries that a slowdown in China’s demand for commodities could impact the local economy also weighed on the bourse. Commodity prices and counters didn’t escape the contagion and the Resi-10 was pulled 11.6% lower MoM (-14.7% YTD), while the Fini-15 lost 8.2% MoM (-13.5% YTD) and the Indi-25 closed the month 6.5% down (-4.6% YTD). The rand also came under pressure, dropping by 4.2% MoM against the dollar.

On the economic data front, annual consumer price inflation (CPI) advanced for the second month running, coming in at 4.5% in January (vs 4.0% in December) – the midpoint of the SA Reserve Bank’s monetary policy target range. The higher number was due to increases in the prices of fuel, food and utilities. Housing and utilities, especially, contributed 1.2 ppts, and transport costs 0.9%. MoM, price growth remained at 0.3%. Headline CPI (which excludes the volatile food and fuel component) also quickened to 4.5% YoY, vs 4.0% in December. Meanwhile, January’s trade balance swung to a deficit of R1.87bn from a revised R13.89bn surplus in December, while exports fell 1.4% MoM to R101.4bn and imports rose 16.1% MoM to R103.3bn. Last month, Moody’s also cut SA’s 2020 GDP growth forecast to 0.7% (from 1.5%), citing a stalling economy and the impact of power outages as reasons.

On Wednesday (26 February), Finance Minister Tito Mboweni delivered his highly anticipated 2020 Budget Speech and, for the most part, it was favourably received by market analysts and economists, although we note the implementation will be key. Mboweni said SA intends to cut c. R160bn from the public sector wage bill to contain a rising budget deficit, but this depends on renegotiating wage agreements with labour unions, which is likely to be extremely difficult. Other positive highlights included no tax increases (and even some reductions), an infrastructure drive, and more money for law enforcement including the NPA. We are very positive on the budget and we think that government is finally looking at addressing the real problems impacting our economy rather than just fighting the symptoms. While we accept government may not be able to achieve all that it is hoping, we believe the paradigm shift towards acknowledging the real issues and starting to address these is immensely positive. This may, in time, prove to have been a turning point for the economic tide in SA.

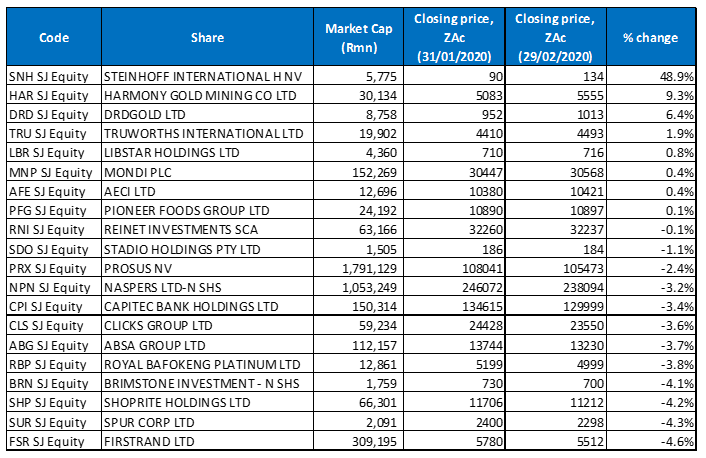

Top-20 February 2020, MoM

Source: Anchor, Bloomberg

Retail holding firm, Steinhoff International (+48.9% MoM) was February’s best-performing share, albeit from a very low base. The share price initially jumped in early February after a report on Sky News that it was in talks to sell its European cut-price retail chain, Pepco for EUR4.5bn (R86.5bn). Pepco has more than 1,600 stores in Central and Eastern Europe, as well as the UK chain Poundland, and Dealz, which has businesses in Ireland, Poland and Spain. In its 1Q20 trading update, Steinhoff said that its revenue rose 7.0% YoY to EUR3.44mn, with growth driven by the performances of Pepco Group and Pepkor Africa. Revenue from continuing operations rose to EUR3.4bn from EUR3.2bn in 1Q19.

Steinhoff was followed by Harmony Gold, which recorded a share price jump of 9.3% MoM. Early in February, Harmony released a 1H20 trading statement, which showed that it expects HEPS and EPS to be around ZAc249 vs a loss per share of ZAc4 in the same period of 2019. Harmony said it expects revenue to increase by 12.0% YoY, due to higher gold prices. The gold miner also consolidated its position as SA’s biggest gold producer by volume after being picked for the R4.46bn acquisition of AngloGold Ashanti’s remaining local assets, including Mponeng, the world’s deepest gold mine.

In third spot, DRDGold (January’s best-performing share), jumped a further 6.4% MoM last month. In February, DRDGold announced that it planned to venture into the platinum group metals (PGM) sector. Earlier in the month, DRDGold had reported a 69% YoY surge in Group revenue to R2.1bn. This was on the back of higher gold production and gold sold, coupled with a 26% jump in the average rand gold price received. This solid performance was despite DRDGold being hit by load shedding.

DRDGold was followed by Truworths (+1.9% MoM), Libstar Holdings (+0.8%), Mondi and AECI Ltd (both 0.4% higher MoM). Truworths’ 1H20 results earlier in the month seem to have given the share price a much-needed boost, although the counter came under pressure again last week. For 1H20, Truworths, which has seen challenging trading conditions in its African and UK markets, said that its revenue rose to R11.03bn from R10.90bn posted in 1H19, while diluted EPS increased by 0.5% YoY to ZAc363.30. Consumer goods Group, Libstar, said last week that it expects double-digit profit in FY19 as it benefits from improved margins and a reduction in debt. Libstar forecast headline EPS to rise by between 7.2% and 12.2% YoY (this includes the effects of accounting changes, which bring leases on to the company’s balance sheet). The firm also said that its gross profit margins had improved in each of its product categories.

For FY19, paper and packaging Group, Mondi Plc reported flat earnings albeit with a brighter outlook and price stability ahead. Mondi posted a EUR1.1bn (R18.22bn) profit – basically unchanged from the EUR1.11bn recorded in FY18 as it battled a weaker pricing environment for container board and uncoated fine paper to deliver flat annual earnings. In addition, the firm said it plans to spend billions of rand in expanding its manufacturing plants despite falling prices for paper and pulp grades weighing on profit.

Rounding out the top-10 performers were Pioneer Foods (+0.1% MoM), followed by Reinet Investments and Stadio Holdings – down 0.1% and 1.1% in a poor month for the JSE. In February, the Competition Commission recommended to the Competition Tribunal that the $1.70bn acquisition of Pioneer Foods, by US snack giant PepsiCo be approved with conditions. Last month, Stadio Holdings said in a trading statement that its core headline earnings will be up to 29.9% higher YoY. The tertiary education Group announced that FY19 earnings and headline EPS would be between 3.5% and 14.5% higher YoY vs the ZAc7.8 it reported in FY18. It also said core HEPS would rise by as much as 29.9% YoY (from ZAc8.6).

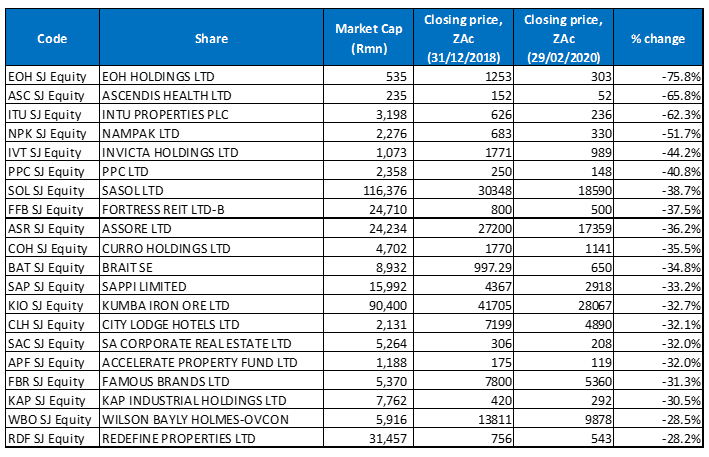

Bottom-20 February 2020, MoM

Source: Anchor, Bloomberg

EOH Holdings was February’s worst-performing share, plummeting by a staggering 63.0% MoM, with the share price hitting levels last seen in 2004. Business Day wrote last week that the sell-off could be due to ongoing concerns about the Group’s history of corporate governance. The article noted that EOH is in the midst of cleaning up its balance sheet following allegations of underhanded dealings with government, forcing the company into taking billions of rand in write-down charges and losing c. R1bn. CEO Stephen Van Coller has taken a hard line against corruption.

For the second month running, Ascendis Health was the second-worst performing share – down 47.5% MoM. This, despite saying in February that it has been given a revenue boost by Cyprus-based Remedica, which it is still considering selling. Ascendis has been grappling with a hefty debt burden – its liabilities of R8.6bn as at the end of June 2019 exceeded its assets by R400mn.

Invicta was the third worst-performing share – declining 36.5% MoM. The industrial Holdings firm said in February that it is considering shaking up its capital allocation structure and may tap shareholders or dispose of non-core assets. Invicta, which has subsidiaries that include distributors of capital equipment, spare parts and engineering consumables, also indicated that it is considering realigning its debt, and conducting specific inventory reduction programmes. The company’s share price plummeted 49.1% in 2019 and has fallen a further 44.2% YTD. It recently appointed Steven Joffe as CEO.

PPC, Fortress REIT -B-, Nampak and City Lodge reported MoM losses of 35.7%, 33.2%, 32.7% and 31.7%. Nampak said last month that the Competition Tribunal has approved the sale of its glass business, although certain conditions still need to be fulfilled. Meanwhile, City Lodge’s share price slid after it reported 1H20 results in February, which showed that its revenue increased to R809.25mn from R807.41mn posted in 1H19, but diluted EPS fell 67.0% YoY to ZAc126.40, hurt by weaker trading conditions and the adoption of IFRS 16 leases.

UK-based mall owner, Intu’s share price remained under pressure in February, losing a further 36.5% after plunging 45.0% in January and dropping by 70.4% in 2019. Last month, Intu was dealt a further blow after a Hong Kong-based investor (Link REIT) pulled out of plans to take part in the Group’s capital raise – a day after it had confirmed talks. Intu is struggling under GBP4.7bn (c. R89.9bn) in debt and had previously confirmed it would announce an emergency cash call, expected to be worth at least R19.1bn to coincide with the release of its FY19 results.

Rounding out February’s worst performers were Assore and Curro Holdings which recorded MoM declines of 29.2% and 28.8%. Mining holding company, Assore reported disappointing 1H20 results last month, which showed that its revenue declined 12.2% YoY to R3.47bn, while its diluted EPS stood at R20.14, vs R28.27 recorded in the corresponding period of 2019. The earnings declines were driven by an 11% iron ore sales volume drop and poor prices for manganese ore and chrome ore. According to Assore, the decline in iron ore sales volumes was due mostly to the timing of shipments.

Curro also reported disappointing FY19 results, which showed that recurring headline EPS were down 15% YoY to ZAc51, while revenue rose to R2.94bn from R2.50bn posted in the previous year. Curro said that despite the number of learners increasing by 12% YoY to 57,597 in 2019, an increase in bad debts and “economic pressure” in certain schools had eaten into its profits.

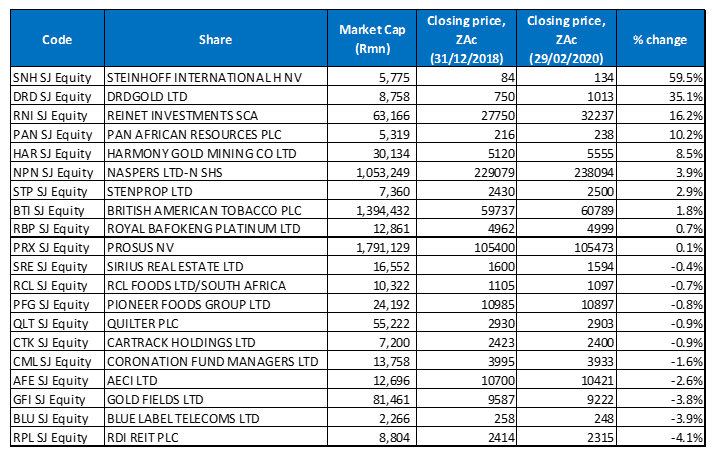

Top-20 February 2020, YTD

Source: Anchor, Bloomberg

Four of the top-10 MoM best-performing shares also featured among the YTD best performers, with Steinhoff (+59.5% YTD, discussed earlier) taking the top spot in both rankings. DRDGold moved up a spot YTD to the second-best performing share (it was the third-best performer MoM), with a 35.1% YTD gain. In third position was Reinet with a 16.2% YTD rise. Reinet’s share price advanced by 16.3% in January, which pushed the share up the rankings after the 0.1% MoM loss it recorded in February.

Reinet was followed by Pan African Resources, Harmony Gold (discussed earlier), Naspers, and Stenprop with gains of 10.2%, 8.5%, 3.9% and 2.9% YTD. Naspers’ share price was down 3.2% in February, but the share had gained 7.4% in January, when Naspers raised c. R24bn through the sale of 22mn ordinary Prosus shares – just 90 minutes after the announcement of the offering was made, the sale was completed. Each Prosus share was sold for EUR67.50 (c. R1,080) resulting in gross proceeds of c. EUR1.5bn (c. R24bn), Naspers said in a shareholder notice.

BAT (+1.8% YTD), Royal Bafokeng Platinum (++0.7% YTD) and Prosus NV (+0.1% YTD) rounded out the YTD top 10.

Bottom-20 February 2020, YTD

Source: Anchor, Bloomberg

Looking at the YTD worst performers, with the exception of Sasol which replaces City Lodge among the YTD worst performing shares, the remainder were unchanged from the MoM rankings. As with the MoM worst performers, EOH Holdings (-75.8%) and Ascendis Health (-65.8%) were the two worst-performing shares but in third spot, Intu (-62.3%) moved down a few notches vs its MoM performance, replacing Invicta (-44.2% YTD) as the third-worst performing counter.

YTD, Nampak, PPC and Sasol lost 51.7%, 40.8% and 38.7%, respectively. Sasol had a challenging six months as its Lake Charles woes continued to impact profit. On 24 February, Sasol reported disappointing 1H20 results with headline EPS falling 74% YoY to R5.94, due to a combination of weak oil (a 9% YoY drop in the rand per barrel price of Brent crude) and chemicals prices as well as heavy Lake Charles Chemicals Project (LCCP) capital expenditure continuing to pressure the balance sheet. Sasol did say that it is anticipating that LCCP will start generating positive earnings before interest, tax, depreciation and amortisation (EBITDA) in 2H20. Capex spending should also ease going forward, as it is guided to nearly halve (-46%) from R56bn in FY19 to R30bn in FY21 (FY20 guidance: R38bn). Not surprisingly, Sasol’s dividend was also cut for this period and a final dividend is also very unlikely.

Fortress REIT -B- (-38.7% YTD), Assore (-36.2% YTD) and Curro (-35.5% YTD) accounted for the remainder of the 10 YTD worst-performing shares.