The last month has seen a meltdown of epic proportions in economies and stock markets around the world, with dizzying moves in equity prices and other assets. The worldwide sell-off, sparked by two black swan events – the rapidly increasing novel coronavirus (COVID-19) infections and an unanticipated Russian assault on the oil price – worsened as governments implemented lockdown measures to fight the spread of virus. While much has been written about the impact of COVID-19 and the lockdowns put in place by various governments (including South Africa [SA]), the oil price drop came after OPEC, led by Saudi Arabia, met with its allies on 6 March to discuss a response to falling oil demand on the back of the growing spread of COVID-19. Unable to reach agreement with Russia around OPEC’s demand to cut 1.5mn barrels of oil production a day, Saudi Arabia announced it would open the spigots and cut its oil prices by upwards of $6/bbl. This saw oil prices plummet and by the end of the month the price of Brent Crude was down 55% – its worst month since 1983. In unprecedented times, fears run high and in March investors seemed to be dumping all assets. Even gold, usually regarded as a safe haven, saw its price fall before recovering again and ending the month only 0.5% lower (for 1Q20 the price is still up 3.9%).

In the US, March was the worst month for markets since the Great Depression with the three major stock indices recording significant MoM losses. The Dow ended March 13.7% lower MoM and for 1Q20 the index recorded its worst quarter in history – down 23.2%. MoM, the S&P 500 fell by 12.5% and logged its worst quarter since 4Q08 – down 20.0%. Even the usually reliable Nasdaq lost ground, closing 10.1% down MoM – its worst monthly performance since November 2008, according to Reuters. 1Q20 was also the tech-heavy index’s worst quarter since 4Q18 as it recorded a 14.2% drop. During the month, a proactive US Federal Reserve (Fed) announced two emergency rate cuts, which brought the Fed’s overnight bank borrowing rate back to near zero, and rolled out other emergency measures almost on a weekly basis including relaunching large-scale asset purchases (quantitative easing [QE]).

An initial lacklustre response to the pandemic by the Trump administration has seen over 3,000 deaths in the US with over 164,000 cases confirmed as the country has become the new epicenter of the virus over the last few days. Congress has deployed a massive $2trn stimulus package to cushion the economic blow from COVID-19 and is looking at taking additional steps to manage the mounting human impact. On the economic data front, US jobless claims hit a record of 3.3mn last week, with a Dow Jones survey of economists stating that an additional 2.7mn claims could be filed this week, as struggling businesses lay off workers.

The UK’s FTSE 100 plummeted 13.8% in March and delivered its worst quarter since 1987 on the back of COVID-19 investor panic – down 24.8% in 1Q20. European markets had a torrid month (and quarter), with Germany’s Dax falling by 16.4% MoM and 25.0% in 1Q20. France’s CAC ended the month 17.2% in the red and dropped by 26.5% for the quarter. With Europe (Italy and Spain in particular) becoming the epicenter of the virus in early March, the latest economic data show economic activity plummeting to record lows, with steep declines in manufacturing and services. The March IHS Markit eurozone manufacturing purchasing managers index (PMI) fell to 44.5 from 49.2 in February – a seven-and-a-half-year low. We note that levels above 50 indicate expansion, while below 50 shows contraction. The PMI report stated that the sharp decline from February’s 49.2 print was primarily due to COVID-19 related shutdowns. To assist Europe’s financial system, the European Central Bank (ECB) has announced that it will buy an extra EUR750bn of bonds over the next nine months, including both sovereign and corporate debt.

In Asia, China’s Shanghai Composite was down 4.5% MoM and fell 9.8% in 1Q20. However, according to The South China Morning Post it remains the only major stock market index not in bear territory. Hong Kong’s Hang Seng lost 9.7% MoM and is down 16.3% for the quarter. In some good news, China factory PMI data released on 31 March showed an unexpected bounce for the month after plunging to a record low in February (when China was effectively shut down because of the virus). This indicator provides some hope for global markets as commentators believe that this could indicate an early phase China-led economic rebound. In Japan, stocks also recorded major declines with the Nikkei down 10.5% MoM (-20.0% in 1Q20).

On the commodity front, iron ore prices see-sawed in March before settling higher at month-end, fueled by demand hopes after the unexpected rise in China’s March factory activities. In addition, iron ore stockpiles at Chinese ports fell for a second straight week (to 121.25mn tonnes) – the lowest level in c. eight months. MoM, benchmark iron ore prices gained c. 1.8%. Government lockdowns globally weighed on metals prices with platinum down c.16% MoM, while the price of palladium, which has seen a bull run over the past 24 months or so, could not escape the carnage and dropped by 9.9% MoM.

In SA, the JSE ended March red across the board, with the FTSE JSE All Share Index (ALSI) falling 12.8% MoM (-22.1% for 1Q20) as the share price rout impacted most of the counters in the index, and only 25 out of the 158 stocks in the ALSI recording MoM gains. The share prices of market-cap heavyweights such as Glencore (-27.7%), Anglo American (-13.9% MoM), Anheuser Busch InBev (-9.8% MoM), Richemont (-7.1% MoM), and BHP Group (-3.7% MoM) were battered. However, despite extreme volatility, Prosus (+17.1%) and Naspers (+7.3%), managed to end March significantly higher. The benchmark index also suffered several historic daily falls last month, losing 6.2% on 9 March, 8.3% on the 16th and 7.2% on 18 March. However, on 12 March the ALSI closed 9.7% lower on the day – its worst daily drop since the market crash of 1997. This came as fears around COVID-19 as well as the impact of measures taken by various governments to curb the spread of the virus swept across world markets.

Commodity prices and counters didn’t escape the contagion and the Resi-10 was pulled 13.1% lower MoM (-25.9% in 1Q20), while the Indi-25 ended the month 2.2% down (-6.7% in 1Q20). Banking and financial counters were the worst hit, with the Fini-15 plummeting 30.8% MoM (-40.2% in 1Q20). MoM, among the worst impacted financial shares were the big-four banks (Nedbank -53.2%, ABSA -43.3%, Standard Bank -31.0% and FirstRand -26.9%), while Capitec (-32.3%), RMB Holdings (-29.4%), Old Mutual (-24.3%) and Sanlam (-21.4%) were also pummeled. A rampant dollar saw the rand lose 13.9% of its value against the greenback in March. For 1Q20, the rand is 27.4% weaker vs the US dollar.

Looking at local economic data, annual consumer price inflation (CPI) advanced for a third month running, coming in at 4.6% in February (vs January’s 4.5%) and edging just above the SA Reserve Bank’s (SARB’s) monetary policy target range. The main contributors to the increase were higher prices of medical insurance, as well as food and non-alcoholic beverage prices. Retail sales improved in January, advancing 1.2% YoY from a prior recording of -0.5%, while MoM retail sales rose 0.9% vs -3.2% in December. February’s trade balance swung to the biggest trade surplus (R14.15bn vs January’s revised deficit of R2.72bn) in over a year as SA’s exports to Europe surged. Meanwhile, the SARB’s Monetary Policy Committee (MPC) cut the repo rate by 100 bpts to 5.25% in response to the COVID-19 pandemic, and in an effort to bring relief to consumers.

On 23 March, President Cyril Ramaphosa announced that SA will enter a nationwide lockdown for 21-days (from midnight 26 March) in a televised address to the nation. This proactive move by government, to curb the rapid spread of the virus, was widely praised. While government’s approach and handling of the situation was commendable it couldn’t have come at a worse time for SA’s crippled economy. 4Q19 GDP data showed that the local economy shrank by 1.4% YoY, leading us into a technical recession over the period (it follows a 0.8% revised GDP decline in 3Q19). To make matters worse, rating agency Moody’s cut SA’s sovereign credit rating to sub-investment grade (or junk) status with a negative outlook on the day the lockdown took effect. SA is now junk rated by all three major rating agencies.

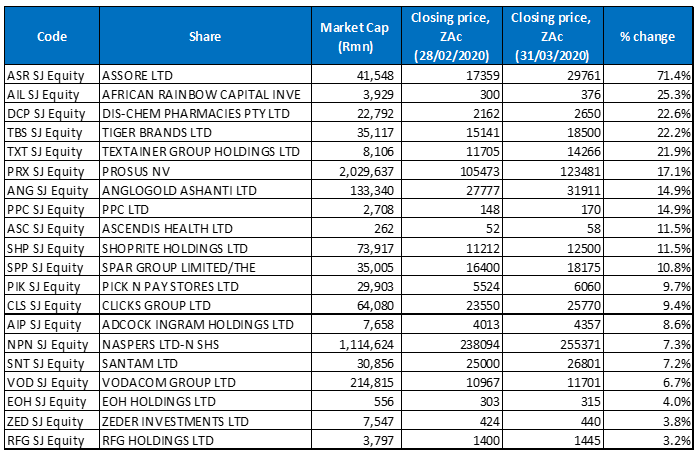

Top-20 March 2020, MoM

Source: Anchor, Bloomberg.

In a month in which the JSE became a sea of red as equity prices plummeted, there were still a few counters that managed to post gains despite the wild swings on our market. Mining Group Assore’s share price soared 71.4% MoM, making it March’s best-performing share. However, we note that the rocketing share price was due to the company announcing plans to buy-out its minority shareholders and then de-list the Group from the JSE after 70 years. On 9 March, Assore made a generous offer to buy out minority shareholders at R320/share (c. 80% upside from where the share had been trading recently). This saw the share price rocket by over 80% the following day.

In second spot, Patrice Motsepe’s investment holding company, African Rainbow Capital Investments (ARC), surged 25.3% MoM. Last month, Tech Central reported that ARC has attached a R13.1bn valuation to SA’s fifth mobile operator, Rain, giving it a value 40% above Telkom’s market cap as at 19 March. ARC valued its own 20.7% stake in Rain at R2.7bn, as at the end of December 2019.

ARC was followed by Dis-Chem in third position with a gain of 22.6%. Retailers have been benefitting from consumers stocking-up on essential goods, with the share prices of companies such as Dis-Chem, Tiger Brands (+22.2% MoM), Pick ‘n Pay and Clicks rising in anticipation of, and after, the lockdown.

Textainer, which leases shipping containers, recorded a MoM share price rise of 21.9%. The company earlier this week doubled its share repurchase programme to $50.0mn (c. R900.0mn), saying that the move reflects confidence in its long-term prospects. In September 2019, the firm announced a $25mn (c. R450mn) repurchase programme. The company is 47.5% owned by Trencor.

Prosus NV (+17.1% MoM), and Naspers, have held up well under the lockdown, likely due to a weaker rand and the fact that globally, during various countries’ respective lockdowns, online food deliveries, gaming, and retail thrives because of consumers’ reliance on digital platforms, thus boosting the likes of Tencent. Naspers has a c. 30% stake in Tencent, through Prosus.

Last week, AngloGold Ashanti (+14.9%) said that its Mponeng Mine, Mine Waste Solutions and surface rock-dump processing operations produced 419,000 oz of gold for the year ended 31 December 2019. It also announced that agreement has been reached to sell these assets to Harmony Gold with the transaction expected to close around 30 June.

Meanwhile, PPC (+14.9% MoM) said in an operational update on 18 March, that lower levels of capital expenditure have helped it offset lower earnings during the 11 months to end-February. In addition, the company noted that its Southern African business was starting to show signs of stabilisation even as it continues to face price pressures from increasing exports.

Rounding out the top-10 were Ascendis Health and Shoprite – both up 11.5% MoM. Ascendis, in its 1H20 results, reported that its revenue increased by 12% YoY to R3.9bn, while headline EPS fell 35.0% YoY to ZAc24.5. Looking ahead, the Group said its short-term priority was to complete its balance sheet restructure. Meanwhile, Shoprite, much like other essentials retailers, benefited from virus-fuelled panic buying at its stores.

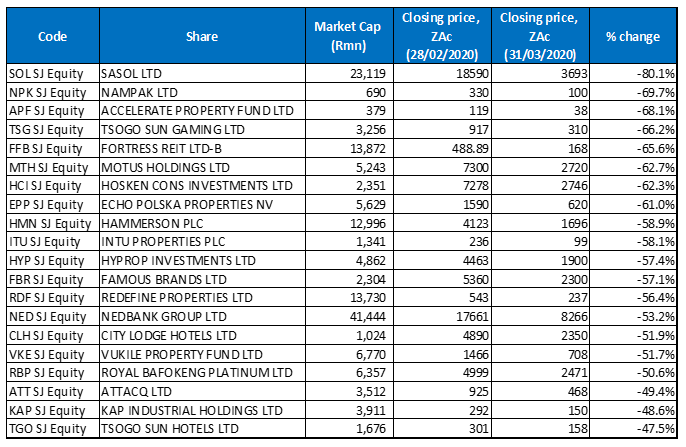

Bottom-20 March 2020, MoM

Source: Anchor, Bloomberg.

Five out of the ten worst-performing shares in March were property companies. The dire local economic outlook had already impacted property share prices hard when COVID-19 hit, but the sector is now in crisis as SA’s 21-day lockdown forces retailers into a situation where they may be unable to pay rentals, adding further pressure to SA’s already-struggling locally listed property sector. Some tenants (especially in the retail sector) will soon earn little or no turnover for some time, and we have no doubt they will want to renegotiate rentals with landlords. Some smaller tenants will go bankrupt. In addition, property companies may adjust (some have already) their capital retention policies — which could impact dividends.

Not surprisingly, Sasol was March’s worst-performing share – down 80.1% MoM. The share price recorded major losses on the back of a plummeting oil price and a worsening of the novel coronavirus. In addition to pressuring Sasol’s earnings, the low oil price places significant pressure on its already strained balance sheet. Sasol has built up a large debt burden due to a combination of weak oil and chemicals prices and heavy capital spending at its Lake Charles Chemicals Project. Its loan conditions require that its debt-to-profit levels remain above a certain level, and the lower oil price saw concerns mount that it will be in breach of its debt covenants, meaning Sasol’s loans could become immediately payable. However, on an investor conference call, CEO Fleetwood Grobler and Financial Director Paul Victor outlined details around a package of measures, that were aimed at addressing its balance sheet and ensuring Sasol’s profitability in the current challenging operating environment. The company said that it views a rights issue as a last-resort option and, instead, it is aiming to generate $6bn from cost savings and asset disposals.

Nampak (-69.7% MoM) was March’s second worst-performing share. In a trading update for the five months to 29 February 2020, the packaging Group said that the impact of COVID-19 was expected to further hinder an already burdened economy by putting more pressure on consumers’ disposable income. Nampak has also agreed to new terms with lenders due to the threat posed by a weaker rand (the local currency breached R18/$1 for the first time this week), noting that its net debt to earnings before interest, taxation, depreciation and amortisation (EBITDA) has been relaxed to 3.5 times from 3.0 times, with effect from its six months to end-March, due to the threat of a weaker rand and delays from proceeds of recent asset sales.

The co-owner of Fourways Mall, SA’s largest shopping centre, Accelerate Property Fund lost 68.1% MoM, coming in third among last month’s worst-performing shares. Accelerate said in a trading update that it has been forced to reduce rentals or even offer rent-free periods as shop owners battle with subdued consumer sentiment and load-shedding. The Group has seen rental reversions of 13.2% in the 10 months to end January, but added that it has also achieved a 93.5% tenant retention rate, which it believed will put pressure on income in the short term, but pay off in the future.

The lockdown has also impacted Tsogo Sun Gaming (-66.2% MoM), which has closed its hotels and casinos during the lockdown. In an update to shareholders, Tsogo Sun said reduced trading volumes since 19 March and the lockdown, would have a negative impact on its FY20 results although it still expects “to deliver a solid set of results regardless of this setback”. Prior to 15 March, Tsogo had been on course to deliver c. 4% YoY revenue and EBITDA, long-term incentives and exceptional items growth, with the second-half performing better than the first. However, it said that from 19 March its position “deteriorated significantly”, with sites operating at limited capacity due to the regulatory restrictions.

In March, Fortress (B share down -65.6% MoM) announced that it has changed its dividend policy to counter local economic headwinds. Fortress also said that it plans to exit non-core assets and reinvest the proceeds into high-quality logistics parks. A growing number of property groups say retaining cash will help them weather the difficult conditions that are likely to continue for the short term.

Motus Holdings, Hosken Consolidated and Echo Polska Properties (EPP) recorded MoM declines of 62.7%, 62.3% and 61.0%, respectively. EPP, Poland’s largest retail landlord, in March delayed payment of EUR53.0mn (R1.0bn) in dividends for its year to end-December and did not provide any guidance for FY20, due to uncertainty over COVID-19. Rounding out the top-10 were two other property companies, Hammerson Plc (-58.9% MoM) and Intu Properties (-58.1% MoM).

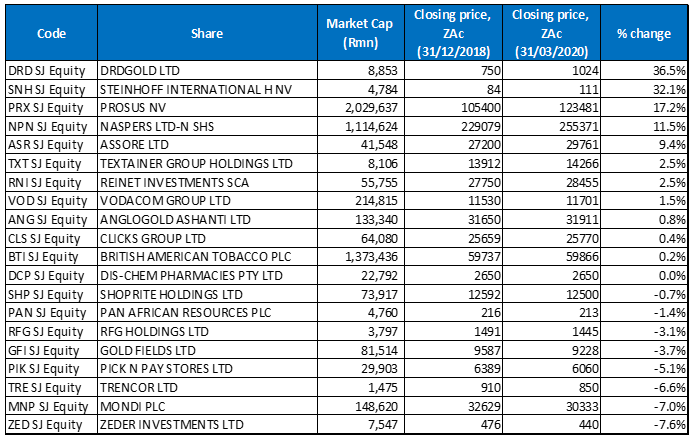

Top-20 March 2020, YTD/1Q20

Source: Anchor, Bloomberg.

Five of March’s best-performing shares YTD/1Q20 were also among the top-10 performers for the year to end February. However, Assore (+9.4%), Textainer (+2.5%), Vodacom (+1.5%), AngloGold Ashanti (+0.8%) and Clicks Group (+0.4%) bumped Pan African Resources, Harmony Gold, Stenprop, BAT and Royal Bafokeng Platinum out of the top-10.

After taking the number-one spot in the year to end February, Steinhoff (+32.1% YTD/1Q20) lost ground, falling to second place with DRDGold (+36.5% YTD/1Q20) moving up to the top spot for the quarter. Despite their share prices coming under pressure during March’s worst days on the market both Prosus and Naspers gained ground YTD/1Q20 – up 17.2% and 11.5%, respectively.

Reinet (+2.5% YTD/1Q20) was pushed down the ladder after its 11.7% share price drop in March, while Vodacom recorded a 6.7% share price gain last month helping it show a YTD/1Q20 gain of 1.5%.

Finally, AngloGold Ashanti and Clicks rounded out the YTD/1Q20 top 10, with Clicks benefitting from the lockdown as it remains open during the 21-day period and customers scurry to buy those essentials Clicks sells.

Bottom-20 March 2020, YTD/1Q20

Source: Anchor, Bloomberg.

Looking at the YTD/1Q20 worst performers, apart from EOH Holdings (-74.9%) and Famous Brands (-70.5%), which replace Motus Holdings and EPP among the YTD/1Q20 worst-performing shares, the remainder were unchanged from the MoM rankings. As with the MoM worst performers, Sasol (-87.8%) and Nampak (-85.4%) were the two worst-performing shares but in third spot, Intu (-84.2%) moved down a few notches vs its MoM performance, replacing Accelerate as the third worst-performing counter.

YTD/1Q20, in fourth position, was Fortress-B, which lost 78.5%, and was followed by Accelerate (-78.3%), EOH Holdings (-74.9%), and Tsogo Sun Gaming (-74.8%). Not even a 4.0% MoM gain during a market rout could pull EOH out of the worst-performers list. The troubled technology group said in March that it has trimmed its losses for the six months to end-January. In a trading update, EOH said it expects to report a headline loss per share from total operations of up to ZAc525 for the period vs a ZAc993 loss previously, while its headline loss from continued operations is expected to be no more than ZAc500/share. EOH noted that it is around 12 months into a turnaround plan that is expected to take at least two years to complete, adding that “good progress on key strategic initiatives in respect of the evolving business model, cost savings and capital structure initiatives has continued over the past six months.”

Famous Brands is down 70.5% in 1Q20. The company said last week that its sales had slowed down from the beginning of March as the COVID-19 outbreak took its toll on consumer activity and shortened trading hours. According to the Group, initial indications were that sales deteriorated steadily in the first three weeks of March as governments took measures to restrict consumer activity, with those markets where the virus had been prevalent for longer being most affected.

Finally, Hammerson and Hosken’s share price drops in March saw these counters pulled down by 70.0% and 69.8% in 1Q20.