Finance Minister Enoch Godongwana presented South Africa’s (SA) 2026/2027 Budget on 25 February against a more constructive backdrop than last year, when National Treasury (NT) had to table it three times before it was finally adopted on 21 May 2025. Broader consultation within the Government of National Unity (GNU) and improved in-year fiscal performance contributed to a more measured, market-friendly tone.

While last year’s difficulties were a poignant reminder of what we all already knew – that SA’s finances are stretched, soaring gold and platinum prices have seen tax revenues from mines increase, and a R21bn revenue over-collection relative to prior forecasts has provided the government with significant wiggle room.

Consistent with November’s Medium Term Budget Policy Statement (MTBPS), the 2026 Budget reinforces a commitment to fiscal consolidation. The focus remains on stabilising public debt rather than introducing significant new spending or tax increases. VAT is unchanged at 15%, with revenue growth expected to come primarily from improved collection and compliance efforts at the SA Revenue Service (SARS), coupled with a growing economy rather than higher tax rates. As the deficit narrows, the government’s borrowing requirements are projected to decline, easing funding pressure.

Revenue performance exceeded expectations, with gross tax revenue R21.3bn higher than forecast in last year’s Budget, driven by stronger VAT, corporate income tax, and dividend taxes. This primarily reflects commodity-linked corporate performance. Treasury projects tax revenue to keep increasing in nominal terms rather than stagnate, forecasting gross tax revenue to rise from c. R2.0trn in 2025/2026 to R2.13trn in 2026/2027 and R2.4trn by 2028/2029, implying a steady revenue base supporting government spending while the deficit narrows.

On the expenditure side, total spending continues to rise in nominal terms, with large allocations for strategic areas such as infrastructure and social services over the next three years. However, expenditure growth is expected to moderate sufficiently to prevent it from outpacing revenue growth, allowing debt to stabilise and, over time, decline.

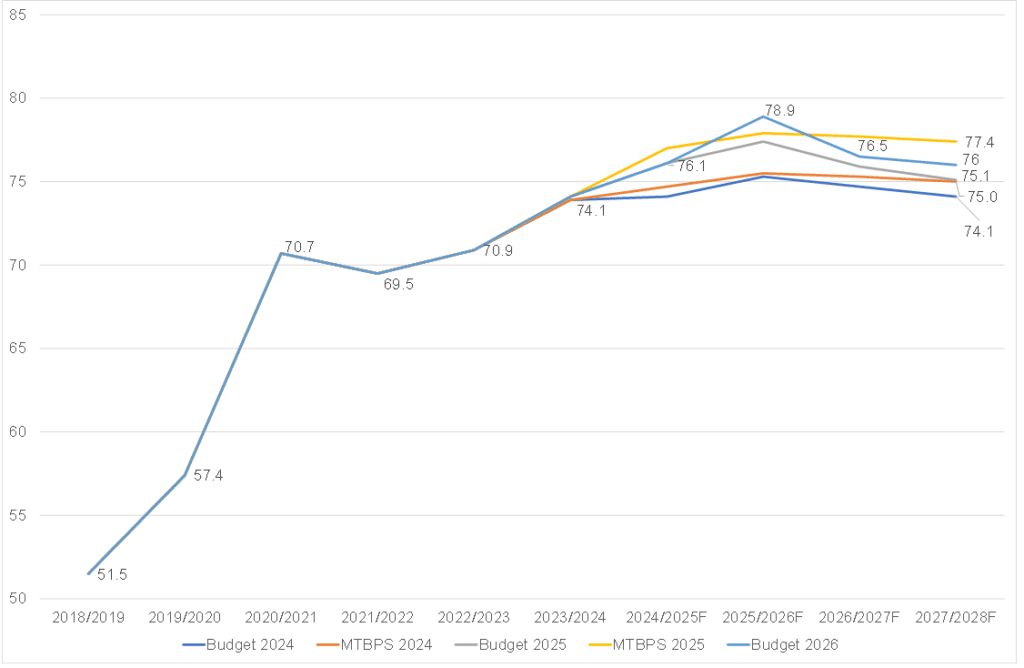

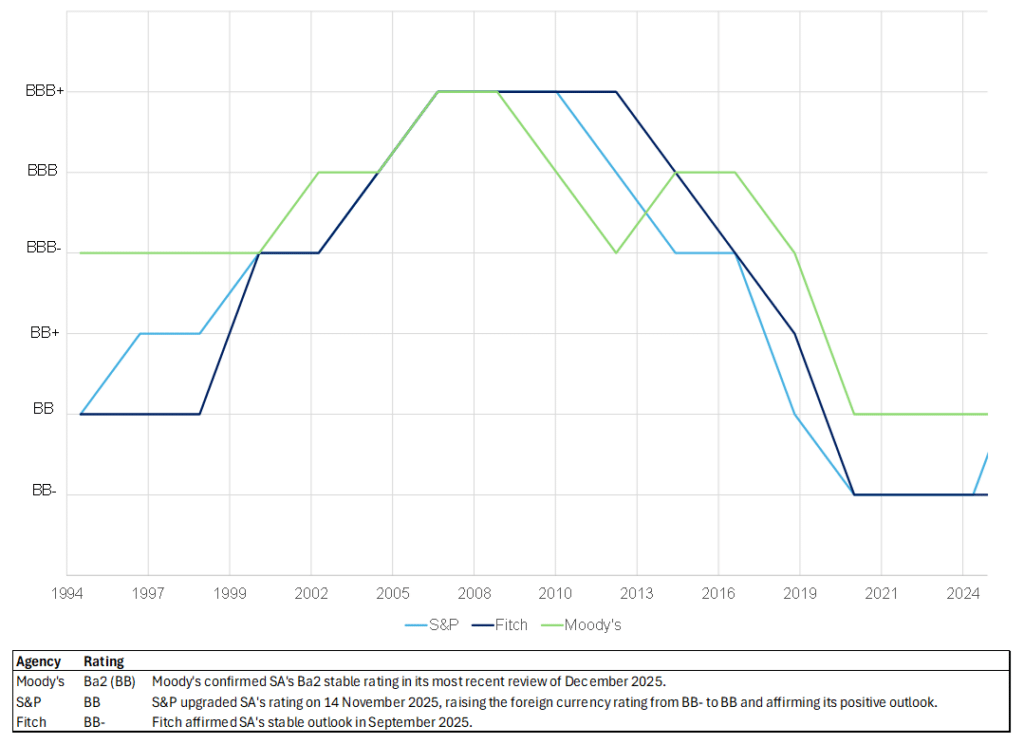

Real GDP growth is forecast at 1.6% this year, improving modestly thereafter. Public debt is expected to peak at 78.9% of GDP (slightly higher than we would have liked), but importantly, it will start to decline from here. This should please financial markets and the rating agencies a little (see Figure 2). SA’s recent removal from the Financial Action Task Force (FATF) grey list and a sovereign credit rating upgrade from S&P Global in November (to BB from BB-, while maintaining a positive outlook) have been further positive developments.

Figure 1: SA government debt as a percentage of GDP, %

Source: NT, Anchor Capital

Figure 2: SA sovereign credit ratings

Source: Reuters, NT, Anchor Capital

The deficit is forecast to decline from the current 4.5% to 3.1% in 2027/2028. For once, this seems believable. Achieving this will more than likely see further credit rating upgrades by 2028. We continue to believe that an upgrade in 2026 is plausible, though it is more likely to arrive only in 2027.

Encouragingly, Treasury is using the fiscal breathing room to reorient spending toward growth-enhancing investment. Infrastructure outlays remain a priority, with allocations for infrastructure spending continuing to rise, and ongoing monitoring and structural reform at Transnet, Eskom and water infrastructure. The Passenger Rail Agency of South Africa (PRASA) received a meaningful allocation of R5.8bn for railcars.

The windfall taxes on commodities have given some scope for tax relief for individuals. This is in the form of an inflation adjustment to personal income tax brackets, an increase in the annual tax-free savings thresholds and a rise in limits to maximum deductions for retirement savings.

The annual turnover threshold for registration as a VAT vendor has been increased to R2.3mn, which reduces the potential administrative burden on smaller businesses.

As expected, fuel levies and excise duties (“sin taxes”) were increased notwithstanding the overcollection from mines. A beer now carries ZAc8 more tax, while a litre of petrol will cost ZAc21 more due to a blanket inflationary adjustment to the general fuel (GFL) and Road Accident Fund (RAF) levies. Draft regulations under the Currency and Exchanges Act will introduce enhanced oversight of cryptocurrencies.

Grants have been increased marginally for recipients; however, the cancellation of 35,000 fraudulent claims mitigates the cost impact.

We also note a continued commitment toward public-private partnerships (PPPs), which should continue to yield benefits for the country.

Overall, the impression is one of the government taking pragmatic advantage of the opportunity afforded to SA by the commodity boom to take a few small steps in the right direction. The fiscal outlook is not without risks. Weaker global growth, commodity price volatility, and the precarious financial health of several state-owned entities (SOEs) all remain vulnerabilities. High debt redemptions will continue to sustain large borrowing requirements, and the slow pace of structural reform (particularly in energy, logistics, and local government) continues to constrain growth. In addition, we are left guessing regarding the plans for the National Health Insurance (NHI) funding and how robust the fiscal anchor (that is touted to form part of the MTBPS this year) will be. Still, for now, we expect a slightly stronger financial market as the budget serves to confirm that we are staying on the path of fiscal consolidation.